RT : What is the likelihood that the US will go through with and actually impose economic sanctions on China if it does not implement the new sanctions regime against North Korea? Jim Rogers : Sanctions are sanctions. They could do sanctions which are not very important or don’t do much damage. And then they will have good public relations which says they have sanctions, but it is meaningless. I would suspect if anything, that is what they will start with. If they put sanctions on China in a big way, it brings the whole world economy down. And in the end, it hurts America more than it hurts China because it just forces China and Russia and other countries closer together. Russia and China and other countries are already trying to come up with a new financial system. If America puts sanctions on them, they would have to do it that much faster and in the end America will lose its monopoly on the financial system, which will hurt America more than anybody.

RT : What do you think, is it an empty rhetoric and saber-rattling from Donald Trump because he said “those [UN] sanctions are nothing compared to what ultimately will have to happen” without specifying what he meant by that. Do you think this is just mere bluff on the part of the US, or would it really use the ‘nuclear option’? JR : If it uses a nuclear option for sanctions, it will hurt America much more than will hurt North Korea, it will hurt America much more than it will hurt China, Russia and everybody else. It will force the rest of the world to find an alternative to the US financial system. If he does that, it is going to cause a lot of turmoil in the world financial economy and in the end it is going to hurt America more than it is going to hurt anybody else. I would give you an example, if you look at Russian agriculture right now – America put sanctions on Russian agriculture trying to hurt Russia, but it has helped Russian agriculture. Russian agriculture is booming now. In the end, America has hurt itself more than it has hurt anybody else.

RT : If that happens, what would the consequences be for the global economy? Could this end up becoming a global economic crisis? JR : We are probably going to have a global economic problem, maybe even crisis, in the next couple of years. This may be one of the things that start it. There is always something which starts a crisis. If America does something like this, this could be the thing that did it. In 1929, it started when America started a huge trade war with the rest of the world and the economists said, “please, this is a mistake,” but America did that anyway. And then we had a great collapse and The Great Depression of the 1930s.

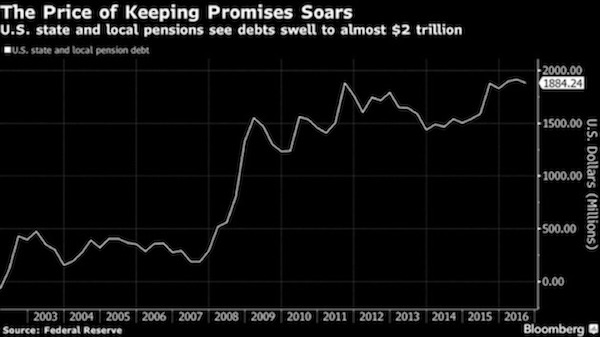

Total unfunded liabilities in state and local pensions have roughly quintupled in the last decade. You read that right – not doubled, tripled or quadrupled: quintupled. That’s nice when it happens on a slot machine, not so nice when it’s money you owe. The graph [shows] that unfunded pension liabilities for state and local governments was $2 trillion. But that assumes an average 7% compound return. What if we assume 4% compound returns? Now the admitted unfunded pension liability is $4 trillion. But what if we have a recession and the stock market goes down by the past average of more than 40%? Now you have an unfunded liability in the range of $7–8 trillion.We throw the words a trillion dollars around, not realizing how much that actually is. Combined state and local revenues for the US total around $2.6 trillion.

Following the next recession (whenever that is), the unfunded pension liabilities for state and local governments will be roughly three times the revenue they are collecting today, and that’s before a recession reduces their revenues. Can you see the taxpayer stuck between a rock and a hard place? Two immovable objects meeting? The math just doesn’t work. Pension trustees don’t face personal liability. They’re literally playing with someone else’s money. Some try very hard to be realistic and cautious. Others don’t. But even the most diligent can’t control when the next recession comes, or when the stock market will crash, leaving a gaping hole in their assets while liabilities keep right on rising. I have had meetings with trustees of various government pensions.

Many of them want to assume a more realistic discount rate, but the politicians in their state literally refuse to allow them to assume a reasonable discount rate, because owning up to reality would require them to increase their current pension funding dramatically. So they kick the can down the road. Intentionally or not, state and local officials all over the US made pension promises that future officials can’t possibly keep. Many will be out of office when the bill comes due, protected from liability by sovereign immunity. We are starting to see cities filing for bankruptcy. That small ripple will be a tsunami within 7–10 years.

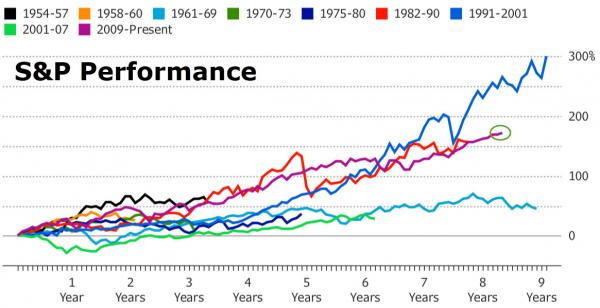

U.S. stocks have risen more in the past eight years than in almost any other post-World War II time of economic growth, as defined by the National Bureau of Economic Research. The logic here is that economic expansions fuel bull markets and so it’s reasonable to measure market recoveries after a period of macro contraction ends. Using that definition, let’s review how the S&P 500 has performed during the last ten economic recoveries. To be precise, the birth of the stock market’s bull market is dated as the first day after an NBER-defined recession has ended. The market run continues through the peak. The S&P 500 Index jumped 172% from July 2009, when the current expansion started, through Wednesday. The biggest advance was about 300% and occurred from April 1991 to March 2001, when Internet-related stocks soared.

As Capital Speculator blog’s James Picerno notes, the question before the house: Will the momentum of late endure long enough to overtake the 1991-2001 record in duration and/or magnitude? If so, the bull market in the here and now has to last another 463 trading days, which translates into a market rally that goes deep into 2019. There’s just one thing wrong… Remember – the ‘market’ is not the ‘economy’… or maybe it is in the new normal?

I provide a simple numerical explanation of how austerity works at the micro (individual person, industrial sector, or country) and the macro level (country, or group of countries in a currency union).

Dan Davies, senior research adviser at Frontline Analysts, argued there’s no point in attempting to value bitcoin as if it were just another type of security. “It’s not a security with some intrinsic value, rather it’s a currency that in the long term is governed by an exchange rate driven by trade or volume of transactions,” Davies said. The fact that a significant proportion of bitcoins is hoarded or held for investment doesn’t disqualify it from being a currency, according to Davies. But the BTC/USD BTCUSD, -3.37% exchange rate is entirely determined by speculative portfolio capital flows right now, he said, leaving it difficult to assign fair value. Viewing bitcoin as a currency makes it possible, at least in theory, to come up with a long-term exchange rate by using the quantity theory of money.

The formula is: MV = PT, where money supply multiplied by its velocity equals the price level multiplied by the transaction volume. Since both price and transaction volume is expressed in U.S. dollars, the price of bitcoin would be 1/BTCUSD, Davies said. In this case, bitcoin’s supply is fixed at 21 million and money velocity for normal currencies is usually at around 10, according to Davies. So, the long-term fundamental value of bitcoin equals the long-term value of transactions that will be carried out in bitcoin divided by 210 million (21 million bitcoins multiplied by velocity). The hardest value to plug into this formula is the transaction volume. If, for example, bitcoin was used primarily for global trade in illicit drugs, the figure would be around $120 billion, which is an estimate the U.N. used in 2014.

“I used that number a few years ago, but we would have to come up with a different estimate, as bitcoin is clearly used for things other than illicit drugs now,” Davies said. Davies declined to offer an updated number, saying he needed to do more research. But doubling that transaction volume number to $240 billion, for example, and dividing by 210 million produces a value of $1,142, around a third of the current exchange rate of $3,569. That isn’t far from an estimate that Mohamed El-Erian, chief economic adviser at Allianz Global Investors, recently suggested as a fair value for bitcoin. In an interview with CNBC, El-Erian said the fair price should be about half or a third of what it is now. El-Erian argued the currency will only survive as a peer-to-peer means of payment and governments won’t allow mass adoption.

