William Henry Jackson Hand cart carry, Adirondacks, New York 1902

Marc Chandler says what I have said: it’s not about the energy, it’s about the financing. Which is vanishing from the shale patch. “The big risk now to our shale is not going to be that the price of oil drops so far that it’s not going to be profitable,” he said. “The weakness, the Achilles’ heel, is that they don’t get the cheap funding anymore.”

• This Is Oil’s ‘Minsky Moment’: Marc Chandler (CNBC)

Six years ago, the theories of economist Hyman Minsky were used to make sense of the collapse in housing prices, and its attendant effects on the economy. Today, Marc Chandler says the energy sector has just suffered its own Minsky moment. And while he doesn’t expect it to take down the stock market, the slide in oil could have a serious impact on the high-yield bond market. Minsky moment is a term coined by Pimco economist Paul McCulley in 1998, and it refers to a point when a period of rapid growth and risk-taking leads to a sudden turn lower and a crisis. Chandler, global head of markets strategy at Brown Brothers Harriman, says that is precisely what is happening in crude oil. “Many people a couple years ago, a year ago, were saying that oil prices could only go up—’we’re in peak oil’—meaning that we’re running out of the stuff. So a lot of things were leveraged based on oil prices that can only go up. Sort of like house prices—’they can only go up.’ So what happened is, because people held this as a deep conviction, they leveraged up,” Chandler said.”

In fact, the energy sector has borrowed $90 billion in the high-yield market since 2008, Chandler said, making energy producers “a large component of the high-yield market itself.” The problem is that “a lot of the loans, like loans on houses, were made not so much on a person’s ability to repay the loan as on the value of the house. Similarly, the banks and investors bought high-yield bonds or leveraged loans on the energy sector not on the basis of their ability to repay it, but on the value of the oil in the ground.” And so what happens now that crude oil has fallen nearly 40% from its June highs? Chandler foresees both further consolidation (along the lines of Halliburton’s acquisition of Baker Hughes) and failures ahead as the cheap financing dries up. “The big risk now to our shale is not going to be that the price of oil drops so far that it’s not going to be profitable,” he said. “The weakness, the Achilles’ heel, is that they don’t get the cheap funding anymore.” Or, to use a more modern metaphor: “This is sort of when Wile E. Coyote runs off the cliff.”

“[When] an individual fills up their automobile, there is not an extra $10 bill that shows up in their wallet, therefore, the incentive to spend really is not recognized and the ‘savings’ get washed within already tight consumer budgets ..”

• Cheap Oil’s Economic Benefits May Be A Big Myth (MarketWatch)

Cheap oil is awesome, right? Most economists describe it as a sort of tax cut for Americans at the gas pump. Even Larry Fink, a hot-shot Wall Street money manager, declared oil’s decline “spectacular.” “This is an incredible tax cut for Americans and everywhere else around the world,” Fink told CNBC Wednesday, referring to the startling plunge oil has seen in recent weeks. The cheap oil argument goes like this: consumers and businesses save in heating costs and in fueling their cars and those savings will be spent on discretionary items, fueling consumption. A recent article in the Washington Post indicated that Americans would pocket a $230 billion windfall, if prices stay at their current levels, compared to where they were in June.

