Tim McKulka Elderly Woman Receives Emergency Food Aid, Sudan 2008

Thought we were already there.

• Markets Are In The Twilight Zone, Get Ready For New New Deal (AFR)

Macquarie analysts have likened the bizarre and inherently contradictory moves in markets to a “twilight zone” which is leading investors to a world where free-market economic thinking will be overtaken by the “nationalisation of credit” and state-sponsored growth. Think about that. Monetary policy is beating a path to a world where conventional market signals such as credit spreads and the price of risk will “finally perish” and be unseated by one where states are the drivers of credit, and spending and capital formation is the domain of central banks. “It would take the form of state-sponsored stimulation of consumption, investment, [research and development] and rescuing what essentially is a bankrupt financial superstructure (ie banks, insurance, life and pensions),” the Macquarie report, authored by Hong Kong-based analyst Viktor Shvets, said.

“Whilst similar to FDR’s New Deal, it would be a far more distorted world than either the 1930s or the 1960s-70s, with brand new investment signals.” [..] The unusual commentary from Macquarie says this “state driven paradise” will be brought on by ongoing high levels of volatility and “discontinuities” similar to what markets are grappling with today. “We don’t believe these conditions are yet satisfied, but the chances are high that they would be over the next 12-18 months. In the meantime, we still expect half-hearted ‘stop and go projects’. Japan is likely to be the first to ‘jump’ and wholeheartedly embrace this merger of fiscal, income support and monetary policies but others would eventually follow. It is just a matter of time.”

The Bank of Japan and re-elected Japan Prime Minister Shinzo Abe have signalled a fiscal-led stimulus package in excess of ¥10 trillion ($98 billion) is under consideration. The contradiction that Macquarie is referring to is the way markets have behaved since Brexit, where assets historically linked to “risk-on” and “risk-off” moods have inexplicably rallied in unison. Equities, a classic risk asset, have recovered all of their losses since the Brexit vote on the belief that central banks will step in and lift asset prices by doing stimulus and ignore sound fears about asset bubbles.

Read more …

His role is questionable. Shirked far too close to influencing politics.

• BOE Governor Carney Accused Of ‘Peddling Phoney Forecasts’ Over Brexit (G.)

Mark Carney has agreed to hand notes of private meetings he had with the chancellor in the run-up to the EU referendum to MPs, after a Treasury select committee hearing where the governor of the Bank of England faced questions about whether he had “peddled phoney forecasts” about the risks of a vote for Brexit. In his first appearance at the Treasury select committee since the referendum, the Bank’s governor faced questions about whether he had tried to scare the electorate by warning of the economic shock – and possible recession – that a vote to leave the EU would cause. Andrew Tyrie, the committee’s chairman, citing two former chancellors and two former leaders of the Conservative party, said the Bank had also been accused of “startling dishonesty”.

Tyrie, a Conservative MP, told Carney that the accusations, if true, would be a “very robust assault on the Bank’s credibility” and also of the independence from government it was granted in 1997 that could not be recovered under the Canadian’s tenure. Carney said he had held private meetings with George Osborne before the 23 June vote. He agreed that the MPs could appoint someone to review the notes of those meetings but said he would be reluctant for them to be made public. Carney was also asked by Jacob Rees-Mogg, a prominent Brexit campaigner, whether the Bank should be, like Caesar’s wife, beyond suspicion in terms of being influenced by politicians. The governor, who said politicians had sought to inform him rather than influence him, replied: “Those who cast it [the independence] into question should consider their motivations and their judgments.”

Read more …

That would mean Stage Five: Acceptance. It’ll take a while. In the meantime, the ‘gloom’ is driven by politics, not economics. And yes, Carney is the champ, hoping for a self-fulfilling process. The Leave camp, which won (remember?), should perhaps ask for him to step down.

• Carney Should Stop Being So Gloomy About Brexit (Ashoka Mody)

Few have been more downbeat about the outlook for the U.K. economy than the country’s own central bank governor, Mark Carney. If he wants to help mitigate the consequences of the vote to leave the European Union, he should send a more encouraging message by holding back on monetary stimulus. People charged with managing economies usually try to be optimistic, on the logic that their positive attitude will give people and businesses the confidence to spend and invest, ultimately making the optimism self-fulfilling. The rhetoric surrounding Britain’s vote on EU membership has been a glaring exception. In a bid to influence the vote, a chorus of global policymakers predicted dire consequences. That chorus has sadly persisted.