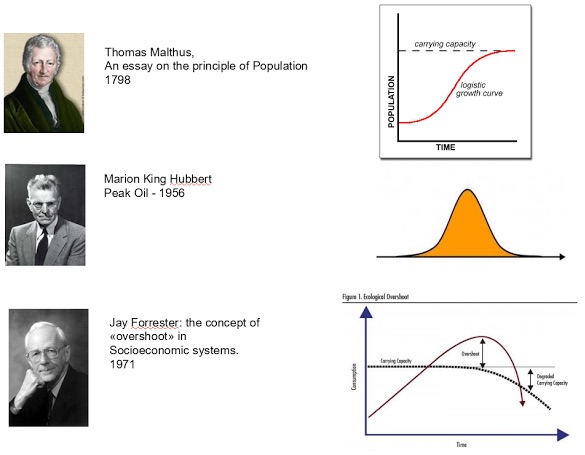

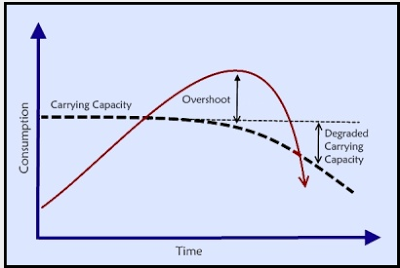

My talk at the Summer Academy of the Club of Rome was mainly a presentation of my latest book, “The Seneca Effect” (Springer 2017). In practice, of course, a book contains many more things than you can say in a 40 minute speech. So, I tried to concentrate on the idea that the behavior I call “the Seneca Curve” is very common, even universal. Below, you can see the Seneca Curve: things go up slowly but collapse rapidly, as the Roman philosopher Seneca said first some two thousand years ago. You may have heard the old Latin motto, “Natura non facit saltus” (Nature doesn’t make jumps) meaning that things change gradually, not abruptly. It may be true in many circumstances but, in practice, it is wholly normal that Nature accumulates energy potentials (as when you inflate a balloon) and then releases them all of a sudden (as when you puncture a balloon).

There are reasons why Nature behaves in this way, but the point I made at the school was not so much about why the curve is so common but how human beings are not normally aware of it. In fact, our thought is often shaped by the idea that things will continue evolving the way they have been evolving up to a certain point. Just think about economic growth, and you’ll notice how economists expect it to continue forever. It goes without saying that the economy is one of those complex systems which are most vulnerable to the Seneca collapse. So, I tried to stress that the understanding that the Seneca Curve exists and it is common is a recent discovery. Even though Seneca had understood it by intuition already almost 2000 years ago, in its modern form it is less than a century old. It was proposed for the first time by Jay Forrester in the 1960s and it was enshrined in “The Limits to Growth” study of 1972, even though the term “Seneca Effect” was not used.

During my talk, I showed this image to evidence how our ideas on the path that complex systems follow evolved over time. You see how modern the idea of “overshoot” (and the subsequent collapse) is. Malthus just didn’t have it. Despite being often accused of catastrophism, he couldn’t envisage societal collapse; he lacked the necessary intellectual tools. He was an optimist! Today, we have this concept. We know that complex systems tend not just to decline, they tend to collapse. But this perception is totally missing in the general debate. When you mention societal collapse, there are two possible reactions. The most common one is that such a thing will never happen.

Then, if you manage to convince people that it is possible, they endeavor to do everything they can to keep the system going; whatever it takes. They don’t realize that when you exceed the carrying capacity of the system, you have to come back, one way or another. And the more you try to stay above the limit, the faster and the harsher the return will be. What you have to do is to ease the collapse, follow it, not try to stop it. Otherwise, it will be worse.

Only business owners with no real estate properties will qualify for a partial write-off of corporate debts in the context of the extrajudicial settlement mechanism. This criterion excludes the owner’s main residence and the production properties, i.e. the professional properties used for the entrepreneurial activity. That was the decision that the technical experts of the country’s creditors are said to have reached with representatives of Greek banks and the Independent Authority for Public Revenue, while there was also convergence on setting the criteria for debt settlement for companies owing between €20,000 and €50,000. In this latter category of debtors, which mostly comprise small enterprises, a standardized procedure will be adopted for assessing repayment capacity and the determination of the amount that the debtor will have to pay on a regular basis.

The Greece firesale will never come anywhere near the €60 billion, but everyone keeps mentioning the number. Their entire railway system went for €45 million. Selling off an entire country is a very bad idea. Europe will find out, but too late.

“It is obvious. Our policies have changed radically, ” says Stergios Pitsiorlas, the deputy economy and development minister, whose airy office is visited daily by bankers, hedge-fund managers and industrialists jockeying for bargains. “Being leftwing doesn’t mean you are also a fool. It doesn’t mean, in the words of Lenin, that we are useful idiots. Let’s speak seriously. Those who complain that Greece is being sold off, that Greece will lose out, don’t know what they are talking about.” Tall, bearded and bespectacled, Pitsiorlas is the point man in Athens’s attempt to raise €60bn (£53bn) through privatisations – sales that, increasingly, have become the focus of international creditors keeping the debt-stricken country afloat. In what has been called the most ambitious sell-off in modern European history, assets ranging from public utilities and transport companies to marinas and hotels are up for grabs.

[..] Privatisations are central to completion of a new round of bailout negotiations with the EU and IMF. Greece’s third, €86bn, rescue programme is due to end next summer and Tsipras has made a clean exit from it, which would herald Athens’s return to the markets, an overarching goal. But hurdles lie ahead. On Friday, eurozone finance ministers warned that continued persecution of the country’s former statistics chief, Andreas Georgiou, could dent international confidence and derail chances of recovery. Officials also raised the prospect of fresh austerity should Greece fail to hit the primary surplus target of 3.5% – a prospect made likely by a huge shortfall in tax revenues. But in a week when the Italians finally took control of Greece’s state-owned train network (acquired by Italy’s own state operator for a paltry €45m) Pitsiorlas is optimistic.

He cites the takeover of Piraeus port by the Chinese shipping conglomerate Cosco as an example of what privatisations can bring: “They will make it the biggest port in Europe and that will boost other professions, create thousands of jobs, revitalise shipyards, which they are also looking at, pave the way to better trains, roads and logistic centres, and trigger development and growth.” In five years, he enthuses, Greece will be a very different place, cosmopolitan and vibrant. “There are rules which need to be observed but ultimately everything will be solved,” he insisted, referring to the obstacles Eldorado and others have encountered. “A miracle will happen. There will be huge change … but the state can’t do it alone, the private sector has to be involved.”

Beijing will suspend construction of major public projects in the city this winter in an effort to improve the capital’s notorious air quality, official media said on Sunday, citing the municipal commission of housing and urban-rural development. All construction of road and water projects, as well as demolition of housing, will be banned from Nov. 15 to March 15 within the city’s six major districts and surrounding suburbs, said the Xinhua report. The period spans the four months when heating is supplied to the city’s housing and other buildings. China is in the fourth year of a “war on pollution” designed to reverse the damage done by decades of untrammelled economic growth and allay concerns that hazardous smog and widespread water and soil contamination are causing hundreds of thousands of early deaths every year.

Beijing has promised to impose tough industrial and traffic curbs across the north of the country this winter in a bid to meet key smog targets. In the capital, it is aiming to reduce airborne particles known as PM2.5 by more than a quarter from their 2012 levels and bring average concentrations down to 60 micrograms per cubic metre. Last year the city experienced near record-high smog in January and February, which the government blamed on “unfavourable weather conditions” Some ‘major livelihood projects’ such as railways, airports and affordable housing may be continued however, providing they are approved by the commission, said the report.

