G.G. Bain Political museums, Union Square, New York 1909

“Now we’ve reached the bottom 40% of Americans, but guess what? We’ve run out of stuff. Sorry guys, you get nothing.”

• It’s Wealth Inequality That Drags Down The Economy (WaPo)

Let’s imagine that there are just 100 people in the United States. The richest guy – and, yes, he’s probably a guy – owns more than one-third of the total wealth in this country. He’s got a third of all the property, a third of the stock market and a third of anything else that can be owned. Not bad. The next-richest four people together own 28% of all the stuff. Divvied up four ways that’s still not too shabby. The next five people together own 14% of all the things, and the next 10 own another 12%. We’ve accounted for just 20% of the people, but nearly 90% of the total wealth. 90%! You can probably tell where this is going. The next 20% of people have only nine% of the wealth to split among them. Not great, but they’re still doing a lot better than the 60% of people below them.

The next 20% – the middle wealth quintile – only have 3% of the wealth to split 20 ways. Now we’ve reached the bottom 40% of Americans, but guess what? We’ve run out of stuff. Sorry guys, you get nothing. In fact, Wolff calculates that this bottom 40% actually has an overall negative net worth, which means that they owe more money than they own – and they probably owe that money to somebody in that top 5% or 10%. You’re not necessarily living in squalor if you have a negative net worth. For instance, some student loans and a brand-new mortgage will probably put you in that category. But if you’ve got a bachelor’s degree, a job and a house to show for it, you’re probably doing okay.

But plenty of folks will be stuck in that bottom 40% category forever. And as the OECD report points out, this is a big problem for everyone — even the top 1%. Their data shows that more inequality equals less economic growth: Between 1985 and 2005, the OECD estimates that increasing inequality has knocked nearly 5 percentage points off growth in OECD countries. If you’re one of the fortunate ones with money in the bank, you can think of this as a five% smaller return on your investment over that period, simply because the less fortunate aren’t able to contribute to the economy as much as they could otherwise.

Read more …

Much of it used to buy their own stock. The snake-eats-tail economy.

• US Companies Owe $1.267 For Every Dollar Of Earnings (Bloomberg)

A dark shadow is lurking behind the happy façade of rising stock prices. U.S. companies are borrowing money faster than they’re earning it – and they’re doing it at the quickest pace since the aftermath of the financial crisis. Instead of deploying the debt to build factories, hire new workers or expand product lines, companies are funneling more of their money to shareholders or using it to fund deals. Stock buybacks reached an all-time high last year and the volume of global mergers and acquisitions announced so far this year would make it the second-busiest ever, according to data compiled by Bloomberg. The debt undermines future growth and could dent company income when borrowing costs rise. Higher interest rates will make already indebted companies less desirable to lend to.

The consequence: profitability, buoyed by cheap money since rates went to near-zero in 2008, will sink. “Companies have said, ‘We don’t have an ability to grow organically, so we can distract shareholders instead,’” according to Jody Lurie, a credit analyst at Janney Montgomery Scott LLC, which manages $63 billion. “When they buy back shares, all it does is optically make earnings per share look better.” As recently as last year, companies in the Standard & Poor’s 500 Index had the lowest net-debt-to-earnings ratio in at least 24 years. Examining a slightly different universe – companies, excluding financial firms, with top credit ratings who’ve issued debt – the median net leverage in the first quarter of 1.267 was the highest since 2010 and up from 0.927 in the first quarter of 2014.

The leverage figure means companies owe $1.267 for every dollar of earnings after subtracting cash on hand. Companies reacted to the Federal Reserve’s rumblings about raising interest rates by going on a borrowing spree. “There are a lot of pressures on management to lever up to improve returns,” said Charles Peabody of Portales Partners. “They’ve taken on more leverage because the cost of transactions is very low. If that changes because rates go up, it’s going to be hard to sustain that gain.” Investment-grade non-financial companies issued $366 billion in bonds in the past two quarters. The $194.6 billion they sold in the first quarter was the most in history, according to data compiled by Bloomberg.

Read more …

Yield chasing.

• BofA Explains How the Bond Rout Could Turn Into a Bloodbath (Bloomberg)

The good news is investors are finally shaking off fears of economic stagnation worldwide. The bad news is this is brutal for credit markets. Prices on U.S. investment-grade bonds have fallen 1.1% in the first two days of June, a pace so fast it’s reminiscent of the notes’ 5% selloff in two months in 2013 when speculation emerged that the Federal Reserve was poised to scale back its bond buying. Bank of America strategists see the pain deepening from here. The reason? Investors who like these bonds tend to prize safety and reliable returns above all. They plowed into corporate bonds, often instead of more-creditworthy notes such as U.S. Treasuries, for higher yields as the Fed purchased debt and held interest rates at record lows to ignite growth.

These buyers, in particular, don’t like to see losses on their monthly mutual-fund statements. When the prospects for their debt look shaky, they’ve often responded by yanking their money. And that’s what they’ll likely do now, according to Bank of America analysts. “We expect high-grade fund flows to turn generally negative in line with the initial experience during the Taper Tantrum,” Hans Mikkelsen, a strategist in New York, wrote “Corporate bond prices are declining at a pace eerily similar to what we saw” during that selloff of 2013. That year, U.S. bond funds reported record withdrawals as investors girded for a period of steadily rising debt yields – or, in other words, losses. Investors pulled more than $70 billion from bond mutual funds in 2013, according to TrimTabs.

Of course, the exodus proved premature. Top-rated corporate bonds have returned 7.6% since the end of 2013 as oil prices plunged and ECB stimulus sent yields down globally. Now, however, there are signs that the American economy is finally improving enough for the Fed to raise rates as soon as this year. Yields on 10-year Treasuries are approaching the highest since November, making them a more attractive alternative to corporate debt for buyers looking for the safest source of income.

Read more …

“You want to shove rates down to zero, people are going to make big bets because they don’t think it can last; Every move becomes a massive short squeeze or an epic collapse..”