After voters chose to leave, the secretary general of the Organisation for Economic Cooperation and Development, Angel Gurria, reiterated forecasts of higher unemployment and permanent damage to household incomes. Christine Lagarde, managing director of the IMF, said that the decision was “casting a shadow over international growth.” Yet Brexit’s shadow is hard to discern amid the broader global decline in output growth and interest rates that began in early 2014. Perhaps no one, though, has been as active as Carney in stoking feelings of gloom and doom – a particularly notable feat, given that central bank governors rarely make predictions of economic and financial turmoil, especially when it concerns their own currency.

As far back as May, the Bank of England said that the possibility of Brexit was already weighing on the British pound, even though much of the decline in sterling’s value had happened earlier, when the polls – and especially the betting markets – showed a clear lead for the “Remain” campaign. The currency actually stabilized during the brief period when polls showed the “Leave” campaign gaining ground. Markets have come to anticipate Carney’s public appearances as harbingers of bad news. The pound began to decline in the hours before his first major post-Brexit speech on June 30, and he did not disappoint: Brexit-induced uncertainty, he insisted, had caused “economic post-traumatic stress disorder amongst households and businesses, as well as in financial markets.”

Read more …

Or else what?

• German Leaders Demand Brexit Clarity From New British PM (R.)

German leaders stepped up the pressure on Britain’s incoming prime minister Theresa May on Tuesday by demanding she swiftly spell out when she will launch divorce proceedings with the European Union. “The task of the new prime minister … will be to get clarity on the question of what kind of relationship Britain wants to build with the EU,” Chancellor Angela Merkel told a news conference. Her finance minister Wolfgang Schaeuble said clarity was needed quickly to limit uncertainty after Britain’s shock choice for ‘Brexit’, which has rocked the 28-nation bloc and thrown decades of European integration into reverse. May, 59, will on Wednesday replace David Cameron, who is resigning after Britons rejected his advice and voted on June 23 to quit the EU.

On arriving and departing from Cameron’s last cabinet meeting, she waved a little awkwardly from the doorstep of 10 Downing Street, shortly to become her home. She will face the enormous task of disentangling Britain from a forest of EU laws, accumulated over more than four decades, and negotiating new trade terms while limiting potential damage to the economy. The pound was up 1.2% against the dollar at around $1.3150, boosted by the appointment of a new prime minister weeks earlier than expected after May’s main rival dropped out. But it remains more than 12% below the $1.50 it touched on the night of the June 23 referendum, reflecting concerns that Brexit will hit trade, investment and growth.

The German leaders spoke after May’s ally Chris Grayling appeared to dampen any hopes among Britain’s EU partners that her rapid ascent might accelerate the process of moving ahead with the split and resolving the uncertainty hanging over the 28-nation bloc.

Read more …

Which of course can be blamed on Brexit again. But it’s really just a Ponzi scheme dying a natural death.

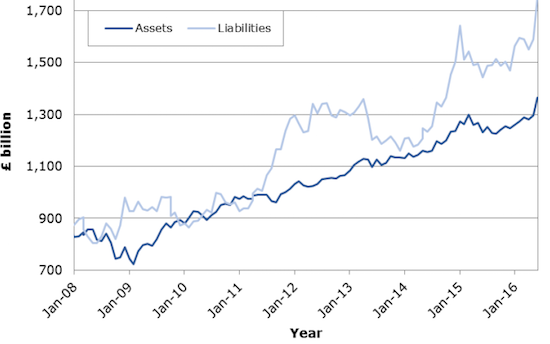

• British Pensions £383 Billion Underwater As Liabilities Hit Record (Tel.)

Britain’s gold-plated pensions now have record-breaking liabilities of £1.75 trillion after the EU referendum triggered a rout in their core gilt and equity holdings, highlighting the difficulty of funding the UK’s retirement needs. The country has almost 6,000 defined benefit schemes, which are obliged to pay their members an amount in retirement often tied to their final salary. Just 950 of these schemes were in surplus on June 30, with the rest hoping to make up the shortfall from long-term investment returns. In total, defined benefit funds are £383.6bn underwater, compared to £294.6bn just a month ago, as the tumbling UK government bond yields added to liabilities while global stock markets wiped value from the schemes’ equity investments.