The European Union said President Donald Trump’s administration is shifting its approach to a landmark global agreement on climate change, an assertion which was quickly denied by the White House. The U.S. signaled that it’s no longer seeking to withdraw from the pact and then renegotiate it, but rather wants to re-engage with the Paris Agreement from within, said EU’s climate chief Miguel Arias Canete. He spoke in an interview from Montreal, where the U.S., China, Canada and almost 30 other countries gathered to discuss the most-sweeping accord to date to protect the environment. “Our position on the Paris agreement has not changed. @POTUS has been clear, US withdrawing unless we get pro-America terms,” White House Press Secretary Sarah Huckabee Sanders said on Twitter.

Announcing plans to quit the pact, Trump said in June that the agreement favored other countries at the expense of U.S. workers and amounted to a “massive redistribution” of U.S. wealth. Trump’s administration last month began the formal process of exiting from the climate accord, drawing fire from allies and foes alike. EU climate commissioner Canete made the comments about a change of stance after meeting with Everett Eissenstat, deputy director of the National Economic Council and deputy assistant to the president for international economic affairs. “Now we don’t see the messages that they are withdrawing from the Paris agreement radically,” Canete said, adding that the countries at Saturday’s meeting agreed not to seek a re-negotiation of the Paris deal.

Number 4 in the UK charts, but the BBC refuses to play it. It’s just so well done, and so timely, that none of that matters. It’s 40 years ago that the same happened with the SexPistols’ “God save the Queen”. The BBC ban pushed the song up the charts.

NHS crisis, education crisis, u turns … you can’t trust Theresa May. Let’s get this into the top 40. Download now and force the BBC to play it on our airwaves. All proceeds from downloads of the track between 26th May and 8th June 2017 will be split between food banks around the UK and The People’s Assembly Against Austerity. Download from the following links: (Please note we previously released a version of Liar Liar in 2010 so don’t download the wrong one! Correct track is called ‘Liar Liar GE2017’)

The quality of debate in the 2017 UK General election has been generally terrible. The Tories have been trying to push the “There’s no such thing as a Magic Money Tree” line, and falling straight into the “Don’t think of a pink elephant” problem. This line is known in economic and political circles as The Noble Lie. The Magic Money Tree does exist. They all know it does. When there is a bank to bail out, does anybody ask where the money is coming from? When there is a nuclear missile system that needs building? How about when a foreign nation needs bombing? Like the elephant in the room The Tree cannot be mentioned, because then the electorate might start asking awkward questions about public services – perhaps we should have some? – and taxation – are we overtaxed for the size of government we have, given that we still have people without work?

Once you know about The Tree you might have your politicians delay a casino build and build a hospital instead. You might let the rich people keep their coins, but stop them using them to reserve scare doctors and teachers for their own purposes ahead of the general population. The Tories want to privatise everything, and Labour want to hit rich people hard with taxation sticks. There are no doubt reasons for these fetishes that psychologists would find fascinating. But they are damaging to our nation. They get in the way of doing the job. The debate we should be having is about the size of government we want. And then we instruct our government to provide that. Taxation then is just a thermostat on the wall. You count the bodies in the unemployment queue. If there are too many there is too much taxation and you turn the dial down. If there aren’t any and prices are hotting up, you may have too little taxation so you turn the dial up a little.

Alex Douglas explains in Getting Money out of Politics that the debate is one about resource allocation: “you don’t need to worry about ‘where the money will come from’ to pay for this or that programme or public service. Think about this instead: Are there enough resources to provide the proposed service? Is there enough wood, bricks, glass, PVC, to build new council houses? Is there enough land to build them on? Are there enough builders to build them? If not, are there enough apprenticeships to train them? Are there enough staff in the schools and hospitals? If not, are there enough colleges to train them? If not, are there enough resources to create more of these?” So let’s drop the pretence and get onto the real debate. We know that the last 40 years has been about the magic of the market and that government must constrain itself. It must do as it is told by a small number of unelected technocrats sitting in a central bank ivory tower.

Watch these 6 minutes. And then watch it again and again until you understand it. The world will never look the same. Share it wherever you can. Make people literate.

A nation’s currency is a wonderful, powerful thing. Learn how countries like the U.S.—which issue their own sovereign currency—can afford to use that currency to serve their citizens. Get inspired about our untapped potential, and learn to be less worried about the so-called “national debt”!

Earlier today I came across an article about President Trump’s new budget from Fox News, and in this article the author makes a startling claim… “The hard fact is that the past decade’s $10 trillion in deficit spending has produced the worst economic growth as measured by Gross Domestic Product in our nation’s history. You read that right, in the past decade our nation’s economy grew slower than even during the Great Depression. This stagnant, new normal, low-growth economy is leaving millions of working age people behind who have given up even trying to participate, and has led to a malaise where many doubt that the American dream is attainable.

When I first read that, I thought that this claim could not possibly be true. But I was curious, and so I looked up the numbers for myself. What I found was absolutely astounding. The following are U.S. GDP growth rates for every year during the 1930s…

1930: -8.5%

1931: -6.4%

1932: -12.9%

1933: -1.3%

1934: 10.8%

1935: 8.9%

1936: 12.9%

1937: 5.1%

1938: -3.3%

1939: 8.0%

When you average all of those years together, you get an average rate of economic growth of 1.33%. That is really bad, but it is the kind of number that one would expect from “the Great Depression”. So then I looked up the numbers for the last ten years…

2007: 1.8%

2008: -0.3%

2009: -2.8%

2010: 2.5%

2011: 1.6%

2012: 2.2%

2013: 1.7%

2014: 2.4%

2015: 2.6%

2016: 1.6%

When you average these years together, you get an average rate of economic growth of 1.33%. I thought that was a really strange coincidence, and so I pulled up my calculator and ran all of the numbers again and I got the exact same results. The 1930s certainly had more big ups and downs, but the average rate of economic growth during that decade was exactly the same as we have seen over the past 10 years. And of course the early 1940s turned out to be a boom time for the U.S. economy, while it appears that our rate of economic growth is actually slowing down. As I noted yesterday, U.S. GDP growth during the first quarter of 2017 was just 0.7%.

So could the US of course. The problem in Europe is it’s too late now. Getting it right would be seen as too negative in Germany, and it’s Germany, and Germany alone, that ultimately takes ll the main decisions in the EU.

The Office for National Statistics (ONS) published last week some figures which show how a successful monetary union works in practice. It is not obvious at first sight, from the dry heading: “regional public sector finances”. The ONS collects information on the amounts of public spending and money raised in taxes across the regions of the UK. The difference is the so-called fiscal balance of the region. Only three regions generate a surplus. In London, the South East and the East of England, total tax receipts exceed public spending. The capital has a healthy positive balance of £3,070 per head, followed by the South East at £1,667 per head. Essentially, these two regions subsidise the rest of the UK. Public spending in the North East, for example, is £3,827 per person above the level of taxes raised in that region.

In Wales, it is even higher at £4,545. No wonder that one of the first things Carwyn Jones, leader of the Welsh Assembly, said after the Brexit vote was: “Wales must not lose a penny of subsidy”. The region which benefits most is Northern Ireland, which gets £5,437 per head more than it generates in tax. Scotland, to complete the picture, receives around half of that, at £2,824 per person. There is a lot of debate around Brexit and the border between the North and the Republic of Ireland. There is even talk of reunification, but on these numbers the Republic would be mad to want it. Essentially, the regions receive these subsidies because they are running deficits on their trade balance of payments. The exports of goods and services from the North East, for example, to the rest of the UK are much less than it imports.

In balance of payments jargon, the subsidy it receives is a monetary transfer from the rest of the country, principally from London and the South East. The ONS does not actually produce regional balance of payments statistics. But the fact that most regions receive these large transfers implies that they are just not productive enough to sustain their living standards by their own efforts. All the regions are in the sterling monetary union. Those running trade deficits cannot devalue to try to improve their position. They must instead rely on subsidy. Exactly the same principles apply in the Eurozone. The massive difference of course is that there is no central Eurozone government to make sure the weaker performing regions receive the necessary funding.