• Bond Rout Wipes Out 2015 Gain as Traders Fret Even Leaving Desks (Bloomberg)

The global bond market selloff has erased all of this year’s gains as historic market moves from Germany to the U.S. and Japan whipsaw traders. After being up as much as 2.3% as of mid-April, the BoAML Global Broad Market Index of bonds with a total face value of $41 trillion is now down 0.4% for the year. Bond traders have been caught off guard by signs the worldwide economy is likely to avoid mass deflation and by improvement in the euro zone’s economy, leaving little incentive to own debt securities with yields that in some cases are below zero. The latest leg lower in bonds came Wednesday, when ECBPresident Mario Draghi said investors should get used to the heightened volatility they’ve seen in recent weeks.

“This is sheer panic in the market from the standpoint of what’s been happening in Europe,” said Thomas di Galoma at ED&F Man Capital Markets in New York. “Most of Wall Street is guarded here as far as taking on new positions.” Like many of his peers around the world, di Galoma said he has had to cancel meetings as yields rose ever higher through key levels that many thought would attract demand, but didn’t. Take the yield on the benchmark 10-year German bund: it soared to as high as 0.94% Thursday as of 7:18 a.m. in London from as low as 0.049% on April 17. During the same period, the yield on similar maturity Treasuries surged to as high as 2.39% from 1.84%. The U.S. yield was little changed at 2.38% in London trading.

At a conference in Cambridge, Mass., Michael Lorizio said he couldn’t keep his eyes away from his phone, where price alerts were announcing a crash in German bond prices. He said he skipped out early from the networking session, and headed back to his office in Boston. “I couldn’t pay attention to any of the content, I was just watching the price action,” said Lorizio, at Manulife. “You’ve had to be a little more decisive because prices are moving very quickly.” At a news conference in Frankfurt Wednesday after an ECB policy meeting, where it didn’t even change rates, Draghi suggested several reasons for the rout in bonds. He cited including an improving economic and inflation outlook in the euro area, heavier issuance, volatility, poor market liquidity and an absence of certain investors.

Draghi, the architect of a €1 trillion bond-buying program, is an unlikely foe of the bond market. Quantitative easing provides an almost endless source of demand for bonds and should keep yields low. Instead, it’s made investors overly sensitive, said Jim Bianco, president of Bianco Research LLC in Chicago. “You want to shove rates down to zero, people are going to make big bets because they don’t think it can last,” Bianco said. “Every move becomes a massive short squeeze or an epic collapse – which is what we seem to be in the middle of right now.”

Read more …

“There’s a huge selloff all over the world..”

• Bond Slump Deepens as Europe Shares Slide With Metals, Oil (Bloomberg)

The global bond rout gathered pace, with Japanese notes and German bunds slipping a fourth day after Mario Draghi forecast faster euro-area inflation and continued market volatility. European shares slid with oil and metals as the Aussie declined. Yields on 10-year German government bonds climbed 2 basis points to 0.9% by 8:13 a.m. in London. The Japanese rate rose 3 basis points to 0.49% and Australia’s topped 3% for the first time in three weeks. The Stoxx Europe 600 index fell 0.4% and the MSCI Asia Pacific Index lost 0.5% as U.S. index futures slipped 0.2%. U.S. oil held below $60 before Friday’s OPEC meeting.

This year’s gains in global bonds evaporated as the ECB chief inflamed a selloff in German bunds, saying price growth in the region would pick up further. Greece’s premier claimed to be near agreement with creditors, adding there was no need to worry about an IMF payment due Friday. The U.S. reports jobless claims Thursday, before payrolls data at the end of the week. “There’s a huge selloff all over the world,” said Kim Youngsung at South Korea’s Government Employees Pension Service in Seoul. “The European economy is back on track. The U.S. economy is stable. Suddenly we’re worried about inflation.”

The Bank of America Merrill Lynch Global Broad Market Index of notes with a total face value of $41 trillion is down 0.4% for the year, after being up as much as 2.3% in mid-April. Ten-year German bund yields have soared by 41 basis points this week to the highest level since October. Rates on Australian government debt due in a decade jumped 15 basis points to 3%. Yields on similar-maturity New Zealand and Singaporean notes climbed at least four basis points. Ten-year South Korean sovereign yields rose 3 basis points to 2.48%. Benchmark Treasury notes held losses, with 10-year rates little changed at 2.36%.

Read more …

Talking their books.

• Wall Street Sounds Bond Warning as Holdings Shift Sparks Concern (Bloomberg)

More Wall Street executives are sounding alarms about the bond market. The latest to warn were Gary Cohn, president of Goldman Sachs and Anshu Jain, co-CEO of Deutsche Bank. The concern is bond investors looking to buy, or especially to sell, will face wide prices swings and higher costs to get a transaction done. “The problem is on the days when you need liquidity, it probably won’t be there,” said Cohn at a Deutsche Bank investor conference on Tuesday. Large Wall Street banks, or dealers, are carrying a smaller share of bonds on their books, as regulations restrict the capital they can hold on their balance sheets. Money managers, meanwhile, are holding a lot more of them.

Dealer inventories dropped by 27% between 2007 and early 2015 while assets held by bond mutual funds and exchange-traded funds almost doubled. Federal Reserve officials have also taken notice. They discussed changes in the structure of bond markets at recent meetings, and said those changes may be a risk to financial stability. Deutsche Bank’s Jain said at the Tuesday conference that he didn’t have a “dire warning” about the growing gap between the dealers’ holdings and bond funds’ assets. “But I would certainly say as one of the larger market makers in the system, we very much have an eye on this growing imbalance,” Jain said.

Read more …

“Europe must also consider what it says to the world if, at a dangerous time, it proves unable to fix its own problems.”

