Alfred Palmer New B-25 bomber at Kansas City plant of North American Aviation 1942

“..Joe and Joanna Sixpack want to scream in rage. They are doing so by rejecting the establishment political parties and candidates at almost every electoral turn..”

• Albert Edwards: Central Bankers Lead Us On The Road To Perdition (ZH)

Earlier this week we described the personal come to non-GAAP Jesus moment of trading commentator Richard Breslow, who confessed in no uncertain terms that he has had it with endless central banking intervention: “a portfolio built to only withstand stress thanks to central bank intervention is one destined to blow-up spectacularly. The embedded flaw in this new logic is that central banks give investors perfect foresight. And nothing can go wrong… You don’t need to be a Taleb or Mandelbrot to calculate that we have been having once in a hundred year events on a regular basis for the last thirty years.”

Today it is another famous skeptic, SocGen’s Albert Edwards who has had enough and says he feels “utterly depressed” because he has not “one scintilla of doubt that these central bankers will destroy the enfeebled world economy with their clumsy interventions and that political chaos will be the ugly result. The only people who will benefit are not investors, but anarchists who will embrace with delight the resulting chaos these policies will bring!” As he openly warns his readers : “I have long recognised my own contrariness (or is it bloody-mindedness) and hopefully put it to good use in my chosen profession. If you want the consensus bull-market cheerleading nonsense, readers know it is amply available elsewhere.” With that warning in place, here is why the man who popularized the deflationary “Ice Age” blows up”

“I am neither monetarist nor Keynesian. I see merit and demerit in both sides of a very fractious argument. But what I do know is when in the last few weeks I have heard that Janet Yellen sees no bubble in the US, when Ben Bernanke hones and restates his helicopter money speech, and when Mario Draghi says that the ECB’s policy of printing money and negative interest rates was working, I feel utterly depressed (I could also quote similar nonsense from Japan, the UK and China). I have not one scintilla of doubt that these central bankers will destroy the enfeebled world economy with their clumsy interventions and that political chaos will be the ugly result. The only people who will benefit are not investors, but anarchists who will embrace with delight the resulting chaos these policies will bring!”

We said in 2010 when the Fed launched QE2 that the ultimate outcome would be civil (or more than civil) war, so we thoroughly agree with Edwards “depression” because sadly he is right, but since stocks keep rising, few others seem to care. Edwards’ lament continues:

“I’m not really sure how much more of this I can take. So here we are 5, 6 or is it now 7 years into this economic recovery and it still remains pathetically weak. And so it should in the wake of one of the biggest private sector credit bubbles in history. The de-leveraging hangover was always going to be massive and so it is. Quick-fix monetary QE nonsense has made virtually no difference to the economic recoveries other than to inflate asset prices, make the rich richer, inequality worse and make Joe and Joanna Sixpack want to scream in rage. They are doing so by rejecting the establishment political parties and candidates at almost every electoral turn and seeking out more extreme alternatives at both ends of the political spectrum. And who can blame them apart from the chattering classes?

I have just returned from Germany on a marketing trip. I absolutely agreed with their Finance Minister Schäuble when he blamed ECB loose money policies for contributing to the rise in the extremist right Alternative for Germany party. Schäuble, “said to Mario Draghi…be very proud: you can attribute 50% of the results of a party that seems to be new and successful in Germany to the design of this [monetary] policy,” And this is not just a German phenomena – it is a global one. The people are angry and they are lashing out. But central bankers have painted themselves into a corner with their overconfident rhetoric and monetary experiments. They have now committed us all to their road to perdition.”

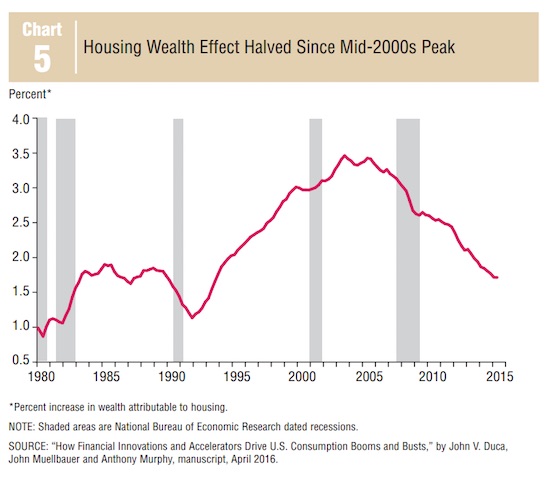

Deflation 101: “..around the middle of 2005, households would spend an extra $3.40 in the event that their home gained in value by $100. Near the end of 2015, households would increase outlays by just $1.70..”