This is why President Macron and Chancellor Merkel announced they will examine changes to treaties to allow for further Eurozone integration. Even the hardline German finance minister, Wolfgang Schauble, said: “a community cannot exist without the strong vouching for the weaker ones”. To be sustainable, a monetary union needs large transfers between its regions. London and the South East already put their hands deep into their pockets for the rest of the UK. Gordon Brown did get one thing spectacularly right. He kept us out of the Euro.

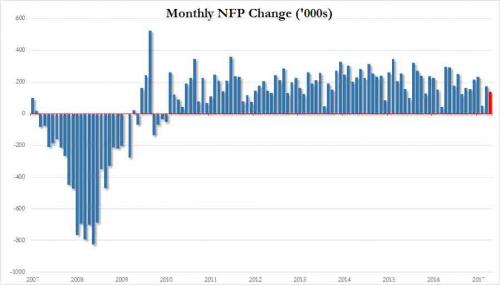

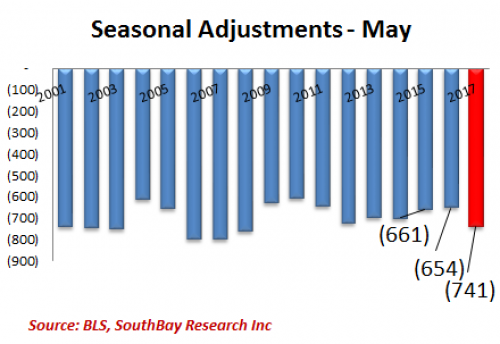

As previewed last night, the jobs “whisper” risk was to the downside, and in what was a very disappointing print released moments ago by the BLS, the whisper was spot on with only 138K jobs added in May, far below the 185K estimate, and below the lowest estimate of 140K. This was the second lowest print going back all the way to last October. Additionally, April’s big beat of 211K was revised substantially lower to only 174K, suggesting that any expectation the Fed may have had of “evidence” the recent economic slowdown was transitory was just crushed.

The change in total payrolls for March was revised down from +79,000 to +50,000, and the change for April was revised down from +211,000 to +174,000. With these revisions, employment gains in March and April combined were 66,000 less than previously reported. This means that over the past 3 months, job gains have averaged 121,000 per month, a far cry from the 181,000 average jobs added over the past 12 months. To be sure, as SouthBay Research points out, a big reason for the unexpected miss was the sharp seasonal adjustment favtor, which was the biggest going back to the financial crisis days:

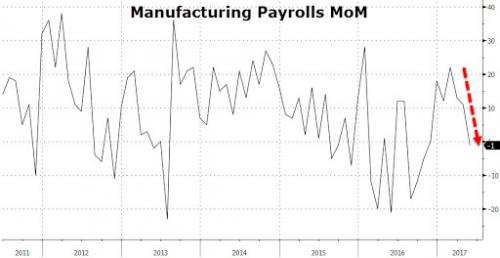

Not helping the Trump agenda, manufacturing jobs declined sharply, posting the weakest growth of 2017.

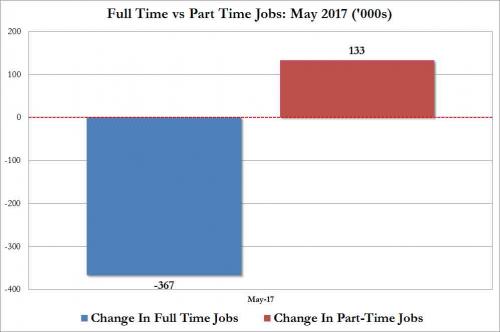

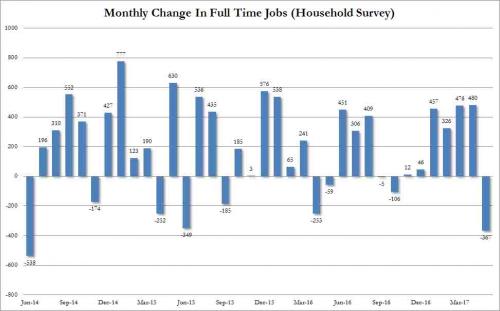

While on the surface, the payrolls report, the wage growth and the unemployment rate (which dropped for all the wrong reasons) were disappointing, a quick look inside the underlying data reveals even more troubling trends, such as that in addition to the number of employed workers dropping by 233K according to the household survey, the composition of these jobs raised even more red flags because in May the US lost 367,000 full time jobs offset by the gain of 133,000 part time jobs.

Putting this number in context, it was the biggest drop in full-time jobs going back to June 2014. And in this context, we are happy to announce that while manufacturing jobs once again declined by 1,000, the waiter and bartender recovery continues to hum along, with 30,000 workers added in “food services and drinking places.”

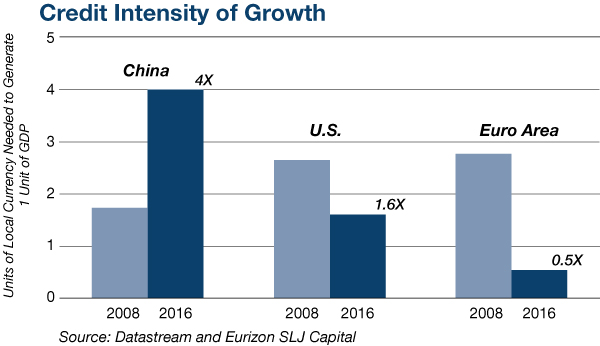

China has reported annual growth rates since the panic of 2008 of between 6.7% and 12.2%, with a steady downward trend since early 2010. If China’s growth engine is running out of steam, as I’ve described, how has China managed to maintain such relatively high growth rates? The answer is contained in three key words: debt, deflation and waste. Waste is a blunt word referring to non-productive investment. The investment component of China’s GDP is about 45% of the total. Most major economies show about 25% to 35% for investment. But at least half the Chinese investment is wasted. It goes to projects that will never produce an adequate return, either on an absolute basis or relative to alternative uses of the funds. If this wasted investment is subtracted from GDP, similar to a one-time write off under general accounting principles, then 8% growth would be 6.2%, and 6% growth would be 4.7%.

[..] Any economy can produce short-term growth by incurring debt and using the proceeds as government spending, tax cuts, investment, or grants. This is nothing more than the classic Keynesian fiscal stimulus with its mystical “multiplier” effect that produces more than $1.00 in aggregate demand for every $1.00 borrowed and spent. In fact, there’s ample evidence that the Keynesian multiplier only exists when an economy is in recession or the very early stages of an expansion, and when its debt levels are relatively low and sustainable. Highly indebted economies in the late stages of an expansion do not conform to Keynes’ theory of a multiplier. Unfortunately for China, it is both highly indebted and has not suffered a recession for eight years. China should therefore expect the GDP multiplier on new debt used for spending or infrastructure to be less than 1.

That is exactly what the data shows. The chart below measures credit intensity defined as the number of units of local currency needed to produce one unit of growth. The local currency metric is a measured by central bank money printing to monetize debt, and is therefore a proxy for the debt itself. The chart shows that in China today, it takes $4.00 of money printing to produce $1.00 of growth. This is up significantly from 2008 when it took $1.70 of money printing to produce $1.00 of growth. This shows that the Keynesian multiplier is less than 1, in fact it’s 0.25 in China today. (Only Europe shows a true multiplier where less than one unit of new money can produce a unit of growth).

A race to the bottom in oil prices may not have many winners, but Russia is certain it can survive. It’s less sure about hedge funds. “We’re actually ready to live forever with the oil price at $40 or below,” Russian Economy Minister Maxim Oreshkin said in a Bloomberg Television interview at the St. Petersburg International Economic Forum on Thursday. “All macroeconomic policy is now based on the assumption of the oil price of $40.” While the world’s biggest energy exporter has made clear it’s hunkering down for years of depressed oil prices, “forever” might be a slight exaggeration, according to the head of Russia’s second-largest bank. Still, “I fully agree with the minister that the oil price is no threat to the economy,” VTB Group CEO Andrey Kostin said during a panel on Friday. As Russia’s future economic plans increasingly converge around crude at that level, Oreshkin says he’s baffled by a more bullish turn taken by hedge funds.