• Syriza Could Split, And What Could Europe Have To Deal With Next? (Guardian)

Another crisis of solvency, and Greece is – once again – described as confronting a fork in the road. Athens must finally choose, runs the argument of its creditors, whether it is ready to face up to its responsibilities, or whether instead it prefers to wish away the stack of red final-reminder bills piling up from the IMF, demanding €1.5bn this month. If Greece plumps for denial, however, it should not assume that it can rely on the flow of finance from the north, which is all that is keeping Greek cash dispensers going. Instead, Greeks will have to prepare to slip out of a euro they overwhelmingly wish to keep. There is something in the creditors’ account of events, and yet much is omitted. It neglects to mention how austerity has steadily smothered day-to-day life.

Greece has not merely suffered a recession but a full-blown Grapes of Wrath-style depression, with social and political convulsions to match. The unemployment rate has been 25%-plus for years, with a similar proportion knocked off national income. The “medicine” swallowed so far has proved to be poison. The “Greece must grow up” story also glosses over something else: the frightful choice confronting the rest of Europe. For Greece there is a real dilemma, albeit between two unappealing options. A new drachma would be a leap in the dark, with the disruption of contracts certain and a wipeout of savings likely, even if devaluation could also offer a possible path back to recovery by pricing Greece back into tourism and other markets.

Who is to say whether this mix of the ugly, the bad and the good is worse than the dismal certainties of more stagnation? For the wider eurozone, by contrast, the costs of Greek exit far exceed the costs of preventing it. Yes, bold debt forgiveness may provoke pesky requests for similar help from others in future, but the alternative would mean having to defend for the rest of time a supposedly permanent currency which had proved liable to crumble. Europe must also consider what it says to the world if, at a dangerous time, it proves unable to fix its own problems. The EU confronts Russian chauvinism to its east, terror in the Middle East, and a humanitarian crisis on its Mediterranean shore. Greece stands at the junction. A euro exit would throw the ideal of “ever closer union” – which is soon to be further tested by the UK referendum – into an unprecedented reverse.

This week it was reported that the creditors would offer Greece access to €7.2bn in aid in return for extreme prudence in the longer term, on a take-it-or-leave-it basis. Before risking a “leave it”, they need to ask themselves who it is they want to deal with. An iron law of modern European history runs thus: extreme economics leads to extremist politics. A line can be drawn from the Versailles treaty to the breakdown of the Weimar Republic. Eighty years on, a similar phenomenon is at work. In the course of its depression, Greece has lurched from a social-democrat government to a centre-right one to Syriza – a coalition of leftist parties ranging from Keynesian to Marxist. As the troika crashed Greece again and again, Syriza shot from nowhere to lead a government. Brussels’ strategy, then, has been politically counterproductive in the extreme.

Read more …

Kudos to Tsipras.

• Greek Groundhog Day Drags On As Tsipras Rejects Creditors’ Proposals (Bloomberg)

Another round of top-level talks failed to resolve the standoff between Greece and its international creditors as Prime Minister Alexis Tsipras rejected proposals that would unlock bailout funds necessary to avert a default. After a meeting with European Commission President Jean-Claude Juncker and Dutch Finance Minister Jeroen Dijsselbloem, who also heads the Eurogroup, Tsipras said the basis for any accord must be a Greek proposal meant to avoid spending cuts and tax increases, rather than a plan drafted in recent days by creditors. “The realistic proposals on the table are the proposals of the Greek government,” Tsipras told reporters early Thursday in the Belgian capital. We can’t “make the same mistakes, the mistakes of the past,” he said.

The commission said in a statement that “intense work” will continue and “progress was made in understanding each other’s positions on the basis of various proposals.” Months of antagonism and missed deadlines have given way to a greater urgency to decide the fate of Greece. Without access to capital markets, the country has to meet four payments totaling more than €1.5 billion to the IMF in June, while its euro-area-backed bailout also expires this month. Tsipras signaled that Greece will meet its first June IMF payment, which is due Friday. “Don’t worry,” he said. Tsipras said demands by the euro area and the IMF for cuts in the income of poor pensioners and increases in value-added tax on power are unacceptable, highlighting what have been “red lines” in Greece’s stance since his anti-austerity Syriza party swept to power in snap elections in January.

“Ideas like cutting benefits for low-income pensioners, or raising the VAT rate for electricity by 10 percentage points, can’t be a basis for discussion,” he said. The premier sought to paint the commission, the EU’s executive arm, as more favorable to his proposals than are other creditor representatives deemed by Greece to be taking a harder line in the aid deliberations. “There was a constructive will from the EC to reach a common understanding,” he said. The Tsipras government has looked to the commission for support to dilute the austerity-first formula that’s underpinned two Greek rescues totaling €240 billion since 2010. This has led to clashes with creditors who say such bailout conditions have worked for other countries such as Ireland now out of aid programs and Greece should get no special treatment.

Read more …

Really, Ambrose? “..under existential threat from a revanchiste Russia”?

• Europe Has No Choice – It Has To Save Greece (AEP)

Greece has been through the trauma of default and currency collapse before. It went horribly wrong. The sequence of events in the inter-war years have a haunting relevance today. In 1932, Greece turned to the League of Nations and British bankers in a last-ditch effort to defend the drachma under the Gold Standard as reserves drained away. The creditors dithered for three months but ultimately said “no”. Greece devalued and imposed a 70pc haircut on loans. Debt service costs fell by two-thirds at a stroke. It seemed like a liberation at first. The economy was growing briskly again – at more than 5pc – within a year. Then the sugar-rush faded. The credit system remained broken. Greek industry was too backward to exploit a cheaper exchange rate, unlike Japanese industry under Takahashi Korekiyo at the same time. .

The government never regained its credibility. There were four attempted coups d’etat, ending in the military dictatorship of Ioannis Metaxas. Political parties were abolished. Trade union leaders were killed or imprisoned. Greece fell to Balkan fascism. The cautionary episode is dissected in a seminal paper by the University of Athens. “The 1930s should perhaps be given more attention by those currently advocating the ‘Grexit scenario’,” it said. Nobody should underestimate the political hurricane that will follow if Europe proves incapable of holding monetary union together, and Greece spins out of control. The post-war order is already under existential threat from a revanchiste Russia. State authority has collapsed along an arc of slaughter through the Middle East and North Africa, while an authoritarian neo-Ottoman Turkey is slipping from of the Western camp.

