NY Fed Mortgage Debt Data Says No US Recovery

Home › Forums › The Automatic Earth Forum › NY Fed Mortgage Debt Data Says No US Recovery

- This topic is empty.

-

AuthorPosts

-

November 30, 2012 at 12:36 am #8415

Raúl Ilargi Meijer

KeymasterLet me try to keep this short and still make the point I want to make. Lately, I've seen a huge amount of people talking about an economic recover

[See the full post at: NY Fed Mortgage Debt Data Says No US Recovery]November 30, 2012 at 9:21 am #6506SteveB

ParticipantThe obvious question: is inventory up because no one’s buying it?

The emperor should be passing through any day now.

November 30, 2012 at 10:21 am #6507Anonymous

GuestI’m curious, other than the fact that the graph starts at 2003, is there any reason that 2003 debt levels are supportable now, or in the resource-depleted future?

November 30, 2012 at 10:32 am #6508Viscount St. Albans

ParticipantRe: Mortgage Debt Reduction and Deficiency Judgements

How much of that reduction in Household Mortgage debt is really an illusion? If a house is sold for less than the debt owed (through short-sale or foreclosure auction), then banks have 5 years to decide whether or not to sue homeowners for the loss (the deficiency). If the judge agrees with the bank, then homeowners, who think they’ve shucked off the ball-and-chain, will soon find the shackles re-applied through a deficiency judgement.

Type the words “deficiency judgement” into google. You’ll see that this sneaky dog is beginning to snarl, bark-at, and bite the moms and pops who thought they’d moved-on to better days.

Most homeowners don’t know that a deficiency judgment has been activated until the debt collectors begin to knock at the door and ring the phone. The provision to seek debt collection for the mortgage loss is often buried deep in the legal fine print of short sale and foreclosure documents, and banks or loan sharks who buy the distressed debt have 20 years to collect.

https://online.wsj.com/article/SB10001424053111904060604576572532029526792.html

November 30, 2012 at 12:09 pm #6509Mark T

MemberHiding the government’s liabilities from the public makes it seem that we can tax our way out of mounting deficits. We can’t

Cox and Archer: Why $16 Trillion Only Hints at the True U.S. Debt

https://online.wsj.com/article/SB10001424127887323353204578127374039087636.html?mod=googlenews_wsj

November 30, 2012 at 1:43 pm #6510davefairtex

ParticipantIlargi –

I agree with all the stuff you say. I’ll add:

As long as the US government can successfully borrow 30% of federal expenditures every year, I think that things will remain largely happy. Our housing prices bounce, we see a modest recovery, and all will seem well.

Its only when we can no longer live on prosperity borrowed from the future that the whole ponzi system will unwind – the way it is doing right now in Spain and Greece. So that market crash that some people expect won’t happen until that inability to borrow comes home to the US government. Inability to borrow happens first in the periphery and then moves to the core. And the US defines “the core”, so it will happen here last.

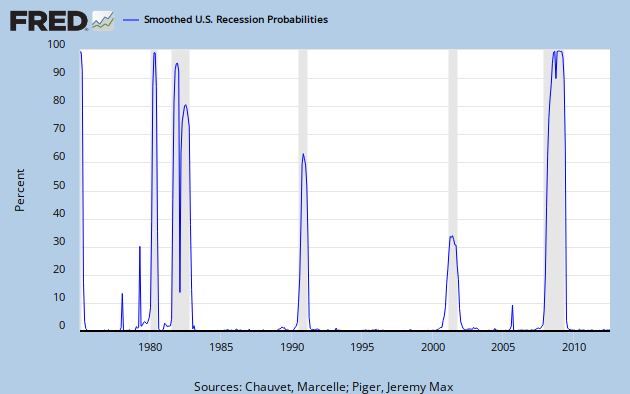

Regarding recoveries though – an interesting chart crossed my screen the other day. An indicator which seemed to do a good job at predicting recessions. Here’s the chart:

https://research.stlouisfed.org/fredgraph.png?g=dht

I make no claims on its ability to prognosticate, but it did intrigue me. This indicator doesn’t trigger too often, and in the past 40 years it has never gone above 20% without a recession happening very soon thereafter. My trader instinct says to wait for it to hit 30-40% before taking action, because these are unusual times. This indicator is updated monthly. However, I have not done a deep dive into understanding what goes into calculating this index. Here’s the paper behind the calculations, in case YOU want to dive into this particular rabbit hole:

https://research.stlouisfed.org/publications/review/03/03/ChauvetPiger.pdf

Having an indicator that can detect the onset of a recession in real time is actually quite valuable – at least for those of us who are interested in such things anyway. Usually, we only find out we entered a recession six months after the fact.

