William Claxton John Coltrane at the Guggenheim Museum, New York 1960

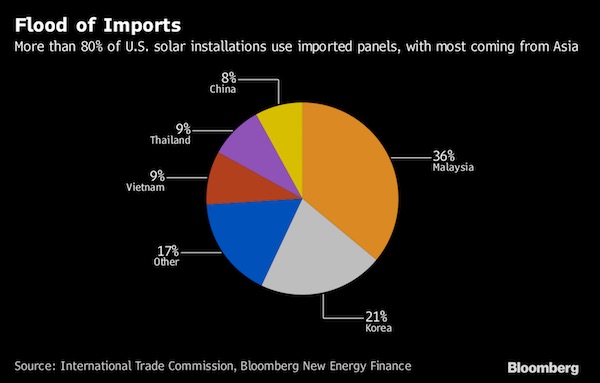

Make your own solar panels. What’s wrong with that?

• Trump Makes First Big Trade Move With Tariffs Aimed At Asia (BBG)

President Donald Trump imposed tariffs on imported solar panels and washing machines, in his first major move to level a global playing field he says is tilted against American companies. The U.S. will impose new duties of as much as 30 percent on foreign-made solar equipment, the U.S. Trade Representative’s office said Monday. The president also approved tariffs starting as high as 50 percent on imported washing machines. Chinese and South Korean officials condemned the move, analysts said it could backfire, while markets largely shrugged it off. The tariffs were announced as Trump prepares to travel to the World Economic Forum in Davos, Switzerland, where the international business and political elite gather to mull the current state of the global order.

While the measures may sharpen the president’s “America First” policy after months of rhetoric and herald a hotter trade conflict with China, in Asia manufacturers and investors said the reality wasn’t as bad as they had feared. Investors “are used to bluff from Trump, which often turns out to be a non-event,” said Qiu Zhicheng at ICBC International Research in Hong Kong. “As long as the situation doesn’t escalate into a full-scale trade war, the market impact will be limited. We believe the two economies will stay rational, as a trade war would hurt both.” LG Electronics, a maker of domestic appliances, and South Korean solar panel makers fell initially in Seoul trading on the news before recovering. Samsung said the tariff on washing machines is a “great loss” for U.S. workers and consumers.

South Korea’s trade minister said Tuesday that his nation will file a petition with the World Trade Organization against the U.S. for imposing anti-dumping duties on Korean washing machine and solar panel makers. The U.S. decision is “excessive,” Kim Hyun-chong said. China exported more than 21 million washing machines worth just under 19 billion yuan ($2.9 billion) globally from January through November 2017, according to customs data. China is also the world’s largest exporter of solar panels.

David knows his shutdowns.

• The Shutdown Scam: The GOP Is Now The Second “Government Party” (Stockman)

Nowadays, government “shutdowns” are obviously not all that, and we do claim some expertise on the topic. Since 1975 there have been 14 shutdowns and we have had the privilege of being on-hand up close and personnel during 11 of these. Five shutdowns occurred while your editor was a member of the US House (1977-1981) and another six during his stint as director of OMB. The idea back then, needless to say, was that shutdowns came about mainly when anti-spenders refused to capitulate to the incessant demands of the swamp creatures for more appropriations, pork and graft.

[..] What is really happening, of course, is that the Trumpite/GOP is proving in spades that America is now saddled with two pro-government parties. This means a good shutdown is going to waste and that there is no stopping the fiscal doomsday machine that is now racing toward a national calamity, unimpeded. After all, the reason Washington is operating on its 3rd CR of the fiscal year and struggled a whole weekend to get a fourth one lasting a mere 16 days, lies in the utter irresponsibility of the Trump GOP approach to fiscal policy.

These clowns want to spend $120 billion on disaster relief without a single dime of off-setting cuts; raise defense by $80 billion when the Pentagon is already a $620 billion swamp of waste; appropriate $33 billion for an utterly idiotic Wall on the Mexican border when the problem could be solved by cancelling the $32 billion per year “War on Drugs” and putting up guest worker sign-up booths along the border; and authorizing tens of billions on top of that to pay for the backroom “deals” that were made in order to get the votes for a massive tax bill that not a single Senators or House member had read before it was ram-rodded into law by desperate GOP leaders on Christmas Eve.