• America’s Wealth Effect From Rising Home Prices Has Been Cut in Half (BBG)

The U.S. consumer might be the engine of global growth – just not the roaring V12 it used to be. From the fourth quarter of 2003 through 2006, amid the real estate bubble, personal consumption expenditures grew at an average annual clip of 3.5%. Since the S&P/Case-Shiller Composite 20-City Home Price Index bottomed out in March 2012, however, personal consumption expenditures have increased by just 2.3%, on average. In an economic letter published by the Federal Reserve Bank of Dallas, economists John Duca, Anthony Murphy, and Elizabeth Organ identify one reason why this American muscle car has lost its nitrous oxide. The researchers found that the wealth effect from real estate – that is, the extent to which home price appreciation juices consumer spending – has been cut in half since the mid-2000s:

The chart shows that around the middle of 2005, households would spend an extra $3.40 in the event that their home gained in value by $100. Near the end of 2015, households would increase outlays by just $1.70 if real estate values rose by the same amount. “In other words, home prices in 2015 need to rise double as fast as in 2005 in order to generate the same impact on consumer spending,” writes Torsten Slok, chief international economist at Deutsche Bank. “This weaker wealth effect is a key reason why the recovery since 2009 has been so weak.” This finding reinforces the challenge that monetary policymakers faced in reflating the U.S. economy via large-scale asset purchases, as this transmission channel didn’t pack the same punch it used to.

The wealth effect for liquid assets, such as bank deposits, is substantially higher than for illiquid assets like real estate, a testament to the ease with which the former can be deployed. The housing bubble of the aughts was characterized not only by soaring real estate values, but also households’ penchant for using real estate as a piggy bank to finance current consumption. In the wake of the crisis, access to credit by this channel was curtailed dramatically and the debt overhang served as a notable drag on consumption, to boot. “In the U.S., increased availability of consumer and mortgage credit, along with rising asset prices, contributed greatly to the consumption boom in the mid-2000s; reversals in these factors exacerbated the bust in consumption during the Great Recession,” the authors wrote.

A huge bubble in things nobody wants. China gets nuttier by the day.

• China’s Great Ball of Money Is Rushing Into Commodities Futures (BBG)

Chinese speculators have a new obsession: the commodities market. Trading in futures on everything from steel reinforcement bars and hot-rolled coils to cotton and polyvinyl chloride has soared this week, prompting exchanges in Shanghai, Dalian and Zhengzhou to boost fees or issue warnings to investors. While the underlying products may be anything but glamorous, the numbers are eye-popping: contracts on more than 223 million metric tons of rebar changed hands on Thursday, more than China’s full-year production of the material used to strengthen concrete. “The great ball of China money is moving away from bonds and stocks to commodities,” said Zhang Guoyu at Tebon Securities “We’ve seen a lot of people opening accounts for commodities futures recently.”

The frenzy echoes the activity that fueled China’s stock market last year before a rout erased $5 trillion, and follows earlier bubbles in property to garlic and even certain types of tea. China’s army of investors is honing in on raw materials amid signs of a pickup in demand and as the nation’s equities fall the most among global markets and corporate bond yields head for the steepest monthly rise in more than a year. Hao Hong, chief China strategist at Bocom International in Hong Kong, says the improvement in fundamentals and the availability of leverage to bet on commodities is making them irresistible to traders. “These guys are going nuts,” Hong said. “Leverage exaggerates the move of the way up, but also on the way down – much like what margin financing did to stocks in 2015.”

The gain in steel prices isn’t just on the futures market, with spot prices for the physical product also rallying amid a sudden shortage as construction activity accelerates. Rebar prices have risen 57% this year on average across China, according to Beijing Antaike Information Development, a state-owned consultancy. Even after output of steel increased to the highest monthly volume on record in March, rebar inventory is still falling, signaling a supply deficit.