Will a recession cause a market crash? An interesting question. It would surprise me, given all the money being borrowed and spent. But it could happen. Currently, I’m on the fence.

November 30, 2012 at 2:39 pm #6511backwardsevolution

MemberIlargi – great article. Thank you. Here’s the New York Fed’s report from August, 2010 (scroll down three pages). Comparing the two, you can see that student debt has increased from 4% to 8% in the last two years, auto loans have increased from 6% to 7%, HE revolving has gone from 6% to 5%, and mortgages from 74% to 71%.

They’ve just rearranged the deck chairs.

https://www.newyorkfed.org/research/national_economy/householdcredit/DistrictReport_Q22010.pdf

Karl Denninger spoke about GDP and inventories today:

“That (government deficit spending) is bad, not good. But it’s reported as good and people lap it up. And inventory build is indeed GDP, but building inventories mean that manufacturers are not selling as fast as they’re producing — this typically happens right in front of recessions!”

November 30, 2012 at 8:18 pm #6512Participantdavefairtex post=6215 wrote: Usually, we only find out we entered a recession six months after the fact.

Dave,

That might just be the case.

December 1, 2012 at 12:47 am #6513Ghung

Participant“…the low-hanging fruit has been picked when it comes to household deleveraging.”

In the past 15 years we’ve deleveraged to where we have no power company, no water company, no utilities at all in fact. By year’s end we’ll have no mortgage or other debt. Heck, the utilities don’t even have an easement onto our property. We’re also firing our big telecom, going with a local wireless WAN provider and VOIP. Just doing our part to move things along.

When one adopts something akin to Greer’s “voluntary poverty” meme, what one “may a) need, b) demand and c) want” comes into clear focus, as do the predicaments faced by the average ‘consumer’ and our overall economic system. Deleveraging begets decoupling and disinvestment, leaving one wondering how in hell we ever got to this point.

Perhaps we’ll use the load of bricks lifted from our backs to build a new barn or something, or just enjoy the clarity that comes with no longer being deluded. Many thanks to TAE, TOD, TAR, and others for providing context and support during these trying years.

Get thee to the non-discretionary side…. Stop feeding the beast.

December 1, 2012 at 1:39 am #6514Ken Barrows

ParticipantSteve from Virginia has it right: industrial society cannot pay for itself, at least until the thorium reactors or nuclear fusion give us the net energy to grow out of this massive debt :). Seems to be that Bill McBride is just another unquestioning believer in perpetual growth. Haven’t read much from him on energy issues.

December 1, 2012 at 2:03 am #6515KeymasterAmen to all that, Ghung.

And kudos for getting there.

Wish many more people would have the foresight to follow suit.

We’re grateful we could play our little part in it.

December 1, 2012 at 3:53 am #6516TonyPrep

ParticipantDave Cohen is also discussing the debt issue on his blog:

https://www.declineoftheempire.com/2012/11/us-household-debt-is-totally-out-of-control.html

December 1, 2012 at 4:19 am #6517jal

ParticipantSteve from Virginia has it right: industrial society cannot pay for itself, at least until the thorium reactors or nuclear fusion give us the net energy to grow out of this massive debt.

Off topic

Has anyone ever calculated how much heat is being released into our environment by oil, natural gas, coal, nuclear, and volcanoes?

Having thorium reactor as another heat producer does not seem me that there would be any decrease in the amount of heat that is being pumped into our environment.

Global warming problems … here we come.

December 1, 2012 at 5:20 am #6518GuestAn interesting graph, for sure. I have to say, however, that I am a little confused… The article takes the stance that households MUST deleverage by $2 to $3 trillion (back to the 2003 level), end of story, no alternative. What’s the economic argument for 2003 debt levels? Why not 2005, or 2001, or any other year for that matter? The article also says that the massive deleveraging is inevitable, but is it not possible that the economy could fluctuate for decades between moderate further deleveraging and minuscule growth? I don’t believe the market pumpers who say we’re “getting back to normal” (what the heck is “normal” after all), but I also have trouble with the idea that total collapse is the only alternative.