So this shutdown is indeed different. Unlike the case back in the day, there is no fiscal red line whatsoever at issue; only a prospective eruption of more red ink and an interim game of political chicken about 700,000 Dreamers, who at the end of the day will not be deported and who will eventually get a path to citizenship. That’s because they, and millions of more immigrants to come, comprise the only available “growth” margin for the US work force in the decades ahead; and therefore constitute the next generation of Tax Mules which will be absolutely necessary to support today’s 50 million retirees. That is, as their population inexorably swells toward 100 million during the next four decades.

Pressure on the FBI is set to increase tenfold.

On Sunday, the FBI revealed that it had lost five months of text messages between Trump antagonists Peter Strzok and Lisa Page. The agency offered a lame explanation that “software upgrades” and “misconfiguration issues” interfered with the app that is supposed to automatically save and archive communications between officials on FBI phones. This was the couple who chattered about an FBI-generated “insurance policy” for the outcome of the 2016 election with Deputy Director Andrew McCabe. When will these three be invited to testify before a house or senate committee to inform the nation exactly what the “insurance policy” was?

The bad odor at the FBI seeps into several other areas of misbehavior involving Hillary Clinton, her campaign, the Democratic National Committee (DNC), and members of the permanent Washington bureaucracy. Did the Obama White House use the Christopher Steele dossier, paid for by the Clinton Campaign, to obtain FISA warrants against her opponent in the election for the purpose of conducting electronic surveillance on him? Was the FBI abetting a Democratic Party coup to get rid of Trump by any means necessary once he got into office?

Did the FBI conduct a stupendously half-assed investigation into Hillary Clinton’s private email server by dismissing the charges before interviewing any of the principal characters involved, granting blanket immunities to Obama White House officials, and failing to secure computers that contained evidence? Does the FBI actually know what then Attorney General Loretta Lynch discussed with Bill Clinton in the parked airplane on the Phoenix tarmac? Did the FBI fail to investigate enormous contributions (roughly $150 million) to the Clinton Foundation after the Uranium One deal was signed? Did they look into any of the improprieties surrounding the DNC’s effort to nullify Bernie Sander’s primary campaign?

Growth is God.

• IMF Raises Global Growth Forecast, Sees Trump Tax Boost (R.)

The IMF on Monday revised up its forecast for world economic growth in 2018 and 2019, saying sweeping U.S. tax cuts were likely to boost investment in the world’s largest economy and help its main trading partners. However, the IMF, in an update of its World Economic Outlook, also added that U.S. growth would likely start weakening after 2022 as temporary spending incentives brought about by the tax cuts began to expire.\ The tax cuts would likely widen the U.S. current account deficit, strengthen the U.S. dollar and affect international investment flows, IMF chief economist Maurice Obstfeld said. “Political leaders and policymakers must stay mindful that the current economic momentum reflects a confluence of factors that is unlikely to last for long,” Obstfeld told reporters at the World Economic Forum in Davos.

He said economic gains from the tax cuts would be partially paid back later in the form of lower growth as temporary spending incentives, notably for investment, expired and as rising federal debt took a toll. IMF Managing Director Christine Lagarde pointed to a “troubling” increase in debt levels across many countries and warned policymakers against complacency, saying now was the time to address structural deficiencies in their economies. Obstfeld said a sudden rise in interest rates could lead to questions about the debt sustainability of some countries and lead to a disruptive correction in “elevated” equity prices.

IMF wants their cake and eat it. They warn against the failure of their own policy recommendations.

• IMF: Next Recession Will Come Sooner And Will Be Harder To Fight (EuA)

The global economy is growing faster than expected, fuelling CEO optimism as they arrive this week at the World Economic Forum (WEF) in Davos, Switzerland. But the IMFhas warned that the next crisis will hit sooner and harder that we thought. “In seed time learn, in harvest teach, in winter enjoy,” said IMF Managing Director Christine Lagarde, issuing a warning by quoting British poet William Blake to describe the state of mind of businessmen and politicians in the world. The global economy continues to beat previous forecasts. The Fund revised upward by 0.2% the growth expected for this year and next. In Europe, the IMF increased further its outlook by 0.3% in 2018 (2.2%) and in 2019 (2%). But “complacency is one of the risks we should go against”, Lagarde told reporters in Davos hours before the official opening of the WEF.