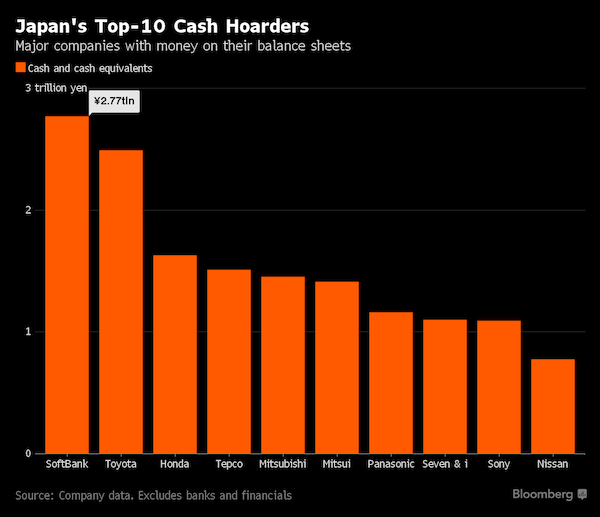

No-one wishes to acknowledge that it’s over. There’s a reason Japan Inc. is not investing.

• Ex-BOJ Economist Suggests Tax to Make Japan Inc. Spend Their Cash (BBG)

Japanese policy makers have taken extraordinary measures in recent years to yank the nation clear of deflation and create a better environment for businesses. They’ve had mixed results, and corporate Japan is yet to reciprocate with higher spending and wages. That’s prompted some analysts to suggest more radical ways of compelling companies to deploy their cash hoard on capital investment and salaries. Hiromichi Shirakawa, a former central bank official who is now chief Japan economist at the Credit Suisse Group, is at the forefront of the debate with his plan to tax corporate savings. “We have to try this policy as a last resort for beating deflation,” he said in an interview by telephone from Tokyo. “We have been suffering deflation for twenty years and the current policy is still not working.”

Shirakawa’s thinking goes like this: Corporate savings have swelled since Prime Minister Shinzo Abe came to power at the end of 2012 and unleashed fiscal stimulus and unprecedented monetary easing via the Bank of Japan. The ultra-loose policy weakened the yen, boosting profits for exporters. These earning must now be put to work. Kozo Yamamoto, one of the key members of Abe’s brains-trust of reflationist advisers, thinks the idea is worth looking at. This month he called for more fiscal stimulus, a fresh round of easing from the central back and the consideration of a tax on corporate cash. Imposing a 2% levy tax on cash and deposits of non-financial corporations could spur them to redirect enough money into investment to boost GDP by 0.9%, according to one scenario explored by Shirakawa.

That’s a significant bump given that GDP is likely to expand about 0.5% this calendar year, based on the median of forecasts compiled by Bloomberg. Meanwhile, the BOJ’s preferred inflation gauge is hovering around zero. Businesses remain wary of boosting investment, given Japan’s low growth rate and the likelihood that the market for goods and services will contract as the population ages and declines. While ruling party lawmakers responsible for tax policy say they’re not currently looking at this option, the BOJ’s recent adoption of negative interest rates may open the door wider than ever before. By introducing the concept of a tax on savings – if only, for now, on a portion of cash that financial institutions park at the central bank – the move could in time spur a broader debate about fiscal measures to force companies to spend more.

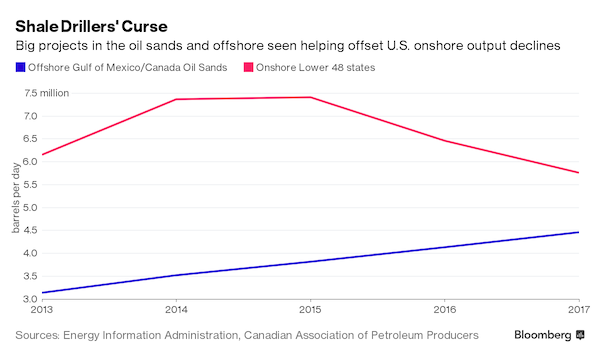

Follow the money.