December 1, 2012 at 5:27 am #6519Gravity

ParticipantSome people say Gravity is a recursive algorithm.

December 1, 2012 at 6:23 am #6520Keymaster“The article takes the stance that households MUST deleverage by $2 to $3 trillion (back to the 2003 level), end of story, no alternative.

That’s correct, mostly. Only thing is it doesn’t stop there.

“What’s the economic argument for 2003 debt levels? Why not 2005, or 2001, or any other year for that matter?”

It seems obvious to me that the 2003 levels are but an example. We could go back further in time, and that would mean more deleveraging. For most people mentally getting used to 2003 levels is bad enough.

“The article also says that the massive deleveraging is inevitable, but is it not possible that the economy could fluctuate for decades between moderate further deleveraging and minuscule growth?”

Where, in that hypothetical case, would people find the money, for decades, to pay off their debt?

“I don’t believe the market pumpers who say we’re “getting back to normal” (what the heck is “normal” after all), but I also have trouble with the idea that total collapse is the only alternative.”

Hey, what the heck is “total collapse” after all?

December 1, 2012 at 8:17 am #6521seychelles

ParticipantI’ve always had the notion that the real estate mania started in 1998 and that imploding manias usually overshoot to the downside. If those ideas are true, we have a whole lot more deleveraging before the system is cleansed. In my neck of the woods, nothing would be selling without FHA loans and a lot of the new ones are already having payment problems.

December 1, 2012 at 9:37 am #6522william

ParticipantTo say the emperor has no clothes would be an understatement. The debt only describes consumer habits of spending unearned dollars.

At a certain point countries that matter will no longer accept the US dollar as the currency of trade. A few years back China put forth in its long term plan that it would in 10 years stop accepting US dollars in trade. They made the announcement to prepare nations.

China has stated about a month ago it will no longer strive to increase world trade but encourage economic trade within its borders. I don’t believe most get the implications but it is simply this: those mortgages and debts we have are held by the Chinese only in the short term and will not be held much longer.

Good luck and get out of debt. Credit is the new boring and Cash is the new sexy.

December 1, 2012 at 10:16 am #6523ParticipantMoney quote from articles linked below:

————————————————

“the resale marketplace for deficiency judgments is growing, with the debt being packaged, chopped up and sold to investors just like mortgages once were.”

——————————————————————————Question of the day:

How many Insurance companies are investing in S&P rated triple-AAA debt built from sliced and diced mortgage deficiency judgements?Anyone looking for a job in this economy? Here is your growth industry.

Article Bar Graph Analysis — where are the numbers?

Sorry to beat a dead horse (see my comment above), but just in case:

Looking at that bar graph, mortgage debt seems to start falling after Q3 2008. I wonder: How was that mortgage debt reduction calculated?

If banks have 5 years post mortgage default to sue for deficiency (i.e. loss) then we really won’t know how much mortgage debt was eliminated until we factor in the number of banks that are allowing their right to sue to expire. Everyone who defaulted anytime after 3rd quarter 2008 is not out of the woods, debt-wise, until 3rd quater 2013. The same 5 year delay holds for everything else going forward. I just don’t see how the numbers underlying this graph were calculated.Given all the accounting shenanigans that have transpired since the financial crisis in ’08, I wouldn’t be surprised if many banks are counting mortgage losses as assets, based on their plan to sue for the deficiency. Thus, the mortgage losses aren’t even realized. The losses (unpaid debts) simply became bank assets that are sold to the street corner knee-capper/debt collector.

When you view the issue from this perspective, the fall in mortgage rates and the enticement to refinance (along with the conversion of non-recourse to recourse loans) the whole issue takes on a much more sinister hue.

https://www.tampabankruptcylawyerblog.com/2011/04/deficiency-judgment-landmines.html

December 1, 2012 at 7:10 pm #6524gurusid

ParticipantHi folks,

… I’m pretty sure about the timing that auto sales were going to collapse a lot further, and he had some arguments on it and I went and looked and thought “auto sales also can’t go too much further, people have to replace their cars.” And so I wrote this article that says look, auto sales are near the bottom – we were at a 9 million annual rate then- I said there’s just no way – we have to be selling 12, 13,14 million because people need new cars every 5-7,8 years.