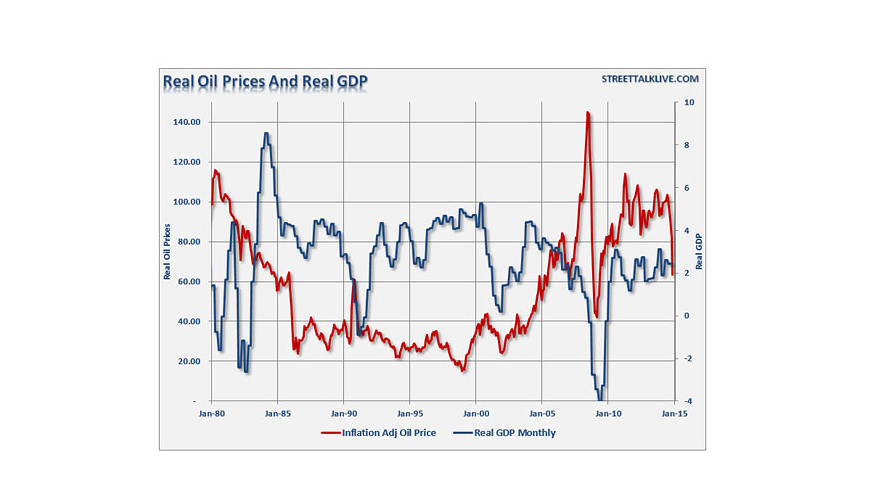

However, some financial experts argue that a decline in oil isn’t all that it’s cracked up to be. In fact, it could be a bad omen for the U.S. economy. Lance Roberts, Strategist for STA Wealth Management, said the idea that declining energy prices are good for the economy is wrong. “[When] an individual fills up their automobile, there is not an extra $10 bill that shows up in their wallet, therefore, the incentive to spend really is not recognized and the ‘savings’ get washed within already tight consumer budgets,” Roberts argued. It’s often noted that consumer spending accounts for about two-thirds of gross domestic product. But Roberts pointed out that history does not seem to support the idea that lower gasoline prices, and other cheaper energy costs, lead to higher consumer spending, as the following chart shows:

In fact, as Roberts attempted to illustrate in the chart below, sharp declines in energy prices have actually “been coincident with lower economic growth rates,” as he termed it. In other words, falling oil prices have typically been a harbinger of difficult economic times to come. Think of oil prices as a measure of the global economy’s blood pressure. While there has been a production glut, the strengthening dollar has also contributed to the dramatic drop in oil prices — and that rapidly rising dollar is a function of weakness elsewhere, particularly in Europe and Asia.

Everything’s on hold for US job numbers later today, but oil is at multi-year lows and slowly falling further this morning.

• Brent Drops From 4-Year Low as Saudi Discounts Deepen Price War (Bloomberg)

Brent extended losses from a four-year low as Saudi Arabia offered customers in Asia record discounts on its crude, bolstering speculation it’s defending market share. West Texas Intermediate dropped in New York. Futures fell as much as 0.8% in London and are headed for a second weekly decline. State-run Saudi Arabian Oil Co. cut its differential for Arab Light sales to Asia next month to $2 a barrel below a regional benchmark, according to a company statement. That’s the lowest in at least 14 years. The kingdom doesn’t want to subsidize Iran, Iraq and Venezuela and is willing to let the market decide prices, said Daniel Yergin, an energy analyst and Pulitzer Prize-winning author.

Crude slumped 18% last month as the Organization of Petroleum Exporting Countries maintained its output quota, letting prices decrease to a level that may slow U.S. production. Saudi Arabia has no price target and will let the market decide at what level oil should trade for now, said a person familiar with its policy. “It seems what the Saudis want, the Saudis are going to get,” Phil Flynn, a senior market analyst at Price Futures Group in Chicago, said by e-mail today. “We’re going to see prices continue to be under pressure. It is still game on.”

Great idea to add US oil to an already overloaded global market.

• Oil Drop Gives U.S. Drillers Argument to End Export Ban (Bloomberg)

Collapsing crude prices have given oil producers a new argument for ending a 39-year-old U.S. ban on exports. With U.S. output at a 31-year high and imports at the lowest level since 1995, producers seeking the best possible price for crude are straining at having to keep sales at home. Removing the ban could erase an imbalance between U.S. and foreign crude prices by expanding the market for shale oil. A 38% decline in crude prices since June, “will weigh into the debate” and help make the case to lift the export ban, said Senator Lisa Murkowski, the Alaska Republican poised to take over as head of the Energy and Natural Resources Committee next year. Lawmakers in Washington are set to hold a hearing next week on dropping the ban. Murkowski hasn’t decided yet whether she’ll introduce a bill to allow exports.

Republicans, who are slated to take control of both houses of Congress next year, have yet to reach consensus on what to do. The top House and Senate Republicans haven’t yet taken a position on the matter and some rank-and-file members, including Senator Susan Collins of Maine, say they are wary of action because of fears it may lead to higher gasoline and heating-oil prices. President Barack Obama’s former top economic adviser Lawrence Summers called for ending the ban in September after the Brookings Institution, a Washington policy group, released an analysis showing that exports would lower gasoline prices. White House Press Secretary Josh Earnest declined to say yesterday whether lifting the ban was being discussed or considered by the administration.

With falling oil prices, these projects loook ever more megalomaniacal. “Backers of LNG projects in British Columbia face higher costs than Gulf Coast proponents such as Sempra Energy because of the pipelines required across two Canadian mountain ranges, the lack of existing infrastructure on the Pacific Coast and negotiations with aboriginals.”