• US Oil Megaprojects Dreamed Up a Decade Ago Thrive Amid Price Slump (BBG)

Oil production in some of the riskiest, highest-cost regions of North America is still thriving, even as the worst slump in a generation takes a bite out of U.S. shale. Onshore U.S. output is poised to drop 22% from last year through 2017, according to the Energy Information Administration. However, new volumes coming on stream from developments envisioned years ago in Canada’s oil sands and the U.S. Gulf of Mexico are limiting North America’s total production decline. Exxon Mobil is among companies bringing platforms online in the U.S. Gulf of Mexico from discoveries made in the past decade, which will help boost offshore output by 18% from last year to a record high in 2017, the EIA forecast this month. In the oil sands, developers including Canadian Natural Resources are also expanding projects, leading to a 16% increase over the same period, Canadian Association of Petroleum Producers data show.

Chicken and egg.

• Will the Fossil Fuel Industry Take the Rest of the Economy Down With It? (Ahmed)

[..] Some analysts believe the hidden trillion-dollar black hole at the heart of the oil industry is set to trigger another global financial crisis, similar in scale to the Dot-Com crash. Jason Schenker, president and chief economist at Prestige Economics, says: “Oil prices simply aren’t going to rise fast enough to keep oil and energy companies from defaulting. Then there is a real contagion risk to financial companies and from there to the rest of the economy.” Schenker has been ranked by Bloomberg News as one of the most accurate financial forecasters in the world since 2010. The US economy, he forecasts, will dip into recession at the end of 2016 or early 2017. Mark Harrington, an oil industry consultant, goes further. He believes the resulting economic crisis from cascading debt defaults in the industry could make the 2007-8 financial crash look like a cakewalk.

“Oil and gas companies borrowed heavily when oil prices were soaring above $70 a barrel,” he wrote on CNBC in January. “But in the past 24 months, they’ve seen their values and cash flows erode ferociously as oil prices plunge—and that’s made it hard for some to pay back that debt. This could lead to a massive credit crunch like the one we saw in 2008. With our economy just getting back on its feet from the global 2008 financial crisis, timing could not be worse.” Ratings agency S&P reported this week that 46 companies have defaulted on their debt this year—the highest levels since the depths of the financial crisis in 2009. The total quantity in defaults so far is $50 billion. Half this year’s defaults are from the oil and gas industry, according to S&P, followed by the metals, mining and the steel sector. Among them was coal giant Peabody Energy.

Despite public reassurances, bank exposure to these energy risks from unfunded loan facilities remains high. Officially, only 2.5% of bank assets are exposed to energy risks. But it’s probably worse. Confidential Wall Street sources claim that the Dallas Fed has secretly advised major U.S. banks in closed-door meetings to cover-up potential energy-related losses. The Fed denies the allegations, but refuses to respond to Freedom of Information requests on internal meetings, on the obviously false pretext that it keeps no records of any of its meetings. According to Bronka Rzepkoswki at advisory firm Oxford Economics, over a third of the entire U.S. high yield bond index is vulnerable to low oil prices, increasing the risk of a tidal wave of corporate bankruptcies: “Conditions that usually pave the way for mounting defaults—such as growing bad debt, tightening monetary conditions, tightening of corporate credit standards and volatility spikes – are currently met in the U.S.”

People’ll believe anything.

• SunEdison: Death Of A Solar Star (FT)

The triumphant email message pinged into SunEdison chief executive Ahmad Chatila’s inbox with only moments to spare. “We are approved by the Independent Cmte,” it said, confirmation that his over-indebted solar energy company would be able to cheat death — at least that day. The email brought news of approval for a cash transfer from TerraForm Global, a company controlled by SunEdison, enough to pay off a $100m margin loan due by 3pm that afternoon. The drastic action that SunEdison took that day in November allowed it to postpone default for several months, but the company was already sliding towards the biggest bankruptcy the renewable energy industry has ever seen. Its fate became a little clearer on Thursday when the world’s largest developer of renewable power projects filed for bankruptcy with debts of $16.1bn, and assets valued at $20.7bn.

The collapse is full of the usual cautionary tales, of corporate hubris and excessive debt, but also offers a new one in its industry: the dangers of financial engineering taken to extremes. In 2009 Mr Chatila took charge at MEMC, a struggling supplier of silicon wafers for chip and solar panels, and set about transforming the company. Through a series of deals, he built a solar power development business, and in 2013 changed the group’s name to SunEdison, after one of the acquisitions. From a low point in 2012, the shares rose 20-fold to peak at $32.13 in July last year. Since then, they have dropped by 99%. The past 12 months have been rough on many US solar power companies, including SunPower and Elon Musk’s SolarCity, but SunEdison is the only one to have blown up in such a spectacular fashion. The root cause of this is its complex financial structure.