To lose Greece in these circumstances – and to lose it badly – would be an earthquake. Yet that is exactly what Greek prime minister Alexis Tsipras evoked in a blistering outburst in Le Monde, more or less threatening an economic and strategic rejection of the West if the creditor powers continue to make “absurd demands”. Yet as a matter of strict economics, nobody knows if Greece would thrive or fail outside the euro. None of the previous break-up scenarios – ruble, Yugoslav dinar or Austro-Hungarian crown – tells us much. The chorus of warnings from EMU leaders that Grexit would be ruinous for the Greeks is a negotiating ploy, or mere cant. Each of the sweeping claims made by EMU propagandists over the last twenty years has turned out to be untrue.

The euro did not enhance growth, or bring about convergence, or displace the dollar as the world’s reserve currency, or bind EMU states together in spirit, and refuseniks such Britain, Sweden, and Denmark did not pay a price for staying out. To the extent that they believe their mantra on Greece, they risk misjudging the political mood in Athens. It leads them to suppose that Syriza must be bluffing. Costas Lapavitsas, a Syriza MP and an economics professor at London University, thinks the new drachma would plunge by 50pc against the euro before rebounding and stabilising at 20pc below current levels. The trauma would be over within six months. “Greece would be growing at a 5pc rate in a year and it would continue for five years,” he said.

Read more …

“..the Syriza government did not come to power supporting 70% of the Memorandum..”

• Tsipras Turns to Party Hand Tsakalotos to End Talks Impasse (Bloomberg)

Greek PM Alexis Tsipras heads into talks to break a stalemate over a financial lifeline in Brussels on Wednesday surrounded by trusted party hands, chief among them Euclid Tsakalotos. The Oxford-educated economist and Greek deputy foreign minister was asked in April to step into the shoes of Finance Minister Yanis Varoufakis in day-to-day debt negotiations as Tsipras moved to defuse the acrimony building up with creditors. As sparring and missed deadlines to decide the fate of Greece enter a fifth month, Tsipras needs someone by his side who’s as acceptable to creditors as he is to party hardliners because the next stage of the battle to avoid financial collapse will likely be fought in Athens. “Tsakalotos is now, at least on paper, the guy in charge of the negotiations with the creditors,” said Wolfango Piccoli at Teneo Intelligence in London.

“It’s also useful for the prime minister to have him in Brussels in relation to the next big challenge: selling the deal to the party.” Tsipras said he will press creditors to be realistic about what his country can accept. After European leaders and the head of the IMF huddled late into the night in Berlin on Monday, creditors agreed on a new document designed to avert a default. Greece has four payments due to the IMF in June while its existing bailout expires this month. Tsipras, who put forward his own plan, is slated to meet EC President Jean-Claude Juncker on Wednesday evening. “I will explain to Juncker that today, more than ever, it’s necessary that the institutions and the political leadership of Europe move forward to realism,” Tsipras said before traveling to Brussels.

The latest twists put the onus on Tsipras’s anti-austerity government to shelve some election promises or jeopardize the country’s euro status. Sticking points in the talks have included budget measures, pension reforms and changes to Greece’s labor laws, with Tsipras’s Syriza party talking about red lines. Some members of the party have been critical of the backtracking on promises that brought Tsipras to power. John Milios, a member of the Syriza central committee, wrote and tweeted a few days ago that “the Syriza government did not come to power supporting 70% of the Memorandum. If Syriza had pledged so, it would probably not be included in the parliamentary map today, playing the key role.”

Read more …

Some things are going well.

• Greek Exports Ex-Fuel Products Soar 14% (Kathimerini)

The increase in olive oil exports and the decline in exports of fuel products were the main factors that affected the course of external trade in the first quarter of the year, according to official data. There was also a significant shift in the main exporting products as well as the markets they head to. The total value of exports in the January-March period this year amounted to €6.27 billion, down 1.8% from the same period in 2014. However, when fuel products are exempted, there was a €549.1million increase, amounting to 14% year-on-year.

The European Commission recently revised its forecast regarding the course of Greek exports, reducing their expected growth to 4.1% on annual basis from a previous estimate of 5.6%. Most Greek exports (52.4%) head to fellow European Union member-states and their value climbed by 14.5% in Q1. However, exports to North America soared 45.8%, on the more favorable exchange rate of the euro with the dollar, making the US the sixth most important market for Greece’s exports, from tenth a year earlier.

Read more …

The pipeline itself needs EC approval, with the US dead set against it.

• Athens Concerned Over Exclusion From TurkStream Pipeline (Kathimerini)

As a spokesman for the TurkStream pipeline said Wednesday that construction of the Gazprom-backed project will start by the end of the month, diplomatic sources in Athens suggested the Greek government was concerned that Moscow was mulling alternative routes which could potentially exclude Greece from the plans. During a meeting with Russian Prime Minister Dmitry Medvedev in Moscow on Tuesday, Slovakia’s Prime Minister Robert Fico put forward a plan that would see his country, plus another three European states, connected to the Russia-Turkey pipeline that will carry gas all the way to the Greek-Turkish border.

According to Fico’s plan, the pipeline would not cross Greek territory but transfer gas to Central Europe through Bulgaria, Romania, Hungary and Slovakia. Fico’s proposal also appeared to be welcomed by Hungary despite the fact that Budapest recently signed a declaration of intent stating that the pipeline will pass through Greece. The declaration was also signed by Hungary, Serbia, Turkey and the Former Yugoslav Republic of Macedonia (FYROM). Diplomatic sources on Wednesday said that Moscow will decide on the exact route only after it has the go-ahead from the European Commission.