• Canada-U.S. LNG Rivalry Draws Focus After Petronas Delay (Bloomberg)

Petroliam Nasional’s deferred decision on a C$36 billion ($32 billion) liquefied natural gas project in British Columbia is bringing to the fore Canada’s struggle to compete with the U.S. on costs. Petronas, as the Malaysian state-owned producer is known, is pushing contractors to bring costs closer in line with U.S. rivals as it tries to keep the first exports to Asia on track to start by 2019, Michael Culbert, chief executive officer of the Pacific NorthWest LNG project, said. “We’ve got real competition that is coming out of the Gulf Coast projects,” Culbert said by phone yesterday, estimating U.S. suppliers can deliver LNG to Asia for $1 to $2 less per million British thermal units than Canadian projects. “With the changing oil prices, contractors may not be as busy as they thought they would be.” While U.S. terminals are already being built, none of the proponents in Canada have decided to proceed. Pacific NorthWest LNG would be the country’s first large project to come online among a handful put forward by Shell to Chevron.

Petronas joined BG Group in pushing back a decision on its plans in Canada as oil trades close to five-year lows. BG cited competition from U.S. supplies when it deferred its decision in October. Backers of LNG projects in British Columbia face higher costs than Gulf Coast proponents such as Sempra Energy because of the pipelines required across two Canadian mountain ranges, the lack of existing infrastructure on the Pacific Coast and negotiations with aboriginals. U.S. projects have caught up to Canadian rivals that received export approvals to start lining up buyers earlier and are now passing them by. Gulf Coast proponents adding export capabilities to existing LNG import terminals need less new equipment and have access to a network of pipelines already linked to vast supplies of gas in shale formations, as well as a larger labor pool.

Ambrose is right. All the speculation on ECB QE is more or less pointless, because Germany (re: the Bundesbank) is not likely to change its mind.

• ECB Paralyzed By Split As Irreversible Deflation Trap Draws Closer (AEP)

The European Central Bank has dashed hopes for quantitative easing this year and acknowledged for the first time that the institution’s elite board is split on plans for a €1 trillion liquidity blitz. Equity markets fell across southern Europe,with Italy’s MIB off 2.77pc, led by sharp falls in bank stocks. Spain’s IBEX dropped 2.35pc. The euro surged by more than 1pc to $1.2455 against the dollar in early trading as speculators rushed to cover short positions. Expectations for immediate stimulus had been riding high after the ECB’s president, Mario Draghi, pledged action “as fast as possible” last month. The bank slashed its forecasts for economic growth to 1pc next year, and admitted that inflation will remain stuck at just 0.7pc, a combination that traps large parts of southern Europe in deflationary slump and corrodes debt dynamics. BNP Paribas said eurozone inflation is likely to average 0pc in 2015, after turning negative this month.

“The ECB’s measures are woefully behind the curve,” said Ashoka Mody, a former EU-IMF bailout chief now at the Bruegel think-tank in Brussels. “For anyone who wants to see it, a debt-deflation cycle is ongoing in the distressed economies. The authorities have very nearly lost control of a process that will become ever harder to manage as it becomes more entrenched,” he said. Mr Mody said the ECB repeatedly asserts that it will act “if needed” but declines to spell out what that means and why it continues to delay when the inflation level – now 0.3pc – is already so far below target. “Cheap talk is a legitimate policy tool. But talk can also create a cognitive bubble,” he said. Mr Draghi denied that the ECB is complacent about the deflation risk or that is succumbing to paralysis. “Let me be absolutely clear. We won’t tolerate prolonged deviation from price stability,” he said.

Yet he pleaded for more time to study the effects of the oil price crash and gave a strong hint that there would be no further decisions on monetary stimulus until after the next meeting in January. The governing council discussed possible purchases of every major asset “other than gold” but has not yet agreed to go beyond the current mix of covered bonds and asset-backed securities. “The credibility of the ECB lies in tatters. It’s now patently clear that Draghi lacks the crucial German support for launching full-blown QE,” said sovereign bond strategist Nicolas Spiro. Mr Draghi insisted that the bank could in principle ram through the QE decision by majority vote but said he was “still confident” that a package of measures could be designed to keep everybody on board.

The oracle leaks lubricant.

• Greenspan Says He Would Pre-Empt Asset Bubbles Financed by Debt (Bloomberg)

Former Federal Reserve Chairman Alan Greenspan, who was blamed by some economists for overheating equity and housing prices in the 1990s and 2000s, said that were he in the job today, he would take pre-emptive action to tackle asset bubbles if they were financed by leverage. Greenspan, who argued in office that it was better to clean up after an asset bubble had burst rather than artificially prick it, told delegates at a conference hosted by Citigroup Inc. in London today that he believed that argument is correct when a speculative boom isn’t financed by debt, mentioning the 1987 stock market crash as an example. If the overheating was caused by leverage, however, “then you’re going to have problems,” he said. “Bubbles are aspects of human nature and you can try as hard as you like, you will not alter the path,” Greenspan told the audience at Citigroup’s European Credit Conference via a video link from Washington.