Around 78pc of the long-term liabilities of the schemes are funded, down from 81.5pc within a month. While these figures are merely a snapshot, the data from the Pension Protection Fund highlights the precarious position of numerous schemes. “Companies are having to divert profits into schemes to make good on their promises, which means less investment capital to help businesses grow and less money available to invest in the pensions of younger workers,” said Tom McPhail, head of retirement policy at Hargreaves Lansdown. “Accrued pension rights have to be respected and investors have to be able to trust the system, however there is also a growing argument for the Government to look at finding a more balanced approach to the retirement funding needs of UK workforce.”

UBS analysts have estimated that a 1pc fall in real yields on government bonds results in a 10pc rise in pension liabilities, although this varies by scheme depending on how many bonds they hold. Gilts have jumped in price, lowering their yields, as global investors seek out safe havens. Industrial companies have the largest pension burdens, amounting to 77pc of their overall market value of the businesses, according to UBS’s research, while telecoms firms have liabilities worth 56pc of their value and utilities’ liabilities have reached 54pc.

Read more …

Hilarious.

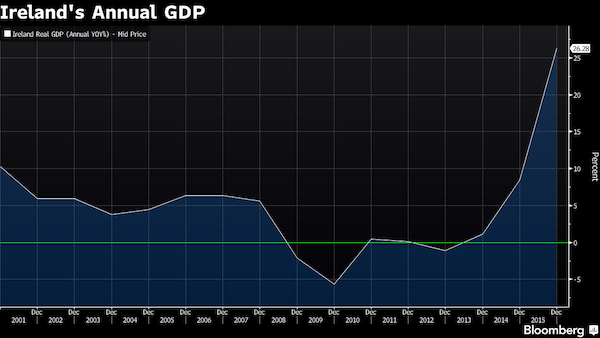

• Ireland’s Economists Left Speechless by 26% Growth Figure (BBG)

In three days, Jim Power is due in London to brief the British-Irish Trade Association on the state of the Irish economy. Now, he has no idea what he is going to say. The economy grew 26% in 2015, officials from the Central Statistics Office told a stunned room full of economists and reporters in Dublin on Tuesday. Previously, they had estimated growth of 7.8%. “I’m not going to stand up and say the economy grew by 26%,” Power, an independent economist, said after the release. “It’s meaningless – we would be laughing” if these numbers came out of China, he said. The figure is mostly explained by the open nature of Ireland’s economy and its attraction to U.S. companies seeking access to a 12.5% tax rate.

Among firms that have inverted to Ireland, mostly through acquisitions, are Perrigo and Jazz Pharmaceuticals. Corporations with assets overseas of €523 billion were headquartered in Ireland in 2014, up from €391 billion in 2013, according to the statistics office. “We are a very small economy, and if we get a big increase in assets, this is what happens,” Michael Connolly, an official at the CSO, said on Tuesday. Once explained the numbers are “believable,” he said. In a statement, Finance Minister Michael Noonan pointed out that growth numbers cut Ireland’s debt and deficit ratios. Trouble is, they carry downsides too. For one, tax inversions artificially inflate the size of Ireland’s economy.

When the headquarters of a group of companies becomes resident in Ireland, all of its global profits may be counted as part of the nation’s gross national income, according to the ministry. Since 2008, that gauge has been boosted by about 7 billion euros thanks to corporate relocations, without accompanying substance or employment, the ministry has said. This in turn drives up the country’s contribution to the European Union budget, which is based on the size of the economy. For a second thing, it leaves self-described “baffled” analysts like Power at a loss to explain the state of the Irish economy. Power says he’ll look at indicators like employment growth and tax revenue for a better gauge, and guesses Ireland’s underlying economic growth was 5.5% last year.

Read more …

A world of pain.