Bets on rising WTI prices jumped the most this year just as Saudi Arabia and Russia were mustering support for the deal they struck in Vienna last month, U.S. Commodity Futures Trading Commission data show. “The oil price within one or two years might be much lower, and those funds which are on the other side of the deals on hedging for one, for two years – they are taking huge risks,” Oreshkin said. Hedge funds’ WTI net-long position – the difference between bets on a price rise and wagers on a drop – rose 20% in the week ended May 23, according to the CFTC. The number had plunged 50% in the previous four weeks. Net-long positions in benchmark Brent – which trades at a small premium to Russia’s Urals export blend – rose 17%, data from ICE Futures Europe showed. Oreshkin questioned “the strategy of those hedge funds” that are striking deals with shale producers for one to two years. “Because the risks are there,” he said.

Instead of reporting precisely what he said, and certainly meant, about fabricated allegations of Russian US election hacking, The Times deliberately misrepresented his recent comments. Interviewed in France by Le Figaro, he repeated what he said many times before. No Russian interference occurred, no evidence suggesting it. “Who is making these allegations,” he asked? “Based on what? If these are just allegations, then these hackers could be from anywhere else and not necessarily from Russia.” Putin knows no hacking occurred. Information was leaked from one or more DNC insiders, no foreign governments involved. He stressed “(i)t makes no sense for (Russia) to do such things. What for?” Speaking to heads of international news agencies on the sidelines of the St. Petersburg Economic Forum, he said “no hackers can influence a foreign election campaign in a significant way.”

“No information leaked this way would resonate with the voters and affect the outcome. We don’t do this at a state level, have no intention of doing it, and on the contrary, we are fighting against it.” He also stressed Moscow’s involvement in creating multi-world polarity. Some countries (meaning US-led Western ones) want Russia contained to further their national interests. “They do this through all kinds of actions that are outside the framework of international law, including economic restrictions,” Putin explained. “Now, they see that this is not working and has produced no results. This irritates them and rouses them into using other methods to pursue their aims and tempts them to up the stakes.” “But we do not go along with these attempts, do not offer pretexts for action. They therefore need to invent pretexts out of nowhere.” Russia, China and Iran are the leading forces against Washington’s hegemonic ambitions – why they’re surrounded by US bases and targeted for regime change.

Addressing the issues of hackers, he said they “can be anywhere…in any country in the world…At the governmental level, we never engage in this. This is what is most important.” He explained attacks can occur from outside Russia made to look like they occurred from its territory. “Modern technology allows that. It is very easy.” It’s a CIA and NSA hacking method to blame Russia, China, Iran or other targeted countries for actions they didn’t commit. “(M)ost important is I am deeply convinced that no hackers can have a real impact on an election campaign in another country,” Putin stressed. “You see, nothing, no information can be imprinted in voters’ minds, in the minds of a nation, and influence the final outcome and the final result.” Those were his recent comments, clearly indicating no Russian direct or indirect involvement in US election hacking or against any other countries.

Instead of reporting what Putin said as I did above, The NYT headlined “Putin Hints at US Election Meddling by ‘Patriotically Minded Russian,” inferring possible state involvement he clearly explained didn’t happen time and again. The Times claimed he “(s)hift(ed) from his previous blanket denials…” False! He did no such thing! The Times: “(H)is comments…were a departure from the Kremlin’s previous position: that Russia had played no role whatsoever in” US election hacking. Fact: His comments repeated what he said many times before, no departure from his position or from any other Russian officials. The Times lied. The Times: “The boundary between state and private action…is often blurry, particularly in matters relating to the projection of Russian influence abroad.”

Again The Times inferred what didn’t happen. If Russian election hacking occurred, incriminating evidence would have been revealed long ago. There’s none, proving accusations are groundless. Instead of truth-telling on this and numerous other vital issues, especially geopolitical ones, notably on Russia, The Times consistently publishes rubbish. Everything it’s reported on alleged Russian US election hacking is disinformation, deception and fake news. Believe none of it.

Owning your own home may be the Kiwi dream but some North Shore homeowners are “drowning in debt” without hope of being mortgage-free. New data from credit information website CreditSimple.co.nz showed North Shore homeowners under 55 had an average debt of $542,600: the highest debt in the country. The information also showed Shore homeowners over 55 still owed an average $381,500. This was the second-highest debt in the country, just behind central Auckland’s older homeowners with an average mortgage of $393,200. Brian Pethybridge, the manager of North Shore Budget Service, was not surprised by the figures. “It’s a phenomenon that’s going to rear it’s head basically because mortgages were $500,000 and now they’re looking at $1 million,” he said. “The options that you had before are limited. It’s a sign of the times.”

According to QV’s latest residential house values, the average house on the Shore was valued at $1.195m, up 8.5% on last year. Pethybridge said many North Shore homeowners were unlikely to pay off their mortgage by the time they retired. Many people’s retirement plans involved selling the house and moving to a cheaper area or a retirement village, he said. But Pethybridge warned there was no guarantee house prices would keep on going up. Another risk was that interest rates could go up and homeowners would not be able to service their mortgage repayments, he said. Banks were already warning people to be prepared to pay 7% interest, and Pethybridge remembered a time when interest rates went “up and up”. Some people were already paying interest-only on their mortgage, meaning the debt was not going down, he said.

To critics of President Donald Trump’s decision to withdraw the U.S. from the Paris climate accord, it may seem like presidential fiat is a very dysfunctional way to do foreign policy. How, exactly, is such overwhelming power consistent with checks and balances? How can one man, even if he is the president, single-handedly alter our international obligations? The short answer is the Constitution, not so much in its origins as in its evolution. It’s an important reminder that the tremendous power of the imperial presidency isn’t an unmitigated good – at least when you don’t like the policies of the person holding office. It’s important to note that President Barack Obama put the U.S. into the Paris climate deal exactly the same way Trump took the U.S. out, namely by unilateral executive action.

Obama couldn’t have gotten two-thirds of the Senate to approve a climate protection treaty. That’s the constitutional requirement for a treaty, as designed by the framers, who for the most part didn’t contemplate that the president would be able to commit the U.S. internationally without the participation of Congress. Understanding that he couldn’t turn the Paris deal into a treaty, Obama turned to a tool used by modern presidents to streamline international deal-making: the executive agreement. An executive agreement doesn’t bring all the domestic legal effects of a treaty. Under the Constitution’s supremacy clause, treaties become the law of the land, which is not the case for executive deals. But that isn’t a huge difference today.

Executive agreements are internationally binding like treaties, because international law isn’t focused on domestic processes like ratification but on the promise to join the compact. The Supreme Court has weakened treaties by requiring explicit language for them to have direct domestic legal effect. And the court has also held that executive agreements can affect some domestic legal rights, a reflection of expanded presidential authority. Indeed, the Paris accord was designed to accommodate the reality that Obama needed to be entering into an executive agreement, not a treaty. It doesn’t call itself a treaty or a protocol but an agreement. And it is in practical terms largely nonbinding, calling for countries to set targets without setting sanctions for noncompliance.

Some conservatives have argued that the Paris accord really is a treaty and should have been submitted to the Senate. But whether they’re right or wrong is a matter courts ordinarily wouldn’t address. Given that Obama entered the Paris accord unilaterally, there isn’t much doubt that Trump can withdraw unilaterally. And liberals who would like to think otherwise would do well to recall that without the executive agreement option, the U.S. wouldn’t have joined the deal in the first place. What’s more remarkable still is that, even if the Senate had approved the Paris accord as a treaty, Trump could have withdrawn without getting the Senate’s consent.