“I still hold to the general view that unless you have debts supporting the bubble, I would just let it alone because certain things about human nature cannot be changed and I’ve come to the conclusion this is one of them.” The former Fed chairman, who warned against “irrational exuberance” in stock markets as early as 1996, was faulted by some economists for not using higher borrowing costs to prevent equity prices from rising before the bursting of the so-called tech bubble in 2000. He cut interest rates afterwards to “mop up” the damage, which some analysts said led to an overheating in the housing market that partly caused the financial crisis. Greenspan remained unapologetic about the tech bubble, saying in a December 2002 speech that central banks had “little experience” in dealing with market bubbles and that “dealing aggressively with the aftermath of a bubble” was “likely to avert long-term damage.”

Yeah, that’s a really important topic. Bragging rights in the glue factory.

• US Economy Still Bigger, But China’s More Crucial (MarketWatch)

Commentary was ablaze Thursday over new data suggesting China now makes up a larger portion of the world economy than the U.S., or at least when adjusted to reflect purchasing power. The numbers — published by the International Monetary Fund — had folks from Nobel laureate economist Joseph Stiglitz to MarketWatch columnist Brett Arends declaring the end of the U.S. as the top economic power, while others such as Harvard professor and former Clinton Administration advisor Jeffrey Frankel, argued that America was still on top. But while most economic analysis would still put the U.S. comfortably atop the world rankings, HSBC economist Frederic Neumann said that the real lesson of the IMF data was that China, and emerging Asia as a whole, has become more crucial to the global economy.

In a report Friday, Neumann noted that if you adjust this year’s gross domestic product data for purchasing parity (smoothing out foreign-exchange differences by making the price of products the same in each country), not only is China bigger than the U.S., but the emerging economies of Asia would be bigger than those of the U.S. and euro zone combined. “But that’s not necessarily the right measure to look at to gauge a market’s importance to the world,” Neumann wrote. “Here, international purchasing power matters, and that is best captured by looking at GDP in U.S. dollars.” In other words, an economy’s influence must be measured by what it’s worth globally, not just in its own currency. So if you look at nominal dollar-denominated GDP, the U.S. makes up 22% of the world’s total, while the euro zone is 17%, and China is 11%. “But that’s not to dismiss the growing importance of Asia,” the HSBC economist wrote. “For one, emerging Asia’s combined U.S.-dollar GDP will pull equal to that of the U.S. for the first time this year.”

We know. That’s why we call BS on ‘growth’.

• Wage Growth Stuck Below Pre-Crisis Levels (CNBC)

Stagnant wage growth in developed countries has pulled average global earnings lower and is in danger of dragging economic performance down, according to the International Labour Organization (ILO). In its latest report published Friday, the ILO said that global wage growth in 2013 slowed to 2%, from 2.2% the year before. As such, pay growth has a significant way to go before it reaches its pre-crisis level of around 3%. The average rate was pulled down by stagnant pay in developed countries, the organization said. Annual wage growth in these economies had been around 1% since 2006, but fell to just 0.1% in 2012, and 0.2% in 2013. Wage growth in developed countries was hit hard by the recent economic crisis, which saw employers become reluctant to increase workers’ pay. Over the past few years, as nascent recoveries took hold in major economies including the U.S. and U.K., pay increases have lagged broader economic growth.

It’s an issue that will be in focus on Friday, when the U.S.’s non-farm payrolls numbers are released. The unemployment rate is expected to be unchanged at 5.8%, according to Reuters, but analysts are hoping for a slight increase in wages – a key measure for the Federal Reserve in considering when to raise interest rates. “Wage growth has slowed to almost zero for the developed economies as a group in the last two years, with actual declines in wages in some,” Sandra Polaski, the ILO’s deputy director-genera for policy, said in a release. “This has weighed on overall economic performance, leading to sluggish household demand in most of these economies and the increasing risk of deflation in the euro zone.” By contrast, pay growth in emerging countries has stormed ahead over the last two years, according to the ILO, coming in at 6.7% and 5.9% in 2012 and 2013 respectively.

That’s how they get their ‘recovery’.