The same sources described comments by Greek officials over an imminent deal with Moscow as overoptimistic. On Wednesday, an unnamed official attending an international gas conference in Paris told AFP that a deal signed in May with the Saipem construction company would allow work on the first of four sections to begin by the end of the month. At the same event, it was made known that Turkish Stream had been renamed TurkStream. The project was announced by Russian President Vladimir Putin late last year in a bid to replace the ditched South Stream pipeline. Analysts have called attention to a Washington warning against the construction of a pipeline bypassing Ukraine, a strategic US ally.

Read more …

The advantages of having one’s own currency.

• Here’s What Defaults Did to Other Countries as Greece Teeters (Bloomberg)

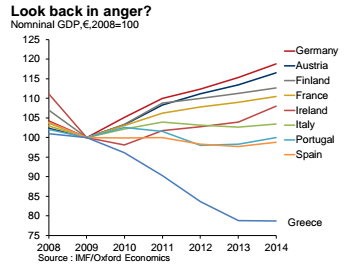

By Friday, we may know whether Greece has reached a debt deal with its creditors. A failure could trigger a default and raise the prospect that it becomes the first country to leave the euro currency union. The history of previous economic cataclysms suggests that changes in currency values can work as escape valves that quickly, though not painlessly, relieve pressure on an economy. Massive depreciations allow countries to become more competitive internationally, enabling them to draw back from the brink more quickly. The charts below compare changes in exchange rates before and after four other disruptions that riled markets: Russia’s default in 1998, Argentina’s in 2001, the U.S. during and after the collapse of Lehman Brothers in 2008, and Greece’s debt restructuring in 2012. For Russia and Argentina, defaults punished their currencies.

For the U.S. dollar, the result was more mixed. Greece is part of the euro zone, and the 2012 impact on that currency was also mixed. The next charts show what happened to gross domestic product. Turns out the Argentine and Russian defaults were boons in those countries, with growth rebounding sharply. Upturns came much more slowly in the U.S. – which while home to the biggest-ever corporate bankruptcy didn’t default on its sovereign debt – and in Greece.

Unemployment rates in Argentina and Russia also showed clear inflection points for the better, while workers in the U.S. and Greece had to suffer through delayed improvement.What separates Greece’s from Argentina and Russia is the Greeks’ membership in the currency union (whereas Argentina and Russia have their own exchange rates). That means the country can’t enjoy the benefits of a massively cheaper currency before exiting the euro first, something that officials across the region have ruled out.

“The problem with Greece is that defaulting on the debt without the followup of a devaluation may buy time but won’t resolve its growth problems,” said George Magnus, senior economic adviser to UBS in London. “If Greece chose to default and stayed inside the euro zone, the option of a devaluation would not exist so it’s not clear why Greece should experience a growth rebound.”This dance that’s happening at the moment could go on for quite some time,” he said.

Read more …

“Arbeit macht frei” seems to have taken on a whole new meaning these days for whole bunch of us out here.”

• A Member Of The Middle Class Responds To Jon Hilsenrath (Zero Hedge)

Dear Mr Hilsenrath and your Central Bank Team, This is Joe from the disappearing Middle Class in America. You asked me the other day to drop you a note if I felt that something was wrong. What I’m having trouble with is “why” you’re asking me if anything is wrong!? So let me explain. Regarding the weather, as you stated, the sun shined in April. It was also overcast some days some places, rained a few spots here and there, was nice quite a few days and even got dark on time, most evenings. And the Commerce Department is spot on that my spending didn’t increase any adjusted for the inflation that you all keep telling me isn’t there. Have you tried to buy some hamburger recently or do you just eat out on a corporate credit card? The price of a pack of spaghetti has doubled over the past 3 years.

Me and Mrs. J along with the kids kinda like spaghetti now and then and the Mrs. even made a great Bolognese sauce, but the hamburger got too expensive as has the spaghetti, so we had to cut back. So you’re right, we did sit at home and watch Dancing with the Stars a lot. It’s what we can afford. So, I really don’t get what you guys mean by those “winter doldrums” because things have gotten worse independent of the weather. The weather’s had nothing at all to do with it. And talking about worse, you’re right. I did get fired in late 2008 from a high paying salaried job with benefits when the economy dumped due to the Lehman Brothers shock.

Since then I’ve been holding down a part time greeters job at Home Depot with no benefits. I even took on a second part time job with no benefits at another place because I was getting bored watching television all day. Plus, we could use the extra money as our savings has been depleted. And we’re very worried about our health and the cost of healthcare is skyrocketing. But I guess you probably have a health care plan paid for by the Wall Street Journal. Why, feeling particularly liberated, Mrs. Joe’s even picked up a couple of part time jobs, as well. “Arbeit macht frei” seems to have taken on a whole new meaning these days for whole bunch of us out here.

Read more …

Surefire road to failure.

• German And French Ministers Call For Radical Integration Of Eurozone (Guardian)

German and French politicians are calling for a quantum leap in how the EU’s single currency is run, proposing an embryo eurozone treasury equipped with a eurozone finance chief, single budget, tax-raising powers, pooled debt liabilities, a common monetary fund, and separate organisation and representation within the European parliament. They also propose that all teenagers in the EU be given the chance to spend a subsidised six months in another European country. In an article published in European newspapers, Sigmar Gabriel, Germany’s social democratic leader and vice-chancellor in Angela Merkel’s coalition government, and Emmanuel Macron, France’s young reformist economics minister, advocate a radical shift in integration of the eurozone, following five years of single currency crisis that have come close to tearing the EU apart.

They call for the setting up of “an embryo euro area budget”, “a fiscal capacity over and above national budgets”, and harmonised corporate taxes across the bloc. The eurozone would be able to borrow on the markets against its budget, which would be financed from a kind of Tobin tax on financial transactions and also from part of the revenue from the new business tax regime. The eurozone’s current bailout fund, the European Stability Mechanism, which is made up of national contributions under a deal between governments, would be made a common eurozone instrument and converted into a European Monetary Fund. The entire new regime would come under the authority of a new post of euro commissioner who would be answerable to eurozone MEPs who, in turn, would need to have a separate sub-chamber in the European parliament.