After suffering a devastating election loss to the weakest candidate the GOP has ever had to offer, establishment liberals have stopped at nothing to rationalize their miserable defeat to reality television star Donald J. Trump, even concocting outlandish McCarthyite theories of foreign interference, in what seems to be intentional, purely for the obfuscation of the Democratic Party’s own deficiencies. Bereft of any evidence whatsoever, political elites accused our old Cold War nemesis, Russia, of interfering in the American presidential election to favor the GOP’s Donald Trump over Democratic Party darling Hillary Clinton. Mass liberal outrage and the Democratic Party’s newfound super-patriotism prompted investigation into foreign hacking claims and the Office of the Director of National Intelligence released its intelligence report on Russian interference in early January.

Despite its grandiose promises of revealing irrefutable evidence of the Kremlin’s direct involvement, the ODNI failed to deliver. Although lauded by both establishments as “damning,” the ODNI’s highly publicized intelligence report provided not a shred of evidence linking Russia to the hacking of the DNC; thus, concluding absolutely nothing. Political analysts, journalists, and those bearing at least some critical thinking ability dismissed the report altogether, as the first half contained nothing but baseless assertions, inconsistencies, and contradictions, while the second half was devoted entirely to irrelevant Russia Today bashing.

One would think that the increased potential of nuclear armageddon would dissuade political elites from accusing a nuclear power of such crimes without solid proof, but liberals never cease to amaze. Unfazed by popular skepticism and/or the general lack of evidence of Russia’s involvement, the liberal bourgeoisie, conjuring recycled Cold War sentiments, advanced their partisan crusade against Trump, painting him as some sort of Russian puppet installed to do the unconditional bidding of President Vladimir Putin. Eleven months have passed since the birth of these Russian hacking conspiracies, but the Trump-Russia non-scandal has persisted to dominate American political discourse ever since — with skepticism in the minority, surviving as fringe thought, at best. Trump’s actual conflicts of interest and legitimate criticism of his policies have drowned into irrelevance as his every tweet receives 24×7 coverage and the liberal mainstream media entertains any and every conspiracy theory of Russian collusion known to man.

“Did incoming officials in earlier election transitions never meet with Russian diplomats on the way to assuming their duties? And if they did meet, what do you suppose they talked about? The Baltimore Orioles pitching prospects?”

The extraordinary thought disorders of this moment in history are equally distributed across the political spectrum. They’re an inevitable product of what Sigmund Freud identified as the discontents of civilization, but they grow especially acute as that civilization enters an economic crack-up zone. The craziness is equally distributed while the nation’s wealth is not. The old middle, or center, is imploding both economically and psychologically, concentrating distortions of reality at each end, Left and Right. The disordered thought in Trumpism is as self-evident as (a) covfefe, though it came into being out of the authentic pain of those classes that bear the brunt of accelerating collapse. The thought disorders among Trump’s adversaries interest me more, because they emanate from the far more educated ranks of society, the place where rational leadership is supposed to spawn.

If you can’t depend on those people to think straight in difficult times, then it raises the question of what exactly is the value of an advanced education? For instance: the incredible new idea put out by CNN that it is verboten for officials in the government — the president especially — to meet with the Russian ambassador to the United States. I’ve asked this question before, but obviously it needs to be repeated in the face of this persistent nonsense: why do you think nations send diplomats to other lands if not to meet with and communicate with government officials? Since when — and why — are we shocked that a US president would meet in the White House with the Russian ambassador and foreign minister? Did previous presidents not meet with Russian diplomats? Did incoming officials in earlier election transitions never meet with Russian diplomats on the way to assuming their duties?

And if they did meet, what do you suppose they talked about? The Baltimore Orioles pitching prospects? The newest fusion cuisine? Or serious matters of mutual geopolitical interest? Do American diplomats in Moscow avoid meeting with Russian leaders? Why do we even bother to send them there? Whether it is a misunderstanding of reality by the educated people who work on Cable TV news, or a malicious twisting of the public’s credulity, it is producing a grievous breakdown in collective coherence with the potential of causing enormous political mischief in American life. The Dem/Prog “resistance” may think that it is taking a bold stand against a rogue government, but it is only making itself look dangerously unreliable as a supposed alternative to Trumpism.

EU member states can use public funds to help struggling banks dispose of soured loans, but only within the limits of laws put in place since the financial crisis, according to an EU report. While EU law normally stipulates that the need for “extraordinary public financial support” means a bank is failing and should be wound down, an exception is made for temporary state aid, known as a precautionary recapitalization, to address a capital shortfall identified in a stress test. “It seems conceivable” for governments to use such aid to finance an impaired-asset measure, the May 31 report states. The document says the conditions in EU law for giving state aid to a solvent bank must be observed.

“Dealing with the issue of high NPLs should not imply any deviation from the rules of the banking union,” it states, referring to the package of laws intended to bolster financial stability and deepen integration in the bloc. Andrea Enria, head of the European Banking Authority, has been one of the most vocal proponents of allowing state aid for banks that incur losses in the course of selling bad loans. He told EU lawmakers in April that state aid could be used to “deal promptly and decisively with the significant legacy of asset-quality problems in the European banking sector, which remains a drag on the EU economy.” Freeing up public money to offset banks’ losses could help to chip away at the €1 trillion bad-debt mountain and could smooth the way for bailouts in the EU’s hardest-hit countries, including Cyprus, Portugal and Italy.

Construction work on a $7.9bn project to develop a sprawling coastal Olympics complex and Athens’s former airport will begin in six months, the Greek government has said. State minister Alekos Flabouraris said on Friday that the leftist administration’s privatisation agency had given the go-ahead to a consortium of Abu Dhabi and Chinese investors backed by the Chinese conglomerate Fosun, which owns 12% of the British holiday company Thomas Cook, to turn the site into a major resort. It had been earmarked as a metropolitan park but was largely abandoned for the past decade. Now the consortium plans to build a 200-hectare (494-acre) park along with apartments, hotels and shopping malls at the site, which also includes some venues from the 2004 Olympics.

Greece committed to sell off state assets under the terms of the international bailout keeping its economy afloat since 2010. Its main private property developer, Lamda, signed a deal in 2014 to build on the Hellenikon coastal area, in one of Europe’s biggest real estate development projects. The announcement came as Greece’s statistics service, Elstat, said the economy expanded in the first three months of 2017, upwardly revising a previous flash estimate in May that showed a 0.1% quarterly contraction. Data showed the economy grew by 0.4% in January to March compared with the final quarter of 2016 when GDP contracted by 1.1%. [..] Under a deal with its EU/IMF lenders, Athens needs to speed up the Hellenikon investment and address any forestry and archaeological issues.

It’s done. Bannon 1 – 0 Kushner. President Donald Trump announced the U.S. would withdraw from the Paris climate pact and that he will seek to renegotiate the international agreement in a way that treats American workers better. “So we are getting out, but we will start to negotiate and we will see if we can make a deal, and if we can, that’s great. And if we can’t, that’s fine,” Trump said Thursday, citing terms that he says benefit China’s economy at the expense of the U.S. “In order to fulfill my solemn duty to protect America and its citizens, the United States will withdraw from the Paris climate accord, but begin negotiations to re-enter either the Paris accord or really an entirely new transaction on terms that are fair to the United States, its businesses” and its taxpayers, Trump said.

As Bloomberg reports, Trump’s announcement, delivered to cabinet members, supporters and conservative activists in the White House Rose Garden, spurns pleas from corporate executives, world leaders and even Pope Francis who warned the move imperils a global fight against climate change. As we noted earlier, we should prepare for the establishment to begin its mourning and fearmongering of the disaster about to befall the world. Pulling out means the U.S. joins Russia, Iran, North Korea and a string of Third World countries in not putting the agreement into action. Just two countries are not in the deal at all – one of them war-torn Syria, the other Nicaragua. The Hill notes that many Republicans on Capitol Hill are likely to support pulling out of the Paris deal – 20 leading Senate Republicans, including Majority Leader Mitch McConnell (R-Ky.) asked Trump to do just that last week.