• British Workers Suffer Biggest Real-Wage Fall Of Major G20 Countries (Guardian)

British workers suffered the biggest fall in real wages of all major G20 countries in the three years to 2013, according to the International Labour Organisation (ILO). They fared worse in terms of falling real pay than all of the bailed-out eurozone economies – Portugal, Spain and Ireland – apart from Greece. Wages in Japan and Italy also fell over the period but at a slower rate than in the UK, while real terms pay increased in the US, France, Germany, Canada and Australia. Patrick Belser, senior economist at ILO and author of the report, said: “In the UK in 2008 there was some positive growth of real wages whereas some other countries had stagnant or declining wages – such as Japan. Then what you see subsequently is a continuous fall in wages to 2013. We expect wages to be at best flat this year, and they will most likely decline.”

The biggest fall in UK wages adjusted for inflation came in 2011, when they fell by 3.5%. In Italy, which was one of the countries hit hardest by the eurozone crisis, real pay fell by only 1.9%. Last year real UK pay fell by 0.3% according to the ILO, compared with a 2% increase globally. Real wages in the UK have fallen consistently since 2008, with inflation outpacing pay rises an economic recovery and recent rapid falls in unemployment. In the UK, but also in Greece, Ireland, Italy, Japan and Spain, average real wages in 2013 remained below their 2007 level. Belser said weak productivity was part of the story in the UK. The Bank of England said in its latest quarterly inflation report last month that recent employment growth had been concentrated among young, lower-skilled and lower-paid workers, which was probably dragging down average wage growth. Weaker-than-expected pay growth in Britain has also generated lower than expected tax revenues for the government, which in turn has slowed deficit reduction.

“One thing is for sure – if we move in anything like this direction, whilst continuing to protect health and pensions, the role and shape of the state will have changed beyond recognition.”

• ‘Colossal’ Cuts To Come, Warns UK Institute For Fiscal Studies (BBC)

The plans set out by George Osborne in the Autumn Statement on Wednesday will require government spending cuts “on a colossal scale” after the election, an independent forecaster has warned. The Institute for Fiscal Studies (IFS) said just £35bn of cuts had already happened, with £55bn yet to come. The detail of reductions had not yet been spelled out, IFS director Paul Johnson said. As a result, he said it would be wrong to describe them as “unachievable”. However, voters would be justified in asking whether the chancellor was planning “a fundamental reimagining of the role of the state”, Mr Johnson told a briefing in central London on Thursday.

If reductions in departmental spending were to continue at the same pace after the May 2015 election as they had over the past four years, welfare cuts or tax rises worth about £21bn a year would be needed by 2019-20, at a time when the Conservatives were committed to income tax cuts worth £7bn, according to the IFS. Mr Johnson added: “One thing is for sure – if we move in anything like this direction, whilst continuing to protect health and pensions, the role and shape of the state will have changed beyond recognition.”

What a great idea with oil moving towards $50. Does that mean they’ll get more of our money?

• North Sea Oil Exploration To Be Allocated UK Taxpayers’ Money (Guardian)

Taxpayers’ money could be channelled directly into North Sea oil exploration under a scheme announced to the industry in Aberdeen on Thursday by Danny Alexander, chief secretary to the Treasury. The promise to give financial support for seismic surveys was one of a number of tax and other benefits proposed by the government in an attempt to halt a collapse in exploration and remedy a fall in production. The moves were welcomed by the offshore industry but criticised by environmentalists as “environmental and economic illiteracy of the highest order”. Alexander said it was right to give targeted support to Scotland’s oil and gas industry building on tax reductions and other moves made in the autumn statement on Wednesday.

“We’re incentivising and working with the industry to develop new investment opportunities and support new areas of exploration. This will help ensure that the industry continues to thrive and contribute to the economy,” he explained. Other North Sea countries including Norway and Holland provide seismic incentives but they are new in the UK. Mike Tholen, economics and commercial director at lobby group Oil & Gas UK, said the allocation was expected to be a few millions of pounds rather than billions and to be matched by companies. It would be targeted at areas that would otherwise not be explored. “It is small beer financially but it is important because it is government putting its money where its mouth is,” he said.

Friends of the Earth said it was extraordinary that the government was trying to squeeze as much oil out of the North Sea as it could while the international community was trying to agree a plan during world climate talks in Lima, Peru to head off the threat of catastrophic climate change. Craig Bennett, the organisation’s policy and campaigns director, said: “This is environmental and economic illiteracy of the highest order. Ministers must end their obsession with dirty fossil fuels and build a clean economy for the future based on energy efficiency and the nation’s huge renewable power resources.”

As the western press tries to make the most out of Poland’s fear of Putin, they have other things on their mind.