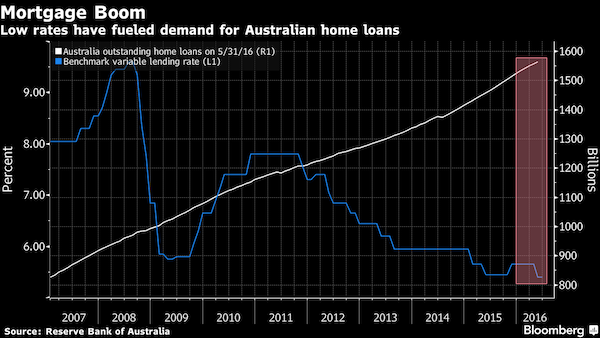

• Losing Australia’s AAA Rating To Make Losers of Mortgage Holders (BBG)

The biggest losers after Prime Minister Malcolm Turnbull scraped through to win Australia’s fractious elections could be homebuyers facing higher costs on their A$1.6 trillion ($1.2 trillion) in mortgages. The price to protect bonds issued by the nation’s banks climbed seven basis points last week after S&P Global Ratings cut its outlook on Australia’s AAA grade to negative on concern government deficits will persist without “more forceful” decisions to rein in shortfalls. It also put the nation’s biggest lenders on notice. Stephen Miller, BlackRock’s head of fixed income for Australia, said Wednesday there’s a “real risk” Australia loses its top debt score.

“An increase in funding costs relating to a ratings downgrade will impact bank margins, but banks may choose to offset this via loan pricing,” said Anthony Ip at Citigroup in Sydney, adding that any increase in funding costs will be significant but manageable. “At the end of the day it’s still a competitive lending market.” Australia’s largest lenders – Australia & New Zealand Banking, Commonwealth Bank of Australia, National Australia Bank and Westpac Banking – rely on offshore bond markets for a fifth of their funding requirements, central bank data show. If their rankings were lowered after a sovereign downgrade, that would increase borrowing costs as much as 20 basis points, prompting them to slap mortgagees with higher interest rates, according to Citigroup.

Read more …

I smell a timebomb.

• The Richest Generation in US History Just Keeps Getting Richer (BBG)

Baby boomers started turning 65 in 2011, marking the unofficial beginning of their retirement years. The timing could not have been better for older boomers, who are already part of the wealthiest generation in U.S. history. Since then, the broad S&P 500-stock index is up 91%, including dividends. U.S. stocks hit a record high yesterday. Market performance in the early years of retirement is a crucial worry for anyone living off a nest egg. In the worst-case scenario, stocks crash just as retirees start spending their savings, leaving them in a hole they can no longer earn their way out of. Older boomers have experienced what is arguably the best-case scenario: The S&P 500 has returned 269% since its March 2009 low.

As a recent study in the Journal of Financial Planning shows, wealthy retirees can be very cautious about spending down their savings. This instinct, along with the stock market’s new record, suggests that many boomers are likely to end up with far more money than they know what to do with. Researchers followed the spending and investing behavior of 65- to 70-year-olds from 2000 to 2008. The poorest 40% of the survey respondents generally spent more than they earned, according to the study, which was funded by Texas Tech University. Those in the middle were able to keep their spending at about 8% below what they could have safely spent from pensions, investments, and Social Security.

The wealthiest fifth, meanwhile, had a gap of as much as 53% between their spending and what they could have spent. The authors wrote: “Retirees in the top quintile of financial wealth were spending nowhere near an amount that would place them in danger of running out of money. In fact, the average financial assets of wealthy retirees increased during this period and most retirees spent less than their income.” In other words, these affluent Americans retired and then continued to get richer. That’s quite a feat when you’re no longer working, particularly against the backdrop of the mediocre stock market of the early 2000s.

Read more …

Conditions in Greece are getting worse, fast. I’ll soon have more on that, firsthand. Meanwhile, another 4 refugees died this morning off Lesbos.

• A Year After Bailout, Greece Struggles For Brighter Future (AFP)

A year after it fought and lost a tug-of-war with its creditors, Greece remains a country that seems adrift, and many of its citizens view the present as joyless and the future as grim. Summer 2015 saw Greece’s youthful left-wing Prime Minister Alexis Tsipras wage an extraordinary battle between the mighty European Union, the European Central Bank and the IMF. Over five months, Tsipras and his firebrand finance minister, Yanis Varoufakis, took Greece and Europe to the brink as they demanded the creditors ease reforms imposed under two previous bailouts agreed since 2010. As the EU, ECB and IMF took a hard line, Greece’s financial flows shrank and a bank crisis loomed – but Tsipras, instead of buckling, stunned the world by announcing a referendum on the new deal proposed by creditors.