Withdrawing from Paris would greatly please conservative groups, which have orchestrated an all-out push in opposition to the pact. “Without any impact on global temperatures, Paris is the open door for egregious regulation, cronyism, and government spending that would be disastrous for the American economy as it is proving to be for those in Europe,” said Nick Loris, a fellow at the Heritage Foundation. “It is time for the U.S. to say ‘au revoir’ to the Paris agreement,” he said.

And use to NOT have their leader appear on TV. I’m thinking a decision by the new (American?!) campaign team installed after the Snap announcement. “Stay away from the camera, it can only do you harm!” Boris PM by July 1?

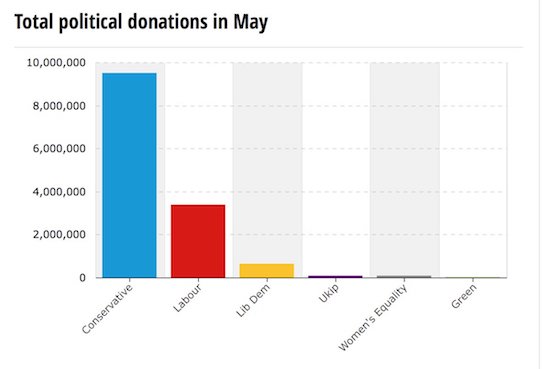

The Conservatives raised more than 10 times as much as Labour last week, partly thanks to a donation of over £1m from the theatre producer behind The Book of Mormon and The Phantom of the Opera. John Gore, whose company has produced a string of hit musicals, gave £1.05m as part of the £3.77m received by the Conservatives in the third week of the election campaign. In the same time, Labour received only £331,499. The Electoral Commission only publishes details of donations over £7,500, so the smaller donors who make up most of Labour’s fundraising are not identified. Almost all Labour’s larger donations came from unions, including £159,500 from Unite. The new figures show the Conservatives have received £15.2m since the start of 2017, while Labour has received £8.1m.

The large donations came as the poll lead held by the Conservatives and Theresa May appeared to fall following controversies around her social care policy. In the week starting 17 May, the Liberal Democrats received £310,500, of which £230,000 came from the Joseph Rowntree Reform Trust and £25,000 came from the former BBC director general Greg Dyke. The Women’s Equality party received £71,552, with Edwina Snow, the Duke of Westminster’s sister who is married to the historian Dan Snow, giving £50,000. Ukip’s donations fell dramatically to £16,300 from £35,000 the previous week. Political parties can spend £30,000 for every seat they contest during the regulated period. There are 650 seats around the country, meaning that parties can spend up to £19.5m during the regulated period in the run-up to the election.

Befitting a surprise election, the manifestos from the main parties contained surprises. Labour is shaking off decades of shyness about nationalisation and tax increases for the rich and for the first time in decades has a policy agenda that is not Tory-lite. The Conservatives, meanwhile, say they are rejecting “the cult of selfish individualism” and “belief in untrammelled free markets”, while adopting the quasi-Marxist idea of an energy price cap. Despite these significant shifts, myths about the economy refuse to go away and hamper a more productive debate. They concern how the government manages public finances – “tax and spend”, if you will.

The first is that there is an inherent virtue in balancing the books. Conservatives still cling to the idea of eliminating the budget deficit, even if it is with a 10-year delay (2025, as opposed to George Osborne’s original goal of 2015). The budget-balancing myth is so powerful that Labour feels it has to cost its new spending pledges down to the last penny, lest it be accused of fiscal irresponsibility. However, as Keynes and his followers told us, whether a balanced budget is a good or a bad thing depends on the circumstances. In an overheating economy, deficit spending would be a serious folly. However, in today’s UK economy, whose underlying stagnation has been masked only by the release of excess liquidity on an oceanic scale, some deficit spending may be good – necessary, even.

The second myth is that the UK welfare state is especially large. Conservatives believe that it is bloated out of all proportion and needs to be drastically cut. Even the Labour party partly buys into this idea. Its extra spending pledge on this front is presented as an attempt to reverse the worst of the Tory cuts, rather than as an attempt to expand provision to rebuild the foundation for a decent society. The reality is the UK welfare state is not large at all. As of 2016, the British welfare state (measured by public social spending) was, at 21.5% of GDP, barely three-quarters of welfare spending in comparably rich countries in Europe – France’s is 31.5% and Denmark’s is 28.7%, for example. The UK welfare state is barely larger than the OECD average (21%), which includes a dozen or so countries such as Mexico, Chile, Turkey and Estonia, which are much poorer and/or have less need for public welfare provision. They have younger populations and stronger extended family networks.

The third myth is that welfare spending is consumption – that it is a drain on the nation’s productive resources and thus has to be minimised. This myth is what Conservative supporters subscribe to when they say that, despite their negative impact, we have to accept cuts in such things as disability benefit, unemployment benefit, child care and free school meals, because we “can’t afford them”. This myth even tints, although doesn’t define, Labour’s view on the welfare state. For example, Labour argues for an expansion of welfare spending, but promises to finance it with current revenue, thereby implicitly admitting that the money that goes into it is consumption that does not add to future output.

The banker at the other end of the phone line was furious, recalled Shanghai lawyer Wang Chaoyu. A pile of steel pledged as collateral for a loan of almost $3 million from his bank, China CITIC, had vanished from a warehouse on the outskirts of the city. Just several months earlier, in mid-2013, Wang and the banker had visited the warehouse and verified that the steel was there. “The first time I went, I saw the steel,” recalled Wang, an attorney at Beijing DHH Law Firm, which represents the Shanghai branch of CITIC. “Afterwards, the banker got in contact with me and said, ‘The pledged assets are no longer there.’” The trouble had begun in 2012, after CITIC loaned the money to Shanghai Hanning Iron and Steel, a privately held steel trader. Hanning failed to meet payments, according to a mediation agreement reviewed by Reuters, and CITIC took ownership of the steel.

It was when CITIC moved to retrieve the collateral that the banker visited the warehouse and discovered that the 291-tonne pile of steel was no longer there, Wang said. The bank is still in court trying to recoup its losses. The missing collateral is a setback for CITIC. But it is indicative of a much wider problem that could endanger the health of China’s financial system – fraudulent or “ghost” collateral. When bank auditors in China go looking, they too often find that collateral recorded on the books simply isn’t there. In some cases, collateral that has been pledged simply doesn’t exist. In others, it disappears as borrowers in financial distress sell the assets. There are also instances in which the same collateral has been pledged to multiple lenders. One lawyer said he discovered that the same pile of steel was used to secure loans from 10 different lenders.

With the mainland facing its slowest growth in over a quarter of a century, defaults are mounting as borrowers struggle to repay their loans. The danger of fraudulent collateral in this situation, say economists, is that it exacerbates the problem of bad debt for China’s banks, increasing the risk of financial turmoil. As growth slows, lenders can expect more nasty surprises, said Xin Qingquan at Chongqing University. More instances of fake collateral will arise, he said. [..] There are no official statistics or estimates of the problem. But fraudulent collateral is “a huge issue,” said Violet Ho, co-head of Greater China Investigations and Disputes Practice at Kroll, which conducts corporate investigations on the mainland. “Often you also see that the paperwork around collateral may be dodgy, and the bank loan officer knows, the intermediary knows, and the goods owner knows – so it’s essentially a Ponzi scheme.”

[..]Bad loans are mounting fast. Officially, just 1.74% of commercial bank loans were classified as non-performing at the end of March. But some analysts say lenders often mask the true level of bad debt and so the figure is likely much higher. Fitch Ratings said in a report last September that it had estimated non-performing loans in China’s financial system could be as high as 15% to 21%. This in a banking sector that has undergone a massive credit expansion. The value of outstanding bank loans ballooned to $17.2 trillion at the end of April from $5.8 trillion at the end of 2009, according to data from China’s central bank. In September last year, the Bank for International Settlements warned that excessive credit growth in China meant there was a growing risk of a banking crisis in the next three years.