• Poland More Worried About Europe Than Russia (CNBC)

With Russia and Ukraine for neighbors, Poland’s economy is feeling the heat from the geopolitical crisis but government officials said insist the country was a bright spot in a bad neighborhood and that the euro zone was more of a concern than Russia. “Sanctions are felt across the board, exports to Ukraine are down 25% and to Russia they’re down 10%,” Krzysztof Rybinski, the former deputy governor of the Polish Central Bank, told CNBC Friday. “But I don’t think investors will pull the plug on Poland unless Russia does something really unpredictable.” For Poland the euro zone slowdown was more of a worry. “For the Polish economy it’s much more important what happens in the west, if there is no growth, stagnation and recession in the west it will take us down with the situation.

Russia and Ukraine together are only about 7.5% of Polish exports – that’s significant but not as much as (our exports to) Germany.” Sanctions in Russia and the conflict in Ukraine, coupled with sluggish growth in the euro zone have had a “chilling” effect on Central Eastern Europe, with Poland no exception. Despite credit rating agency Moody’s saying that Poland’s economy had shown “resilience in times of stress” the country’s gross domestic product has declined. The economy grew by 2.0% in 2012, but grew 1.6% last year, according to EU statistics service Eurostat. Rybinski said there had been some positive effects of the sanctions on Russia, however. “We have many Ukrainian young people flowing through the border to Polish universities, this is a positive effect of sanctions. Other positive effects are that the zloty (the Polish currency) is not very strong which is helping Polish exporters,” he said.

Without that bailout, the markets will attack Greece once again.

• Eurozone Mulls Longer Greek Bailout, But Athens Refuses (Reuters)

Euro zone ministers are considering extending Greece’s bailout by six months to mid-2015, according to a document obtained by Reuters, but Athens said it was only willing to consider an extension of a few weeks to the unpopular program. Extending the program beyond a few weeks into the new year would complicate Prime Minister Antonis Samaras’ efforts to secure victory for his preferred candidate in a presidential vote in February. He had depended on exiting the EU/IMF bailout by the end of the year, when funding from the EU is due to end. “Greece has not received any written proposal on an extension,” a government official told Reuters. “In any case, everything that the prime minister and Finance Minister (Gikas) Hardouvelis has said stands – that Greece can discuss only a technical extension, which cannot be longer than a few weeks.”

An extension of the bailout, under which Athens will have received a total of €240 billion ($300 billion) since 2010, is necessary because international lenders and the Greek government are still negotiating what Athens must do to get the remaining €1.8 billion and secure a back-up credit line for after the bailout ends and Greece returns to market financing. Athens needed to wrap up its bailout review by a meeting on Dec. 8 of euro zone ministers to meet the timeline for exiting by the end of the year. But the talks have been held up by a row over a budget shortfall next year, and a senior euro zone official on Wednesday said Greece would have to ask for an extension on its bailout because a credit line to replace the program will not be ready in time. Euro zone officials are now urging the country to reach a deal by Dec. 14, a Greek finance ministry official said.

Stop pretending already. There is no cure for Japan.

• Japan Pension Fund Head Calls for $389 Billion Stock Revamp (Bloomberg)

Japan’s Government Pension Investment Fund is considering whether to overhaul its $389 billion of stock investments by loosening rules that restrict managers to domestic or international equities. A month after the $1.1 trillion pool unveiled plans to more than double local and foreign share targets so that each makes up 25% of assets, Takahiro Mitani, its president, said separating the world into Japan and everywhere else may not be the best approach. GPIF should consider letting some of its managers invest both at home and abroad, he said. “More funds are investing without discriminating between domestic and foreign, and I think that’s worth considering,” Mitani, 65, said in an interview in Tokyo on Dec. 3. “If choosing between Toyota and Volkswagen, instead of being limited to just Toyota and Nissan, raises investment performance and efficiency, it’s an option we mustn’t rule out.”

The California Public Employees’ Retirement System, the biggest U.S. public pension, makes no distinction between local and foreign holdings. Calpers, which oversees about $295 billion, has a 51% target for public equities, according to its website. GPIF’s stock investments were parceled out to managers in 45 different pieces as of March 31, according to the fund’s annual report. The Topix index rallied 8.4% since GPIF announced the investment strategy changes on Oct. 31. The Bank of Japan unexpectedly expanded its bond buying to 80 trillion yen ($666 billion) a year on the same day, as it targets annual inflation of 2%. The extra purchases helped drive yields on benchmark 10-year notes down by 3.5 basis points to 0.435% yesterday, after touching a more than 1 1/2-year low at the end of November. The Topix rose 0.4% at today’s close to extend a seven-year high. The yen fell 0.3% to 120.01 per dollar.