The economy is growing but not because countries have lifted their growth potential via investment in human capital or technology. Instead, reforms have been elusive and growth has benefited just the few that are on top of the pile. “We are not satisfied,” Lagarde insisted, because “too many people have been left out of the acceleration of growth”. Against the backdrop of fragile growth and outstanding challenges, including a high level of debt, the Fund’s chief economist, Maurice Obstfeld, stressed that “the next recession will come sooner and will be harder to fight”. He warned political leaders that the economic momentum is due to factors that are “unlikely to last for long”, including the monetary stimulus and supportive fiscal stance. For that reason, he urged countries to adopt measures aimed at improving the resilience of their societies in the fast-changing digital revolution and to improve the inclusiveness of their societies.

Another huge surge in debt. Insane. But the only way to keep the zombie from dying.

• Rising Interest Payments Matter (NMT)

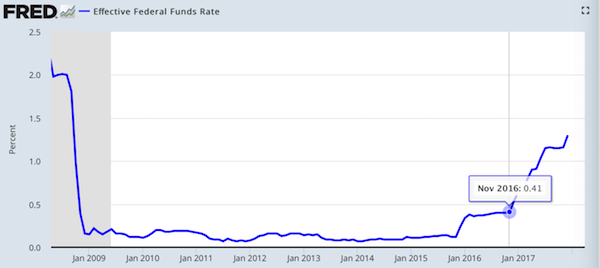

Is anyone paying attention? I don’t know, but the cost of carrying debt has been rising and it’s already showing measurable impacts despite the Fed Funds rate still being very low. My concern of course is that the global debt construct will bring global growth to a screeching halt (see also The Debt Beneath). As the 10 year is already piercing above the 2.6% area now I want to pay attention to the data coming in as the Fed is dot plotting more rate hikes to come. After all the Fed has hiked 5 times off the bottom floor in the past 2 years:

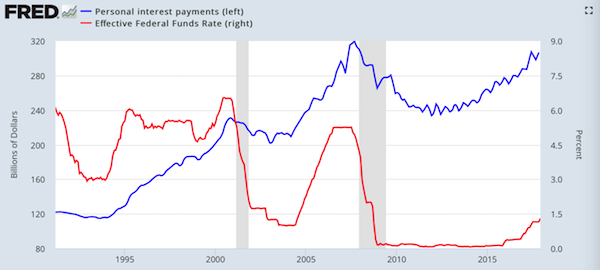

Can we see any measurable impact? You bet we can. Here are personal interest payments for consumers:

Mind you we are still near the lows of the previous cycle and already total interest payments are near record highs. The driver of course is record consumer debt and credit card debt. But despite rates still being historically low this rise in interest rates has an impact on the consumer. Already we see this: “The big four US retail banks sustained a near 20 per cent jump in losses from credit cards in 2017, raising doubts about the ability of consumers to fuel economic expansion. “People are using their cards to get from pay cheque to pay cheque,” said Charles Peabody, managing director at the Washington-based investment group Compass Point. “There’s an underlying deterioration in the ability of the consumer to keep up with their debt service burden.” Recently disclosed results showed Citigroup, JPMorgan Chase, Bank of America and Wells Fargo took a combined $12.5bn hit from soured card loans last year, about $2bn more than a year ago.”

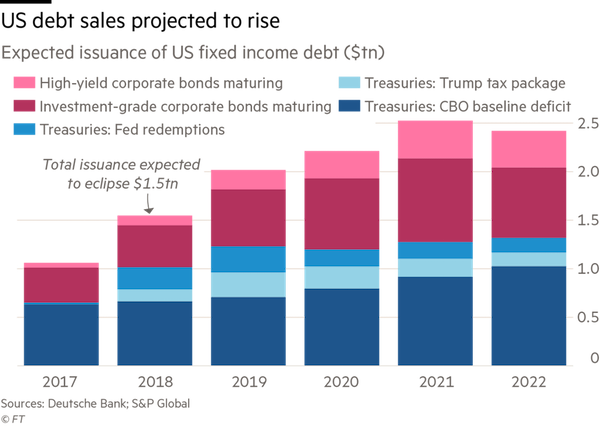

I repeat: “There’s an underlying deterioration in the ability of the consumer to keep up with their debt service burden.” [..] “Economists with Deutsche Bank expect the extra debt the Treasury must issue to fund President Donald Trump’s tax package and the amount of debt the Federal Reserve plans to redeem at maturity this year will bloat issuance to about $1tn in 2018. That’s up more than 50 per cent from a year earlier and, when coupled with a 30 per cent rise in the amount of corporate debt that’s due to mature, leaves questions of who the eventual buyer will be.“ A good question indeed. That’s a lot of debt issuance:

2018 will be the year of the Brexit reversal.