I do like Bill McBride, and his work, and I do like Joe Weisenthal, but I’m sorry, I simply don’t think you can say things like that. It harks back all the way to the dry semantic discussion of what it is that people may a) need, b) demand and c) want. You can’t say that people will buy cars because they need a new one every 5-8 years. Because they will still need to have the money to buy them. Demand is what people can afford, not what they want.

The pic refers to Cuba’s famed old pre-revolution US imported cars most of which are over fifty years old, and are now since 2009 allowed to be ‘sold’ after draconian communist property laws were relaxed. However:

One difficulty facing many Cubans, who make an average monthly salary equivalent to about $20, will be rounding up the money to buy a car. “It’s a good law, but I can’t even buy a bicycle,” said a peanut vendor who did not give his name.

The ‘irony’ is palpable…

L,

Sid.December 1, 2012 at 7:28 pm #6525ParticipantHi Illargi,

As regards GDP, disasters usually have a marked ‘positive’ effect on it, creating a demand for replacement goods and infrastructure. It remains to be seen whether Sandy will have any effect in this way given the lack of credit and demands placed upon the fragile insurance sector (they’re invested in the same dodgy ‘instruments’ as everyone else!). As regards the law of supply and demand, I am reminded of the old joke about two economists variously stuck somewhere dark and confined (apart from having one’s head up the proverbial). When they start to get hungry they do not worry; they ‘know’ that their demand will create sandwiches!

L(ol!)

Sid.December 1, 2012 at 9:13 pm #6526Participantjal post=6222 wrote: Having thorium reactor as another heat producer does not seem me that there would be any decrease in the amount of heat that is being pumped into our environment.

Global warming problems … here we come.

jal, it’s not the heat that’s the problem, it’s the trapping of it. As for thorium, it’s already generating heat, just as all the other radioactive particles on/in the planet. It’s not as simple as just capturing the heat, but thorium reactors wouldn’t cause any kind of spike in heat relative to what we’re already generating, assuming that population and demand don’t climb further.

December 2, 2012 at 1:47 am #6527steve from virginia

Participant@Ken Barrows:

“Steve from Virginia has it right: industrial society cannot pay for itself, [strike]at least until the thorium reactors or nuclear fusion give us the net energy to grow out of this massive debt … [/strike]

Industrial society cannot pay for itself, period. Neither fusion nor thorium reactors can pay for themselves for the same reason coal mines and oil fields do not, they cannot meet their combined life-cycle costs + externalities. We fool ourselves with credit and misused arithmetic, false analysis and politics.

We want what we want and lie to ourselves to get it.

December 2, 2012 at 2:45 am #6528ParticipantRe: Household deleveraging — Some may see the irony in this article:

“…securitized energy-efficiency debt…”

“There is, in short, a gap between what technologists are selling and what consumers are buying. That gap has big environmental costs, given the vast amounts of energy the United States wastes each year through leaky buildings and inefficient machines. Now, a growing cadre of savvy investors is betting there’s money to be made bridging that divide. They’re designing complex financial instruments to bankroll energy-efficiency improvements in houses and other buildings across the country. And they’re setting themselves up as the middlemen…

Taking back their leverage for a noble cause. Jeez.

December 2, 2012 at 6:51 am #6529ChartistFriendPgh

MemberThe 4 Year Presidential Election Cycle Indicator https://chartistfriendfrompittsburgh.blogspot.com/2012/12/the-4-year-presidential-election-cycle.html

December 2, 2012 at 10:27 pm #6530paddler

MemberCan someone extrapolate or expand to the Canadian situation? Are we looking at a similar de-leveraging phenom in Maple Leaf Land giving the high consumer debt levels? Where are home/and prices headed and how geographically sensitive are the pressures?

December 3, 2012 at 5:42 am #6531MemberDecember 3, 2012 at 10:04 am #6533sangell

MemberGiven that there is another debt account, the public debt, and that it has grown by about $10 trillion since 2003 with most of that growth since 2008, a reduction in private consumer debt of a couple of trillion isn’t deleveraging at all. Reducing my Visa card balance by running up my balance ( OK I get a better interest rate) on my new Master Card isn’t getting me out of debt especially when that public spending accounts ( through transfer payments) for such a large proportion of consumer income. Thus if you actually try and reduce the growth in public debt you actually make the private debt burden grow.