GPIF would have to revise its systems to allow one manager to invest across Japanese and non-domestic shares, Mitani said. Alternatively, it could create a new global stock class on top of the existing ones, he said. The fund is due to review foreign equity managers in about 18 months, according to Mitani, who said he plans to retire when his five-year term finishes at the end of March.

And this is what you get, Mr. Pension fund head: ” .. 37% of Japan’s yen-denominated wealth has gone up in smoke ..” Abenomics equals desperation.

• The Japanese Government Bond Market Is Dead. And the Yen? (Wolfstreet)

[The BOJ’s] relentless bid has driven yields to near zero, now increasingly for longer-dated maturities as well. In this process, the Bank of Japandemonium, as I’ve come to call it, has tightened its iron grip on the government bond market to where the market ran out of air and died. Takeshi Fujimaki, an opposition lawmaker, explained the phenomenon this way:

The BOJ used consumer prices as an excuse to add stimulus and continues to hide that it’s monetizing government debt. But the truth is that Japan will default unless the BOJ continues to buy JGBs even after inflation accelerates beyond its intended target.

Alas, to monetize ever larger portions of government debt, the BOJ is selling freshly printed yen into a market it can manipulate but not control: the global currency market. Once big players around the world start dumping the yen, and once scared Japanese folks start dumping their yen too, the yen might do what the ruble is doing now: spiraling down uncontrollably. When Abenomics became a noun in late 2012, it took ¥75 to buy $1. Today it takes ¥120. With the effect that 37% of Japan’s yen-denominated wealth has gone up in smoke. But once the BOJ decides that the yen has fallen enough, it might not be able to stop its fall. It would have to sell its international reserves and buy yen – the opposite of QE.

If it decided to buy yen, instead of printing yen, to prop up the currency, it would thereby surrender control over the government bond market. The relentless bid would disappear even as the flood of new JGBs would continue. There would be no other buyers, not with yields at near zero. Chaos would break out instantly. The BOJ might try for a minute or two, and it might try to talk up the yen, but it can’t actually prop up the yen with yen purchases without causing JGBs to spiral out of control, which it would never allow to happen. It would never allow a debt crisis to throw Japan into chaos. Instead, it will continue to guarantee the nominal value of the debt by buying up every JGB that comes on the market, while keeping yields at near zero. And to heck with the yen. Fujimaki sees ¥200 to the dollar.

Good point.

• Companies Don’t Need Banks for Bank Loans (Bloomberg)

A while ago U.S. banking regulators announced guidelines to prevent banks from making loans to companies at more than six times Ebitda, because the regulators thought those loans were too risky. More recently those regulators have announced, roughly once a week, that they intend to enforce those rules, but for real this time. Here is a Wall Street Journal story about how private-equity firms – whose buyouts tend to be funded by leveraged loans – are adapting to those rules. Here is one funny way to adapt:

Private-equity firms have used adjustments in their models that contribute to a company’s earnings, thereby decreasing the leverage ratio and lifting a company’s future cash flow, a measure regulators use to calculate a company’s ability to repay debt. Vista Equity Partners adjusted Tibco Software’s Ebitda for the 12 months to Aug. 31 by 58%, to $378 million, from Tibco’s own calculation of $239 million.

This is an admirable strategy: If you want to borrow 8.5 times as much money as you make in a year, then that’s bad. One way to fix that is to borrow less money, but that is no fun. Another way to fix it is to make more money, but that is hard. A third way to fix it is to cross out the number of dollars that you make in a year and write a different number, and, boom, now you are borrowing 5.3 times Ebita. (Yes yes yes Vista “factored in cost savings” that the buyout would generate.) I don’t know how popular that strategy is.

The more interesting adaptation strategy is direct syndication. The thing is, most leveraged loans don’t come from banks. When a company does a leveraged loan, a bank will normally arrange the loan, and lend some of the money, but typically most of the money will come from other investors: hedge funds, mutual funds, collateralized loan obligations, etc.3 In the modern leveraged-loan market — much like in the stock and bond markets — banks are mostly intermediaries, matching companies that want to borrow with investors who want to lend. Those investors can still lend. The banks can’t. (I mean, they can, but the regulators will make sad faces at them.) But statistically the banks weren’t lending that much anyway. They were calling up the investors who were actually lending, but banks don’t have a monopoly on telephones.

Everyone seems to be gambling on Russians dumping Putin in hard times, but why should they?