Solar power is fundamentally a low-risk business. Developers, unlike their counterparts in oil and gas, do not have to explore to find resources, and they do not have to manage wild swings in product costs. Projects are typically signed up on 20-year contracts with fixed or predictably rising prices, and the global market is growing rapidly as falling costs make solar increasingly competitive against fossil fuels. The downside of that stability is a crowded market in which returns are generally low. Mr Chatila, however, was thinking big. In a presentation to analysts in February last year, he suggested SunEdison was taking a tilt at the world’s most valuable energy company, ExxonMobil. “Their market cap is around $400bn,” he said. “That’s what we’re going after.” SunEdison’s market capitalisation at the time was about $6bn. A blitz of deals, fuelled by soaring debts, was intended to bring the company closer to realising that ambition. Instead, it sent it plunging to earth.

Chinese will overpay by this much just to get money out of the country.

• The Inside Story Of Vancouver’s Wildest Property Deal (ZH)

It was in fall last year that Bruno and Peter Wall received an offer too good to refuse. The prominent Vancouver property developers behind Wall Financial Corporation had spent C$16.8 million (HK$102 million) to buy two ageing walk-up apartment blocks on adjacent lots on Nelson Street in 2013. They had big plans for the downtown site: a glittering 60-storey residential skyscraper, taking advantage of the location within the city’s West End Community Plan, where a building could rise 168 metres tall under new zoning. The project was dubbed “Nelson on the Park” and the Walls turned to favourite designer Chris Doray to come up with what they hoped would be a new Vancouver landmark. But now a consortium of investors was proposing something even more remarkable.

They would pay the Walls C$60 million for the site alone, which had just been valued at C$15.6 million by BC Assessment. The huge profit was impossible to resist, and the sale was completed in late January. Doray, a 25-year veteran of the Vancouver development scene whose design has now been shelved, said he was “astonished” by the transaction, which he said set a new benchmark for commercial real estate in the city. “The price on this block of land has now thrown everybody in the industry out of whack,” said Doray. “The property is worth, what, C$20 million, and somebody pays C$60million? One wonders what’s going on. Is this New York? Is this Hong Kong?” The scale of the purchase, orchestrated by Sun Commercial Real Estate (Suncom) – a firm that specialises in pooling wealthy investors from Vancouver’s Chinese immigrant community – was exceptional enough.

1059 Nelson Street in downtown Vancouver, where property developers Bruno and Peter Wall had once hoped to build a 60-story skyscraper.

But an investigation by the South China Morning Post now reveals the strange and frantic backdrop to the transaction – including a two-hour stampede by Suncom’s investors, desperate for a slice of the deal. It is a transaction that also sheds light on the rush of Chinese money fuelling Vancouver’s soaring real estate market. The Post interviewed key players and pored over land titles, company directorship and address changes, and English and Chinese social media postings to understand a transaction that looked, from the outside, incomprehensible – and potentially disastrous. But Suncom, whose activities are being reviewed by the BC Securities Commission, knew exactly what it was doing. Because on February 29, one month after taking ownership of the Nelson Street site, the Suncom consortium flipped it, corporate records show. The price was C$68 million. And the Post met the new buyer, a rich Chinese immigrant named Gao Shan, last month.

“While the IMF has demanded a restructuring of Greece’s debts, Germany has suddenly decided that no debt relief is needed at all. Still, it has insisted the IMF participate anyway.”

• Greece’s Debt Crisis Looks Familiar, But Consequences May Be Worse (FT)

While Europe’s political class has been consumed with preventing refugees from entering the EU and Britain from exiting, the mother of all EU crises has slowly and quietly been gathering steam again: Greece. Eurozone finance ministers will meet on Friday after yet another round of fruitless talks in Athens where almost nobody agreed on the way forward. And just like the Greek crisis that gripped the EU last year, there is a hard stop arriving very soon: unless Athens receives its next round of bailout aid, it risks defaulting on €3.5bn in debt payments in July, raising anew the agonising prospect of Grexit. How could this be happening again? After a series of increasingly desperate summits nearly a year ago, EU leaders agreed an €86bn bailout that pulled Greece back from the brink.