On July 5, 62% of voters rejected the package. But even with the mandate of the Greek people behind him, Tsipras backed down: the risk of seeing Greece thrown out of the eurozone was too much. Instead, in a dramatic U-turn, he let go of Varoufakis, replaced him with the more moderate Euclid Tsakalotos – and just over a week later, signed the third bailout. The deal was worth €86 billion over three years and laden with conditions, such as tax hikes and pension reforms, considered by critics to be so tough that social media buzzed with talk of a coup d’etat. Since then, Greece has soldiered on, weathering popular unrest and the consequences of the 2015 migration crisis, while Tsipras strives to defend his leftwing credentials.

Read more …

Brussels is completely lost. Time to end its misery.

• EU Development Aid To Finance Armies In Africa (EuO)

The EU commission wants to finance foreign armies as part of a larger effort to stop people from fleeing to Europe, including in countries with patchy human rights. A commission draft proposal released on Tuesday (5 July) spells out reasons why it is “necessary to provide assistance to the militaries of partner countries”. Some €100 million that were initially slated for development aid will be diverted to finance military-led border control exploits and other initiatives like mine-clearing The EU money can also be used to finance anything from troop transport vehicles to uniforms and surveillance equipment. Even furniture, stationary and “sport facilities” are covered. The EU has already contracted out some €1 billion from 2001 to 2009 when it came to things like law enforcement and border management.

But this is the first time it will pump money directly into a foreign military structure. “The direct financing of the military is not possible [at the moment]. Due to exceptional circumstances in some partner countries, it was important to close this gap,” notes the document, a joint communication to the European Parliament and EU Council. The document attempts to quell some concerns over how the money will be used. It notes, for instance, that it won’t fund “recurrent military expenditure”, weapons and ammunition, and combat training. But such limitations are unlikely to be taken seriously by critics. “This proposal is nothing short of scandalous,” said German Green deputy Reinhard Butikofer.

Read more …

No Ambrose, not the International Court of Justice. The ruling was by the Permanent Court of Arbitration. And your conclusion is fit for the National Enquirer: “The world has not been in such peril since the Cuban Missile Crisis.”

• Global Arms Race Escalates As Sabres Rattle In South China Sea (AEP)

The South China Sea has become the most dangerous fault-line in the world. Beijing and Washington are on a collision course over these contested waters, the shipping lane for 60pc of global trade. As expected, the International Court of Justice in The Hague has ruled that China has no “historic title” to areas of this sea stretching all the way to the ‘nine dash line’ – deep into the territorial waters of a ring of South East Asian states. Equally expected, Beijing has dismissed the verdict with scorn, accusing the tribunal of “shamelessly abusing its authority”. The state media said the country “must be prepared for any military confrontation” with the US, and must not flinch from war if provoked.

It is the latest in a series ominous developments in Asia and Europe that are rapidly subverting the Western international system and setting off a global rearmament race with strong echoes of the late-1930s. Tensions are flaring up across so many spots in East Asia that global investment funds are actively betting on defence stocks and technology companies linked to military expansion. Nomura has launched an “Asian Arms Race Basket” as a hedge against potential conflicts in the East China Sea, the Straits of Taiwan, and the South China Sea. Among the companies listed are Mitsubishi Heavy Industry and Sumitomo Precision in Japan, China Shipbuilding and AVIC Aircraft in China, Korea Aerospace and the explosives group Hanwha, as well as Reliance Defence and Bharat Electronics in India.

The Stockholm International Peace Research Institute says China spent $215bn on defence last year, a fivefold increase since 2000, and more than the whole of the European Union combined. It is developing indigenous aircraft carriers. US experts say its “Two-Ocean Strategy” implies a fleet of five or six aircraft carrier battle groups to project global power. Japan has upgraded its once invisible Self-Defence Force to a full-fledged fighting machine with a humming new headquarters and an air of determined alertness. The country has been increasing military spending for the last four years, especially under its nationalist leader Shinzo Abe, commissioning its largest warship since the Second World War, an 800-ft DDH-class helicopter carrier.