• Putin Warns Russians Of Hard Times Ahead (BBC)

President Vladimir Putin has warned Russians of hard times ahead and urged self-reliance, in his annual state-of-the nation address to parliament. Russia has been hit hard by falling oil prices and by Western sanctions imposed in response to its interventions in the crisis in neighbouring Ukraine. The rouble, once a symbol of stability under Mr Putin, suffered its biggest one-day decline since 1998 on Monday. The government has warned that Russia will fall into recession next year. Speaking to both chambers in the Kremlin, Mr Putin also accused Western governments of seeking to raise a new “iron curtain” around Russia. He expressed no regrets for annexing Ukraine’s Crimea peninsula, saying the territory had a “sacred meaning” for Russia.

He insisted the “tragedy” in Ukraine’s south-east had proved that Russian policy had been right but said Russia would respect its neighbour as a brotherly country. Speaking in Basel in Switzerland later, US Secretary of State John Kerry said the West did not seek confrontation with Russia. “No-one gains from this confrontation… It is not our design or desire that we see a Russia isolated through its own actions,” Mr Kerry said. Russia could rebuild trust, he said, by withdrawing support for separatists in eastern Ukraine.

This has many European countries worried.

• Finns Who Can’t Be Fired Show Debt Trap at Work (Bloomberg)

Finland is a nice place to be if you work in the public sector. But laws that protect municipal workers from the hard reality of a faltering economy are adding to the debt burden in a country that had its credit rating cut just two months ago. In some towns, no public-sector staff can be fired until as late as 2022. Meanwhile, Finnish local government debt has tripled to €16.3 billion ($20 billion) since 2000. It will grow by another €10 billion by 2018, the Finance Ministry estimates. “The government and municipalities have the same problem: the income base has collapsed while expenses have continued to grow,” Anssi Rantala, chief economist at Aktia Bank Oyj, said by phone. As more people retire than join the workforce, Finland’s recession shows no sign of easing.

Prime Minister Alexander Stubb has described the country’s plight as a “lost decade” as manufacturing fails to spur growth for a third consecutive year. Adding to the country’s woes is the economic pain spreading through its eastern neighbor as exports to Russia collapse. In October, Standard & Poor’s cut Finland to AA+ from AAA as the state’s debt exceeds the 60% limit to gross domestic product permitted inside the European Union. As the government struggles to squeeze more competitiveness out of its labor force, existing laws are hampering its efforts. Many municipal employees enjoy a five-year immunity in case their town is merged with another. Among Finland’s 320 towns, the smallest ones may merge several times – giving those workers another five years of job protection each time.

Francis has guts. He fired the head of the Swiss guard as well yesterday. But money is a topic that can draw especially harsh responses, certainly when it’s a lot. And the Vatican has an awful lot.

• Vatican Finds Hundreds Of Millions Of Euros ‘Tucked Away’ (Reuters)

The Vatican’s economy minister has said hundreds of millions of euros were found “tucked away” in accounts of various Holy See departments without having appeared in the city-state’s balance sheets. In an article for Britain’s Catholic Herald Magazine to be published on Friday, Australian Cardinal George Pell wrote that the discovery meant overall Vatican finances were in better shape than previously believed. “In fact, we have discovered that the situation is much healthier than it seemed, because some hundreds of millions of euros were tucked away in particular sectional accounts and did not appear on the balance sheet,” he wrote. “It is important to point out that the Vatican is not broke … the Holy See is paying its way, while possessing substantial assets and investments,” Pell said, according to an advance text made available on Thursday.

Pell did not suggest any wrongdoing but said Vatican departments had long had “an almost free hand” with their finances and followed “long-established patterns” in managing their affairs. “Very few were tempted to tell the outside world what was happening, except when they needed extra help,” he said, singling out the once-powerful Secretariat of State as one department that had especially jealously guarded its independence. “It was impossible for anyone to know accurately what was going on overall,” said Pell, head of the new Secretariat for the Economy that is independent of the now downgraded Secretariat of State. Pell is an outsider from the English-speaking world transferred by Pope Francis from Sydney to Rome to oversee the Vatican’s often muddled finances after decades of control by Italians.

Pell’s office sent a letter to all Vatican departments last month about changes in economic ethics and accountability. As of Jan. 1, each department will have to enact “sound and efficient financial management policies” and prepare financial information and reports that meet international accounting standards. Each department’s financial statements will be reviewed by a major international auditing firm, the letter said. Since the pope’s election in March, 2013, the Vatican has enacted major reforms to adhere to international financial standards and prevent money laundering. It has closed many suspicious accounts at its scandal-rocked bank. In his article, Pell said the reforms were “well under way and already past the point where the Vatican could return to the ‘bad old days’.”