December 3, 2012 at 10:57 am #6534Loch

ParticipantDebt is the thermodynamic demand we place on the future.

Forget, and I mean it, forget, alternative energy. Whatever you have now, you have as a benefit of FIRE. Cars, computers, wind generator parts, solenoid operated steam valves, turbine blades… it all takes fire to produce. Someone, somewhere has to build a fire and melt the metal to make the things needed to make the things and to get the oil, or coal, or uranium needed to fuel the fires.

You and me, we’re on fire. It’s all about oxidation, baby. Oxidation, fast or slow, and the fuel to oxidize. That’s what the economy boils (no pun intended) down to. Debt overhangs and speculative bubbles are nothing more or less than indications of heat energy deficits. We promise more than we can deliver from our respective fires, or fuel stores to make the fires.

December 3, 2012 at 8:09 pm #6535pipefit

Participant“That is, an economic recovery in the US is not possible when households still have to deleverage to the tune of $2-3 trillion.”

I don’t see too much mention of interest rates. With mortgage interest rates still dropping, I think you are a bit early with your call. I agree that the economy isn’t growing, but the main reason for that is that CPI and PPI is much higher than stated by the govt. and therefore REAL growth is much lower than stated.

Freddie Mac says a 30 year fixed is now 3.32%, and a 15-yr is at 2.64%. We are approaching the end here, but I think there is one more leg down.

The key web site to look at is https://droughtmonitor.unl.edu/. All the major grain charts are bullish, and corn and wheat super bullish. If we don’t get way above average rain/snow over much of the eastern half of the nation within five months, you are going to see food price inflation on a terrifying scale.

Once this food price inflation kicks in, next Summer, the fed will be powerless to stop it. Bernanke talks of removing stimulus at a moment’s notice, but as you pointed out, the economy isn’t growing, so he can’t raise rates. This coming hyperinflation will be one for the ages.

December 3, 2012 at 8:28 pm #6536ParticipantSangell said, “Given that there is another debt account, the public debt, and that it has grown by about $10 trillion since 2003….”

Where on Earth did you get that, lol? The public debt is growing $6 trillion per YEAR, using GAAP accounting. See shadowstats and many others. The hyper inflationary phase is well underway!!!!

December 3, 2012 at 9:25 pm #6537Keymaster“That is, an economic recovery in the US is not possible when households still have to deleverage to the tune of $2-3 trillion.”

I don’t see too much mention of interest rates. With mortgage interest rates still dropping, I think you are a bit early with your call.

There’s no timeline anywhere in that call, so how can I be early?

I agree that the economy isn’t growing, but the main reason for that is that CPI and PPI is much higher than stated by the govt.

No, the reason there’s no growth is that the debt levels, both public and private, don’t allow for it.

If we don’t get way above average rain/snow over much of the eastern half of the nation within five months, you are going to see food price inflation on a terrifying scale.

There’s no such thing as “food price inflation”. Which doesn’t mean prices can’t go up. Calling it inflation keeps you from understanding why, though.

That desperate US hyperinflation call of yours is what’s early, way early. It’s typical for those who see the US only, not the world it’s part of. A pretty general affliction; but that still doesn’t make it right.

December 3, 2012 at 10:32 pm #6538Participant“That desperate US hyperinflation call of yours is what’s early, way early.”

You’ve responded to many of my posts that contain a mention of the size of the Federal budget deficit, as measured by GAAP accounting, without addressing that. Annual deficits that are 40% of GDP are hyper inflationary. Money creation on a grand scale. So, no, I am not early at all.

You can argue that social security and medicare are going to be eliminated, and maybe federal employee pensions, military pensions, VA benefits, etc. But that is an argument for the abolition of representative democracy first. And that will be the immediate end of the dollar as the world’s reserve currency, and its return to its inherent worth, zero. And anarchy, with a barter economy.

Barring a weather miracle, food prices are going way up in about six months, all over the world. Unlike the USA, where food accounts for a small percentage of the typical family’s budget, for the majority of the planet it is approaching half or more of the typical family’s budget.

Food importing countries are not going to have luxury of playing the ‘beggar-thy-neighbor’ currency self immolation game of destroying their own currencies to make their exports more attractive. They are going to actively move to strengthen their currencies to combat mass starvation. The USA, being a net food exporter, will see the relative value of its currency drop like a rock. Before 4th of July, 2013!!!!!