In reference to the Greek crisis currently moving towards some form of denouement, the two leading figures say the new regime they are proposing should also establish “a legal framework for orderly and legitimate sovereign debt restructurings, should they become necessary as a last resort. This would prevent both inappropriate use of crisis lending and self-defeating bouts of austerity when countries face unsustainable debts.” Germany and France are the two biggest countries in the eurozone. Gabriel and Macron are both seen as youngish leaders of reformist social democracy in an EU, however, dominated by the centre-right, suggesting that their ideas might struggle to find traction.

Read more …

The crumbling union.

• European Dream Just a Fairy Tale to New Breed of Eastern Leaders (Bloomberg)

Natalia Krzywicka wasn’t alive when Poland shrugged off the shackles of communism in 1989. When it joined the European Union 15 years later, she was only eight. Now, the 19-year-old student is ready for her country to stop acting like a newcomer to the EU and start doing something for its voters, including her. She helped unseat the government-backed incumbent in a May 24 presidential runoff, eastern Europe’s fifth such upset since 2013. “I know that economic indicators quoted in the mainstream media show Poland is in good shape, but that’s just propaganda,” Krzywicka said in front of Warsaw’s Wilanow Palace, a sprawling 17th-century estate. “Poland’s policy makers need to refocus on defending the country’s interests, like everyone else.”

Krzywicka is among voters in the EU’s east who are shaking up politics after more than two decades of tolerating the fiscal and economic measures needed to qualify for membership in the bloc. After years of their governments focusing on selling state assets, luring foreign investment, overhauling communist-era bureaucracy and trying to meet EU budget and competition rules, they’re now demanding action on bread-and-butter issues including pensions and health care. In Poland, opposition-backed Andrzej Duda defeated President Bronislaw Komorowski by pledging to overturn a government-imposed increase in the pension age and to pull the country of 38 million away from the “European mainstream.” His victory followed presidential upsets against ruling party candidates in Romania, Slovakia, Croatia and the Czech Republic over the last two years.

Betting that incomes of the 100 million people in the eastern economies would approach the level of their western neighbors, investors plowed billions into the region even before the EU’s first wave of enlargement in 2004. Since then, they’ve been rewarded by outsized returns. Hungary’s local-currency government bonds have returned 169%, the most among 26 indexes tracked by the European Federation of Financial Analysts Societies. Polish notes have handed investors 107% and Czech securities 77%, compared with an EU average of 71%. Yet there are growing signs that the change from centrally planned to market-driven economies is mostly over.

While the region’s governments sold off most of their state-owned manufacturers, banks and utilities last decade, now governments in Bulgaria, Slovakia and Hungary are criticizing foreign-owned power companies for high prices. The latter two have imposed special taxes, mostly on lenders, to shore up their budgets, a plan Duda wants to emulate in Poland. Hungarian Prime Minister Viktor Orban has gone the farthest in the region in expanding state control, buying the local businesses of foreign companies including EON and GE Capital. “I expect the efforts to push through structural reform will decrease,” said Peter Schottmueller at Deka Investment in Frankfurt. “This is a major problem every government in Europe has to tackle: wage growth, youth unemployment. We haven’t found a solution.”

Read more …

Count me not surprised.

• EU Home To Widespread Labor Exploitation (RT)

The European Union is home to widespread employment abuses, according to a new study. Both EU and non-EU citizens have fallen victim to labor exploitation, despite laws which allegedly protect workers. The study, conducted by the European Union Agency for Fundamental Rights (FRA), is the first of its kind to thoroughly explore all criminal forms of labor exploitation in the EU. The agency compiled around 600 interviews with representatives of trade unions, police forces and supervisory authorities, finding that employment abuses are prevalent across the EU. “Labor exploitation is a reality in the EU,” FRA spokesperson Bianca Tapia said, as quoted by Deutsche Welle. She added that it is becoming extremely commonplace in some sectors of the economy.

According to the findings, criminal labor exploitation is prominent in a number of industries – particularly construction, agriculture, hotel and catering, domestic work and manufacturing. The FRA said that one in five inspectors dealing with the issue came across severe cases of exploitation at least twice a week. “What these workers in different geographical locations and sectors of the economy often have in common is a combination of factors: being paid 1 euro or much less per hour, working 12 hours or more a day for six or seven days a week, being housed in harsh conditions, and not being allowed to go on holiday or take sick leave,” Tapia said in the report.

While the study stressed that both EU and non-EU citizens face such conditions, Tapia did note that “foreign workforces are at serious risk of being exploited in the EU.” Many migrant workers have their passports taken off of them and are cut off from the outside world by employers, the agency said. The Vienna-based rights group compiled over 200 case studies. Among those were Lithuanians working on British farms and living in sheds with little access to hygiene facilities. A case of Bulgarians harvesting fruit and vegetables in France for 15 hours a day – but being paid for just five of the 22 weeks they worked – was also cited.

Read more …

What do you mean, a bubble?

• Who Cares About China’s Economy When Stocks Are Rising This Much? (Bloomberg)

When Sean Taylor looks at China’s soaring stock prices, he sees a market more disconnected from economic fundamentals than at any other time in a two-decade career. His advice to investors? Keep buying. The London-based head of emerging markets at Deutsche Asset & Wealth Management, whose developing-nation equity fund has outperformed 94% of peers tracked by Bloomberg this year, says what matters most in China right now is that policy makers have the motivation and firepower to keep the world-beating rally going. Rising stock prices not only help Chinese companies reduce debt levels by selling new shares, they also make it easier for the government to boost budget revenue and push forward on privatization plans through stake sales.

One way policy makers can support further gains is through further monetary stimulus: banks’ reserve requirement ratios are almost 6 percentage points higher than the 15-year average, even after two cuts this year. “The government wants a strong stock market, to privatize more companies and do more IPOs,” Taylor, whose firm oversees about $1.3 trillion, said in an interview in Hong Kong. He has an overweight position in Chinese shares. The Shanghai Composite has gained 141% in the past 12 months, the most among major global benchmark indexes. The gauge closed little changed today. The following charts underscore the disconnect between Chinese stocks and the economy.