• UK Business Leaders Push For New Campaign To Reverse Brexit (G.)

Business leaders are privately pushing for a new campaign to reverse Brexit as concerns mount about the viability of government plans to prevent a collapse in exports to Europe. On Monday, the CBI launched its most sustained attack yet on the government’s Brexit strategy by calling for full customs union with the EU and single market participation, even if it means abandoning the pursuit of separate trade deals with the rest of the world. Behind the scenes, senior figures on the CBI policy council are urging the lobby group to toughen its message still further and spell out their belief that this logic should ultimately lead to a national rethink of the decision to leave the EU, perhaps through a second referendum or an election.

While this is not the CBI’s official position, the group says it has decided to speak out about the problems of the government’s approach to Brexit after “thousands of conversations” and workshops with its members over the past two to three months. “It’s not for us to say [whether to reverse Brexit], we are simply pointing out that you need single market access and you need a customs union,” said a spokesman. “If someone concludes that we therefore need to retest this, that’s a political decision, we are just being very practical about it.”

Government ministers reacted furiously to previews of the CBI’s evolving position over the weekend, which now directly challenges the British strategy of leaving the customs union so that new trade deals can be pursued outside a common tariff area. The CBI director general, Carolyn Fairbairn, told an audience at Warwick University on Monday: “There may come a day when the opportunity to fully set independent trade policies outweighs the value of a customs union with the EU; a day when investing in fast-growing economies elsewhere eclipses the value of frictionless trade in Europe. But that day hasn’t yet arrived.”

The former government, to be exact.

• Kim Dotcom Sues New Zealand Government For Billions in Damages (BBC)

Kim Dotcom, the founder of file-sharing site Megaupload, is suing the New Zealand government for billions of dollars in damages over his arrest in 2012. The internet entrepreneur is fighting extradition to the US to stand trial for copyright infringement and fraud. Mr Dotcom says an invalid arrest warrant negated all charges against him. He is seeking damages for destruction to his business and loss of reputation. Accountants calculate that the Megaupload group of companies would be worth $10bn (£7.2bn) today, had it not been shut down during the raid. As he was a 68% shareholder in the business, Mr Dotcom has asked for damages going up to $6.8bn. He is also considering taking similar action against the Hong Kong government.

As stated in documents filed with the High Court, Mr Dotcom is also seeking damages for: • all lost business opportunities since 2012 • his legal costs • loss of investments he made to the mansion he was renting • his lost opportunity to purchase the mansion • loss of reputation. “I cannot be expected to accept all the losses to myself and my family as a result of the action of the New Zealand government,” he told the BBC. “This should never have happened and they should have known better. And because they made a malicious mistake, there is now a damages case to be answered.” New Zealand Prime Minister Jacinda Ardern told Radio New Zealand: “This has obviously been an ongoing matter, so no it doesn’t surprise me.”

Mr Dotcom’s key argument over his extradition is the warrants used for the raid on his mansion and arrest in January 2012 were based on Section 131 of the 1994 Copyright Act of New Zealand. “Under the NZ copyright act, online copyright infringement is not a crime,” said Mr Dotcom. “92B of Section 131 – an amendment created by parliament in 2012 – prohibits any criminal sanction against an internet service provider in New Zealand. “In order for the US to be successful with an extradition, the allegation of the crimes that they are charging someone with also have to be a crime in the country from which they request the extradition.”

We must find ways to protect Assange et al.

• Ecuador’s Correa ‘Afraid for Julian Assange’s Safety’ (TeleSur)

Former Ecuadorean president Rafael Correa has warned that WikiLeaks founder Julian Assange’s days are numbered at the Ecuadorean Embassy in London. Correa, who gave Assange asylum back in 2012, said that he’s “afraid for Julian Assange’s safety” due to the new government´s actions with regards to his case. He said that he believes President Lenin Moreno is likely “take away the support” previously afforded to the anti-secrecy activist. “It will only take pressure from the United States to” withdraw protection for Assange and “surely it’s already being done, and maybe they await the results of the Feb. 4 (referendum) to make a decision,” said Correa, in an article published by AFP.