December 3, 2012 at 11:44 pm #6539SidDAvis

MemberFederal Reserve Notes, checking account balances, saving account balances, CD’s, etc. are simultaneously the debts of banks and are the “money” supply we use. When an economy uses bank debt for money, in order for money supply to be increased (bank debt to be increased) banks out of thin air create new checking account balances and loan them to people, businesses, and governments, thus indenturing the public. When these loans are repaid to banks the money supply decreases. This is why debt owed to banks, directly or indirectly, is a drag on economic activity.

Increases in money supply have a tendency to drive up prices as the new money enter the market and bids up prices. Decreases in money supply have the opposite effect. But at higher price levels, the buying power of existing money is reduced so higher prices drag down economic activity.

One of the major factors of the ability of a society to carry debt is income, and when the cost (in money terms and in energy terms) of acquiring energy increases a society’s income diminishes. Its debt carrying ability comes under pressure. Each sources of energy has a cost curve that exhibits compound growth at some rate, ultimately making them terminal as cost in energy terms approaches 100% of the energy acquired.

When government attempts to control markets with subsidies, their own spending, taxing and borrowing, and regulations, the tendencies of an economy to come into balance are thwarted.

Of course there are other factors, but income, debt, price levels, and government interference are quite significant. The old adage that a depression is in size proportional to the debt issued during the preceding boom, and in length is proportional to the effort of government to manage it, seems to be appropriate. But that equation leaves out the problem of energy which is a game changer since energy constraints become income constraints of a society of already indentured servants.

While there is unlikely any avenue to escape our long term fate of economic contraction, certainly (1)abandoning the predatory, unstable, unsustainable monetary system based on credit and fractional reserve banking, and (2)eliminating most of the federal government, would give us a better shot at dealing with what is to come. Of course neither of these will happen peacefully, if at all.

December 6, 2012 at 1:46 am #6542Participant… No US Recovery

Who is his right mind would want a recovery!!

By having inflation with bubbles?

By printing more money to cover the theft done by the bankers?

Oppps!

The financial system want to go back to the way it was and have a recovery.

Its not going to happen.

Japan was lucky to be able to do it for as long as they did.

Now watch what happens to the EU countries as they try to get the printing press rolling.

December 6, 2012 at 10:52 am #6544Babble

ParticipantWell, I see two problems with using the graph. First, it is in dollars so it is not inflation adjusted and second it is not population adjusted. Therefore the debt per capita is lower than shown.

December 6, 2012 at 5:03 pm #6545Nassim

ParticipantI just saw this in the French newspaper le Figaro. It seems that the young (15-24) in mainland France now have an unemployment rate of 24.2% – it was 22.8% three months ago. Of course, a large proportion of people in that age group are students and don’t count as unemployed.

Here is a Google translation:

And the original:

I can’t see them not protesting in the Greek way sometime soon.

December 10, 2012 at 2:32 pm #6555GuestYou did not factor in interest rates in this analysis. Interest rates today are half what they were in 2003. Thus even though households are carrying a larger mortgage debt, the mortgage payment might be lower because the interest rate is lower. By 2010, mortgage interest payments had already fallen below 2003 levels, and the interest rate has dropped further since then.

https://www.bls.gov/opub/btn/volume-1/a-comparison-of-25-years-of-consumer-expenditures-by-homeowners-and-renters.htmDecember 10, 2012 at 10:29 pm #6558Participantkublikhan post=6263 wrote: You did not factor in interest rates in this analysis. Interest rates today are half what they were in 2003. Thus even though households are carrying a larger mortgage debt, the mortgage payment might be lower because the interest rate is lower. By 2010, mortgage interest payments had already fallen below 2003 levels, and the interest rate has dropped further since then.

I suspect that for most households, a lower mortgage payment simply enables them to pay of a little more credit card debt each month. If so, not the makings of a recovery. Anecdotally, friends trying to refinance haven’t been able to due to being ‘under water’. Those people who have been able to refinance aren’t likely to do so a second time due to the costs involved.

While low interest rates might make a difference for some individuals, they don’t seem to be significant in the big picture.

-

AuthorPosts

{kind=link}

- You must be logged in to reply to this topic.

Sorry, the comment form is closed at this time.