Just months later, a chastened Alexis Tsipras, the far-left prime minister who made his political bones railing against two similar EU rescues, won re-election promising to implement the harsh fiscal measures included in a third programme. European Commission officials were touting Mr Tsipras as a changed man; shorn of his ornery finance minister Yanis Varoufakis, Brussels convinced itself that the long-time radical had transformed into a diligent economic reformer. But they overlooked the political realities in Athens — not to mention the financial realities of the bailout. In fact, last summer’s deal was less a cure-all for Greece’s economic woes than a collective kicking of the can down the road. It avoided default by loaning Athens €13bn very quickly in exchange for a narrowly focused set of pension and tax reforms.

Even then, much of the heavy lifting was put off until the new programme’s first quarterly review — including the politically combustible issue of debt relief. As if to underline how ephemeral the deal was, the International Monetary Fund made clear it was not participating and would put off any decision on whether to join until it was certain Mr Tsipras, who had become the first leader of a developed country to default on an IMF payment, would live up to his commitments. That first quarterly review has now stretched into two additional quarters, and the three-dimensional stand-off between Athens, Berlin and the IMF has only deepened. While the IMF has demanded a restructuring of Greece’s debts, Germany has suddenly decided that no debt relief is needed at all. Still, it has insisted the IMF participate anyway.

Meanwhile, the IMF has decided the agreement reached in July was badly constructed and should have lower budget surplus targets. As for Mr Tsipras, he has returned to an angry, defensive crouch, railing against outside forces. There is little political capacity in Athens to push through additional reforms or spending cuts even if Mr Tsipras wanted to. “Europe’s politicians have been distracted with other challenges and markets have become complacent about the inherent risks in Greece’s new bailout,” said Mujtaba Rahman, head of European analysis at the Eurasia Group risk consultancy. “But if Berlin doesn’t revise its approach, this is going to blow up in everyone’s faces.”

The players, the arguments and even the choreography have changed little since last year. But the consequences of failure may have. A year ago, EU leaders felt confident they had ringfenced Greece and that a Grexit, while severely damaging to the Greek economy, would have little impact on the rest of the eurozone. Now, however, they are deeply worried about the prospect of a failed EU member state with 50,000 Syrian, Iraqi and Afghan refugees stuck in deteriorating camps — a state the rest of the bloc is looking to as a front line against the influx of migrants into Europe.

Succumbing to sadists.

• Lenders Tell Greece To Prepare Contingency Package Of Extra Reforms (R.)

International lenders asked Greece on Friday to prepare a package of additional savings measures which would be passed into law now but implemented only if needed, to make sure the country reaches agreed fiscal targets. Once agreed, the set of contingent reforms, together with measures already under negotiation, would enable the disbursement of new loans to Athens and pave the way for debt relief. The idea of a contingency package appears to end a long dispute between the eurozone and the IMF over whether Greece’s current reforms are enough. “We came to the conclusion that the policy package should include a contingent package of additional measures that would be implemented only if necessary to reach the primary surplus target for 2018,” the chairman of euro zone finance ministers Jeroen Dijsselbloem told a news conference in Amsterdam after the ministers met.

The contingency measures needed to be “credible, legislated up-front, automatic and based on objective factors.” Greek Finance Minister Euclid Tsakalotos said Athens could not legislate “contingent measures” as Greek law did not allow it. But Dijsselbloem said a way would be found. “We need to work on how that mechanism is going to look like. Of course if there are legal constraints we can’t and won’t break legal constraints. We will design it in a way that delivers credibility …and (is) legally possible,” Dijsselbloem told a news conference. The contingency package is to produce savings of 2% of GDP, on top of savings of 3% that are to come from reforms under negotiation now, Dijsselbloem said. The amount is the difference between euro zone and IMF forecasts of what primary surplus Greece is likely to achieve in 2018.