• Shanghai Composite performance: The index rose last week to its highest level in seven years, while Bloomberg’s monthly gross domestic product tracker for China is near the lowest since 2009.

• Financial stocks: The CSI 300 Index’s gauge of banks, property developers and brokers climbed to its highest level since January 2008 last week. Data on May 13 showed the M2 measure of broad money supply grew 10.1% in April from a year earlier, the smallest expansion on record.

• Retail stocks: The consumer discretionary index has rallied 75% this year to a record. Retail sales grew 10% in April, the slowest pace since 2006.

Read more …

“Markets might recover, but often people do not.”

• Oliver Stone: Wall Street Culture “Horribly Worse” Than Gordon Gekko (SMH)

The culture on Wall Street is “horribly worse” than it was in the 1980s, and America’s regulatory culture is lost, according to Hollywood director Oliver Stone. Mr Stone, who was in Melbourne speaking at the Game Changers event held by superannuation firm Sunsuper, said he made the sequel Wall Street: Money Never Sleeps in 2010 to address the problem with the culture he exposed in his iconic 1987 film Wall Street. “Gordon Gekko was an immoral character that became worshipped for the wrong reasons… the banks became a version of him, speculating for themselves. To hell with the investor,” he told Fairfax Media.

Gekko’s legacy may be alive and kicking in the finance mecca. A new study of US finance executives found that 47% said they it was likely their competitors had engaged in illegal or unethical conduct to gain a market advantage. A separate study found one third of Wall Street financiers who earned more than $500,000 had witnessed wrongdoing. Mr Stone’s comments came after two of Australia’s top regulators signalled a clampdown on a “rotten culture” that exists within the Australian finance industry. Australian Securities Investment Commission chairman Greg Medcraft said last week the way banks and brokers structured incentives was a driver of white collar crime. ASIC has said it is investigating three investment banks in Australia.

Mr Stone said while money had “polluted politics” in the US, he believed Australia’s regulation was stronger, which helped it avoid the full impact of the global financial crisis. But he was suprised to be told of the financial planning scandal enveloping the big four banks and the subsequent Financial System Inquiry. “You can always make money with banks, the problem is you have to self-discipline so you don’t screw the investors,” he said. Mr Stone said it was the nature of capitalism to bubble and burst. “You can never find a moderate balance. You need supervisroy intelligence to balance the excesses of market, and that is the lesson that [US President Franklin D.] Roosevelt taught us in the 1930s, but that seems to have been forgotten,” he said.

Read more …

Posterchild for regulatory failure.

• Elizabeth Warren Blasts Mary Jo White’s SEC Leadership (MarketWatch)

Sen. Elizabeth Warren on Tuesday blasted the leadership of Securities and Exchange Commission Chairwoman Mary Jo White, calling it “extremely disappointing.” It’s the most aggressive critique yet from the Massachusetts Democrat, who has often criticized regulators over their perceived lax stance against Wall Street firms. In a 13-page letter sent to White on Tuesday, Warren cites four main complaints with White’s two-year tenure:

•The SEC’s failure to finalize Dodd-Frank rules regarding disclosure of CEO pay to median workers.

• White’s failure to curb the use of waivers for companies that violate securities laws. Several firms received a waiver after pleading guilty to Justice Department charges of manipulating the foreign exchange market.

• SEC settlements that don’t require an admission of guilt.

• Numerous SEC enforcement cases that require recusals by White because of conflicts from her prior law firm employment and her husband’s current law practice. Warren even suggests companies may deliberately hire her husband, John White, to lead to a recusal and a 2-to-2 deadlock of remaining commissioners.

White was aggressive in her response, saying the senator mischaracterized her comments. “I am very proud of the agency’s achievements under my leadership, including our record year in enforcement and the Commission’s efforts in advancing more than 30 congressionally mandated rulemakings and other transformative policy initiatives to protect investors and strengthen our markets,” White said in a statement. “Senator Warren’s mischaracterization of my statements and the agency’s accomplishments is unfortunate, but it will not detract from the work we have done, and will continue to do, on behalf of investors.”

Read more …

Looks like the US may be losing.

• Kim Dotcom Thwarts Huge US Government Asset Grab (TorrentFreak)

Kim Dotcom has booked a significant victory in his battle against U.S. efforts to seize assets worth millions of dollars. In a decision handed down this morning, Justice Ellis granted Dotcom interim relief from having a $67m forfeiture ordered recognized in New Zealand. Dotcom informs TF that the victory gives his legal team new momentum. In the long-running case of the U.S. Government versus Kim Dotcom, almost every court decision achieved by one side is contested by the other. A big victory for the U.S. back in March 2015 is no exception. After claiming that assets seized during the 2012 raid on Megaupload were obtained through copyright and money laundering crimes, last July the U.S. government asked the court to forfeit bank accounts, cars and other seized possessions connected to the site’s operators.

Dotcom and his co-defendants protested, but the Government deemed them fugitives and therefore disentitled to seek relief from the court. As a result District Court Judge Liam O’Grady ordered a default judgment in favor of the U.S. Government against assets worth an estimated $67m. Following a subsequent request from the U.S., New Zealand’s Commissioner of Police moved to have the U.S. forfeiture orders registered locally, meaning that the seized property would become the property of the Crown. Authorization from the Deputy Solicitor-General was granted April 9, 2015 and an application for registration was made shortly after.

In response, Kim Dotcom and co-defendant Bram Van der Kolk requested a judicial review of the decision and sought interim orders that would prevent the Commissioner from progressing the registration application, pending a review. The Commissioner responded with an application to stop the judicial review. In a lengthy decision handed down this morning, Justice Ellis denied the application of the Commissioner while handing a significant interim victory to Kim Dotcom. Noting that the “fugitive disentitlement” doctrine forms no part of New Zealand common law, Justice Ellis highlighted the predicament faced by those seeking to defend themselves while under its constraints.