When asked does he have evidence to support his claim, Correa said it’s clear that Moreno “has no convictions, it’s clear that he has yielded to the usual powerbrokers” and will “soon enough yield regarding the question of Assange.” The 54-year old economist added that the ambassador for the United States was shamelessly interfering in Ecuador’s internal affairs, something “hadn’t occurred during ten years” of his government. Earlier this week Correa officially left the ruling PAIS Alliance, the leftist political movement he founded in 2006 and which he first rose to political prominence. Having referred to Moreno as a “traitor,” someone who has called for an “unconstitutional” referendum that could spell an end to “democracy,” Correa went on to say that “they can rob us of Alianza Pais, but never our will and convictions. Despite the pain, this only strengthens us.”

In the future, Manus will be compared to Birkenau.

• Australia Sends Dozens Of Refugees From Pacific Camps To US (AFP)

Dozens of refugees held for years in Australia’s remote Pacific detention camps departed for resettlement in the United States on Tuesday, asylum-seeker advocates said. The Sydney-based Refugee Action Coalition said 40 men flew out from Papua New Guinea’s capital Port Moresby under a deal struck by Australia with former US president Barack Obama but bitterly criticised by his successor Donald Trump. “It was a bitter-sweet moment for the refugees — who on the one hand, are happy to be gaining the freedom that Australia denied them more than four years ago; but on the other, they remain extremely concerned for those that are being left behind,” the advocacy group said in a statement.

The refugees, from camps on Manus Island, flew to Manila from where they will fly on to the US in different groups in the coming weeks before being resettled across the country, it said. The group released photos showing the refugees lining up before dawn to get on buses for the airport, then waiting at the gate to board their flight to Manila. Another 18 men were due to leave Port Moresby in the coming weeks, it said. [..] Canberra sends asylum-seekers who try to reach Australia by boat to detention camps in Manus and the Pacific island of Nauru under a tough policy designed to choke off the flow of refugees to the country. More than 1,000 still remain in limbo in the remote locations.

Canberra has strongly rejected calls to move the refugees to Australia and instead has tried to resettle them in third countries, including the United States. But until now only about 50 refugees have been sent to the US, under an agreement President Trump attacked after taking office as a “dumb deal”. The Refugee Action Coalition said a further 130 people on Nauru have been accepted by the US and are expected to depart next month.

Merkel can’t take that she’s yesterday’s news.

• Angela Merkel Has Completely Reversed Her Refugee Policies (Spiegel)

It’s no longer about people, it’s about a number. It’s about the number of refugees who come to Germany, not about the refugees themselves. The most recent number is 223,000: That’s how many asylum applications were submitted last year, a far cry from the 746,000 applications received in 2016. The new number is rather convenient for Angela Merkel in that it is extremely close to the upper limit of 220,000 that has found its way into the German chancellor’s preliminary coalition outline agreed to by Merkel’s conservatives and the center-left Social Democrats (SPD). This number is the expression of a political policy that has never been clearly verbalized and never been adequately explained. It is the expression of an about-face on refugee policy, away from open borders and toward harsh rejection.

Late in the summer of 2015, Merkel said that if Germany cannot show “a friendly face” in an emergency, “then it is not my county.” She kept the borders open to the incoming refugees, and much of the world was inspired by her humanitarian approach. Now, however, Germany is presenting a much less friendly face to the world. And the German chancellor has no country anymore. But that doesn’t seem to be bothering her. Indeed, her views would seem to have completely changed. In 2016, Merkel engineered a deal with Turkey on behalf of the European Union which essentially shut down the refugee route across the Aegean Sea from Turkey to Greece. She also agreed to demands from the conservative Christian Social Union (CSU), the Bavarian sister party to her own Christian Democrats (CDU), that an annual upper limit be established, though it isn’t allowed to be called an “upper limit.”

In the future, there is also to be a 1,000-per-month upper limit applied to family reunifications for most refugees. That is too low. The CDU and CSU are fond of emphasizing family values, yet they have joined forces to limit family reunification — even though it should be clear to everyone that men have the best chances at integration if they live here together with their families. But none of that matters anymore. The parties only care that the number is low. And SPD leaders are going along without complaint. That, too, is a disappointment.