Rearmament has paradoxical effects. It acts as a form of Keynesian stimulus, as it did in the late 1930s. The spending might absorb some of the Asian savings glut and eat into excess industrial capacity, lifting the world out of secular stagnation, but it is a lethal way to do it. A parallel process is underway in Europe where defence spending has been shooting up since the Russian invasion of Crimea, ending years of neglect and austerity budgets. Outlays are expected to rise by 20pc in Central and Eastern Europe this year, and 9.2pc in South-Eastern Europe, according to the French think-tank IRIS.

Read more …

Not terribly smart people.

• Economic Theory as Ideology (Zaman)

[..] For a very long time, economists refused to take results from experiments seriously, because these were in direct conflict with axioms at the heart of economic theories. The empirical failure of economic axioms led to the creation of “Behavioral Economics,” which studies actual behavior of human beings. In any scientific field, “behavioral economics” would be the center of attention, since it matches the observational evidence about human behavior. Furthermore, the axiomatic theory, which is contradicted by the empirical evidence, would be a long forgotten idea belonging to the primitive history of economic science. Surprisingly, mainstream economic textbooks, used all over the planet, continue to teach axiomatic theories of human behavior as if they are true, while behavioral economics remains neglected and ignored.

Why do economists maintain an ideological commitment to patently false theories of human behavior? Certainly it is not because these theories are noble and elevating. In fact, many observers have argued that these theories create immoral behavior, by teaching that selfishness, without concern for morality or society, is rational for everyone, and good for society. For example, Nobel Laureate Milton Friedman taught that businesses should maximize profits, without any concern for social responsibility. Given this license, multinational corporations have gone on a rampage, exploiting natural resources by using methods which threaten to destroy the planet. The easiest way to make a profit is to appropriate a priceless natural treasure, like a rainforest, and chop it down for timber.

The losses from industrial wastes are changing the composition of the atmosphere, oceans, lakes and rivers, and inflicting costs on all human beings, but creating profits for corporate coffers. This strategy is called ‘socializing the losses and privatizing the gains.’ With massive profits, it is easy to buy politicians to prevent environmental concerns from getting in the way. The book Merchants of Doubt documents a well funded campaign to create doubt about climate change, so that corporations can continue to make profits while destroying the planet. The persistence of economic theories which celebrate and glorify these poisonous ideologies of personal greed and social irresponsibility can be traced to corporate funding of think-tanks and research which promote “free markets”. The charms of “freedom” propagated by economic ideologies conceal the ugly reality of corporate freedom and wage slavery of the masses.

Read more …

The glory of mankind.

• Half Of All US Food Produce Is Thrown Away (G.)

Americans throw away almost as much food as they eat because of a “cult of perfection”, deepening hunger and poverty, and inflicting a heavy toll on the environment. Vast quantities of fresh produce grown in the US are left in the field to rot, fed to livestock or hauled directly from the field to landfill, because of unrealistic and unyielding cosmetic standards, according to official data and interviews with dozens of farmers, packers, truckers, researchers, campaigners and government officials. From the fields and orchards of California to the population centres of the east coast, farmers and others on the food distribution chain say high-value and nutritious food is being sacrificed to retailers’ demand for unattainable perfection.

“It’s all about blemish-free produce,” says Jay Johnson, who ships fresh fruit and vegetables from North Carolina and central Florida. “What happens in our business today is that it is either perfect, or it gets rejected. It is perfect to them, or they turn it down. And then you are stuck.” Food waste is often described as a “farm-to-fork” problem. Produce is lost in fields, warehouses, packaging, distribution, supermarkets, restaurants and fridges. By one government tally, about 60m tonnes of produce worth about $160bn, is wasted by retailers and consumers every year – one third of all foodstuffs. But that is just a “downstream” measure.

In more than two dozen interviews, farmers, packers, wholesalers, truckers, food academics and campaigners described the waste that occurs “upstream”: scarred vegetables regularly abandoned in the field to save the expense and labour involved in harvest. Or left to rot in a warehouse because of minor blemishes that do not necessarily affect freshness or quality. When added to the retail waste, it takes the amount of food lost close to half of all produce grown, experts say. “I would say at times there is 25% of the crop that is just thrown away or fed to cattle,” said Wayde Kirschenman, whose family has been growing potatoes and other vegetables near Bakersfield, California, since the 1930s. “Sometimes it can be worse.”

Read more …