Read more …

“..an “extreme deregulatory agenda” on the part of both the United States and Australia’s negotiators with “serious implications for all service sectors, perhaps human services especially”.

• WikiLeaks Reveals New Australia Trade Secrets (SMH)

Highly sensitive details of the negotiations over the little-known Trades in Services Agreement (TiSA) published by WikiLeaks reveals Australia is pushing for extensive international financial deregulation while other proposals could see Australians’ personal and financial data freely transferred overseas. The secret trade documents also show Australia could allow an influx of foreign professional workers and see a sharp wind back in the ability of government to regulate qualifications, licensing and technical standards including in relation to health, environment and transport services.

In its largest disclosure yet relating to the TiSA negotiations, WikiLeaks has published seventeen documents including draft treaty chapters, memoranda and other texts setting out the overall state of negotiations and individual country positions in a secret bargaining on banking and finance, telecommunications and e-commerce, health, as well as maritime and air transport. The leaked documents were to be kept secret until at least five years after the completion of the TiSA negotiations and entry into force of the trade agreement. Dr Patricia Ranald, research associate at the University of Sydney and convener of the Australian Fair Trade and Investment Network, said WikiLeaks’ publication revealed an “extreme deregulatory agenda” on the part of both the United States and Australia’s negotiators with “serious implications for all service sectors, perhaps human services especially”.

The leaked draft TiSA financial services chapter shows a continuing strong push by the United States, Australia and other countries for deregulation of international financial services, an approach strongly supported by Australian banks keen to increase their business in Asian markets. However Financial Sector Union secretary Fiona Jordan said there was a need to strengthen not weaken financial and banking regulation. “The issue has to be about Australia maintaining the tight regulations it has – and perhaps even adding to these,” Ms Jordan said.

Read more …

Global markets for basic necessities is always a bad idea. They can only lead to hunger.

• The Big Global Food Game (Beppe Grillo’s blog)

The world’s population continues to grow and as the eating habits of people in developing countries like China and Brazil are changing rapidly, they are beginning to include more meat and cereals in their diets. Land for cultivating crops and raising livestock is a finite resource and the race to get hold of pieces of land, water and animals is already in full swing, with China grabbing the lion’s share. The big food game is already going full speed ahead and anyone who is left out at this stage is lost. In his book entitled Pappa Mundi, Francesco Galietti talks about how food is becoming one of the main issues in International relations. We interviewed him to find out more.

“A big hello to all the friends of Grillo’s Blog. Since we’re dealing with a market here, as always it is dictated by two factors, namely supply and demand, both of which are constantly changing. As far as demand is concerned, obviously the big daddy of all topics of debate on this issue is China, the Chinese Dragon. It’s not that the country’s population is increasing disproportionately, but what is changing, and very fast too, is the ratio of its very fast growing middle class to its total population. This means that there is now a whole range of new prerogatives, including tastes, fashions, desires and wants, all of which have very serious repercussions on foods. For these people, meat used to be something that only the privileged could enjoy in the exclusive restaurants but now that they can afford it too, they also want it.

For example, SmithField is the largest global piggery. It is an American company that breeds and raises pigs and just recently it was bought out by the Chinese. This acquisition came to the attention of the American Military, who were absolutely incredulous and couldn’t understand why on earth Chinese investors would come to America to buy pork. They were equally incredulous when they discovered that China has a specific doctrine in this regard, so much so that they have come up with the so-called Strategic Pork Reserve, in other words a way of making sure that China always maintains a certain stock of pork. Then there is also another component, namely the food anxiety that Middle-East investors have. Notwithstanding its great variety, the Middle-East is and remains little more than a huge sandbox.

This means that the petrol sheiks are looking for that which they don’t have, and they go looking for it all over the world. They have created such a huge expanse of rice paddies that Saudi-Arabia has now become the world’s sixth largest rice producer! There is a general fear of finding ourselves without any food for our people, above all the working people who are most often the disadvantaged ones that come from Pakistan and ’Asia, so I the case of the Middle-East, the search is on for what they don’t have. The third important component in the big food game is the use of food as a weapon of war. Putin has decided to counter western sanctions with counter-sanctions on food, which is a real tragedy for us Italians because it means bye-bye to our significant exports of Grana Padano to Russia, as well as other goodies for the oligarchy’s palates.

Read more …

It’s a shame that this focuses on emissions. There are much better reasons to eat local food.

• Replanting America: 90% of What We Eat Could Come From Local Farms (Nosowitz)

Eating a local diet—restricting your sources of food to those within, say, 100 miles—seems enviable but near impossible to many, thanks to lack of availability, lack of farmland, and sometimes short growing seasons. Now, a study from the University of California, Merced, indicates that it might not be as far-fetched as it sounds. “Although we find that local food potential has declined over time, our results also demonstrate an unexpectedly large current potential for meeting as much as 90% of the national food demand,” write the study’s authors. 90%! What?

Researchers J. Elliott Campbell and Andrew Zumkehr looked at every acre of active farmland in the U.S., regardless of what it’s used for, and imagined that instead of growing soybeans or corn for animal feed or syrup, it was used to grow vegetables. (Currently, only about 2% of American farmland is used to grow fruits or vegetables). And not just any vegetables: They used the USDA’s recommendations to imagine that all of those acres of land were designed to feed people within 100 miles a balanced diet, supplying enough from each food group. Converting the real yields (say, an acre of hay or corn) to imaginary yields (tomatoes, legumes, greens) is tricky, but using existing yield data from farms, along with a helpful model created by a team at Cornell University, gave them a pretty realistic figure.

Still, the study involves quite a few major leaps of faith because it seeks not to demonstrate what is possible for a given American right now but to lay out a basic overview of the ability of local food to feed all Americans. It’s not just projecting yields for vegetables grown on land that is today dominated by corn and soy. The biggest leap of faith is perhaps an unexpected one and is surprisingly underreported: Why do we even want to adjust our food supply to be local in the first place?

Read more …