The current reforms include a pension and income tax reform, the setting up of a privatization fund and a scheme to deal with bad loans. The content of the contingency set is not decided yet. Agreement on both reform packages – the regular and the contingent one – would mean euro zone ministers would meet again on Thursday to approve the deal and have a “serious discussion” on debt relief for Greece. The prospect of debt talks may encourage Athens to back the new package, and lenders reminded their Greek counterparts that there are time constraints. “The liquidity situation is becoming tight, there are debt service payments … there is a risk that the government may have to accumulate domestic arrears again,” the head of the euro zone bailout fund Klaus Regling said.

It’s of little use to see this from an economic point of view; it makes no sense in that context. It’s purely a political power game, and economics are a side show at best.

• The Economic Consequences Of The Eurozone (Coppola)

The latest round of Greek bailout negotiations is going anything but smoothly. In fact, the growing rift between Greece’s European creditors – notably Germany – and the IMF threatens to derail them completely. The IMF estimates that the proposed 3.5% primary surplus would turn out to be more like 1.5%, making debt relief essential. But Germany insists that a 3.5% of GDP primary surplus could be sustained indefinitely with the right reforms and no debt relief will be needed. Deadlock. But now we learn that an additional set of “contingent reforms” is to be imposed on Greece. The draft Memorandum of Understanding already specifies spending cuts and tax rises to the tune of 3% of GDP: the new set would make savings of a further 2% of GDP. These contingent measures are currently unspecified: apparently the Greek government is to propose them.

Once specified, they would be passed into law by the Greek government, though they would not come into force unless “needed” (i.e. if Greece missed its fiscal targets). But of one thing we can be certain. They will not be reforms aimed at restoring the Greek economy. No, their sole purpose will be to extract yet more money from Greek households and businesses, to the detriment of the health and wellbeing of the Greek people and the profitability of Greek businesses. The combination of the MOU with the new measures is brutal. No way can a fiscal tightening of 3% of GDP, plus a further tightening of 2% when (not if) Greece misses its fiscal targets, do anything but further economic damage. There is no monetary offset to soften the blow, since Greece is excluded from the ECB’s QE.

A fiscal tightening of this magnitude without central bank support is the equivalent of doing major surgery without anesthetic. The patient may survive the surgery, but the pain and shock will set back its recovery by years. And the surgery is counterproductive, too. It will not ensure that the creditors get their money back more quickly. On the contrary, it may mean they never get it back. The more damage is done to Greece’s economy, the harder it will find it to pay its creditors. To quote the great American economist Irving Fisher, “The more the debtors pay, the more they owe”. Fisher’s “The Debt Deflation Theory of Great Depressions”, from which this quotation is taken, should be required reading for anyone involved in the Greek bailout negotiations. Greece’s depression is now deeper and longer-lasting than the USA’s Great Depression – and it is far from over.

“More than 3 million people have been displaced in the Lake Chad basin – in Nigeria, Niger, Cameroon and Chad – by violence by the militant group Boko Haram..”

• Refugee, Migrant Flow From Turkey To Greece Picking Up Again (Reuters)

The numbers of migrants landing in Greece from Turkey is starting to creep up again, showing efforts to close off the route are coming under strain, the International Organization for Migration (IOM) said on Friday. Around 150 people a day had arrived over the last three days, still way off the numbers seen a month ago, the organisation added, but showing an increase since an EU deal with Turkey deal to stem the flow. “The arrivals in Greece which were down to literally zero some days this month, are beginning to creep back up,” IOM spokesman Joel Millman told a Geneva news briefing. “It could be the weather, it could be any number of things, it could be that smugglers are getting more creative.” Europe signed an agreement with Turkey last month to close off the main route into Europe for more than a million people, most fleeing war and poverty in the Middle East, Asia and Africa.

NATO sent ships into Greek and Turkish waters in the Aegean in March, though Greek Prime Minister Alexis Tsipras said on Friday that Turkish demands were hampering the mission. “It could be that there is just still a lot of demand in Turkey … people have already spent months to get to Turkey and where there is a will and where there is means, people will try to satisfy them,” Millman told the briefing. “It still shows that hermetic sealing that seemed to be happening a month ago isn’t anymore.” There were also signs of increased numbers of people from sub-Saharan Africa taking the perilous route across the Mediterranean to Europe, he said. More than 3 million people have been displaced in the Lake Chad basin – in Nigeria, Niger, Cameroon and Chad – by violence by the militant group Boko Haram, he added.