The Bank of Japan’s assets apparently exceeded 500 trillion yen ($4.49 trillion) as of the end of May, growing to rival the country’s economy as the central bank continues its debt purchases under an ultraeasy monetary policy. The bank’s total assets stood at 498.15 trillion yen as of May 20. By the time the month ended Wednesday, its holdings of Japanese government bonds had increased by another 2.24 trillion yen. Assuming that the BOJ had not significantly reduced its non-JGB assets, its balance sheet almost certainly crossed over the 500 trillion yen mark into uncharted territory. The BOJ’s balance sheet began expanding at a rapid clip after Governor Haruhiko Kuroda launched unprecedented quantitative and qualitative easing in April 2013. At around 93%, the scale of the Japanese central bank’s assets in proportion to GDP has no close match. Latest data shows that the U.S. Fed held roughly $4.5 trillion in assets, which is equivalent to 23% of the country’s GDP.

The ECB’s balance sheet, at about €4.2 trillion ($4.71 trillion) is larger than the BOJ’s, but it still sits at around 28% of the eurozone GDP. The BOJ in September shifted its policy focus from QE to controlling the yield curve, but the bank is still snapping up JGBs to keep long-term rates at around zero. The central bank has stood firm on its pledge to continue expanding its balance sheet to boost currency supply until Japan’s consumer price inflation is steadily above 2%. This suggests that the BOJ’s balance sheet will continue expanding past the 500 trillion yen mark. This prospect makes some financial experts uneasy. Once the inflation target is finally met, and the BOJ starts raising interest rates, the bank will have to pay more in interest to financial institutions’ reserve deposits than it will earn from its low-yielding JGB holdings.

Between 20% and 25% of the nation’s shopping malls will close in the next five years, according to a new report from Credit Suisse that predicts e-commerce will continue to pull shoppers away from bricks-and-mortar retailers. For many, the Wall Street firm’s finding may come as no surprise. Long-standing retailers are dying off as shoppers’ habits shift online. Credit Suisse expects apparel sales to represent 35% of all e-commerce by 2030, up from 17% today. Traditional mall anchors, such as Macy’s, J.C. Penney and Sears, have announced numerous store closings in recent months. Clothiers including American Apparel and BCBG Max Azria have filed for bankruptcy. Bebe has closed all of its stores.

The report estimates that around 8,640 stores will close by the end of the year. Retail industry experts say Credit Suisse may have underestimated the scope of the upheaval. “It’s more in the 30% range,” Ron Friedman, a retail expert at accounting and advisory firm Marcum said of the share of malls that he predicts will close in the next five years. “There are a lot of malls that know they’re in big trouble.” By ignoring new shopping centers being built, the research note took an overly simplistic view of the changing landscape of shopping centers, said analyst David Marcotte, senior vice president with Kantar Retail. “There are still malls being built,” Marcotte said. “Predominantly outlet malls and lifestyle malls.”

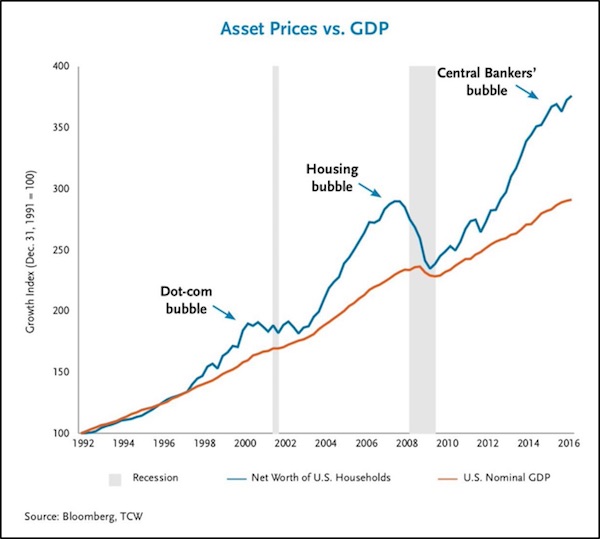

Now don’t get me wrong. Do I think Emmanuel Macron, a former Rothschild investment banker whose “ambition was always two steps ahead of his experience”, is the second coming of Charles de Gaulle? Do I think Donald freakin’ Trump is a modern day Andrew Jackson? Bwa-ha-ha-ha-ha-ha … good one! But here’s what I do think: • Something old and powerful is happening in the real world to crush the status quo political systems of every Western democracy. • Something predictably sad is happening in the political world to replace the old guard candidates with self-absorbed plutocrats like Trump and pretty boy bankers like Macron. • Something new and powerful is happening in the investment world to divorce political risk and volatility from market risk and volatility. The old force repeating itself in the real world is nicely summed up by these two charts, the most important charts I know. They’re specific to the U.S., but applicable everywhere in the West.

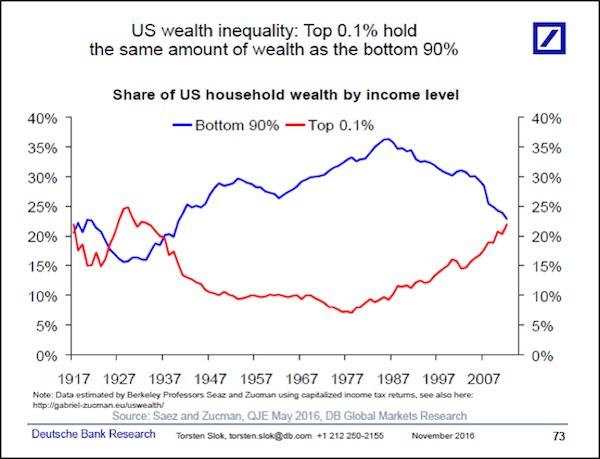

First, the Central Banker’s Bubble since March 2009 and the launch of QE1 has inflated U.S. household wealth far beyond what the nominal growth rate of the U.S. economy would otherwise support. This is a classic bubble in every sense of the word, with the primary difference from prior vast bubbles being its concentration and focus in financial assets — stocks and bonds — which are held primarily by the rich. Who wins the Academy Award for creation of wealth inequality in a supporting role? Ladies and gentlemen, I give you the U.S. Federal Reserve.

And as the second chart shows, this central bank largesse has sharply accelerated the massive shift in wealth to the Rich from the Rest, a shift which began in the 1980s with the Reagan Revolution. We are now back to where we were in the 1930s, where the household wealth of the bottom 90% of U.S. wage earners is equal to the household wealth of the top one-tenth of 1% of U.S. wage earners.

So look … I’m not saying that the current level or dynamics of wealth inequality is a good thing or a bad thing. I’m just saying that it IS. And I understand that there are insurance programs today, like social security and pension funds, which are not reflected in this chart and didn’t exist in the 1930s, the last time you saw this sort of wealth inequality. I understand that there are a lot more people in the United States today than in the 1930s. I understand that there are all sorts of important differences in the nature of wealth distribution between today and the 1930s. I get all that. What I’m saying, though, is that just like in the 1930s, there is a political price to be paid for this level of wealth inequality. That price is political polarization and electoral rejection of status quo parties.

[..] downgrades of bonds issued by local governments raise the interest rates those governments must pay on holders of its debt, thereby costing those communities up to hundreds of millions of dollars annually, according to the report, which was released Wednesday by the non-profit Roosevelt Institute’s ReFund America Project and focused on recent downgrades by Moody’s in relatively impoverished, predominantly-black localities. The more recent report [..] took a granular look at a few communities whose budgets were impacted by downgrades, which drive the prices of bonds down while raising the interest rate at which the government has to pay its bondholders. New Jersey was set to lose $258 million annually as a result of a Moody’s ratings drop, the report calculated, using the spread between interest rates on bonds with different Moody’s credit ratings and the amount of debt affected by the downgrade.

Moody’s announced a downgrade of the New Jersey’s $37 billion in publicly-issued debt to A3, six levels below the agency’s top rating of Aaa, in late March. The agency attributed the downgrade to “significant pension underfunding, including growth in the state’s large long-term liabilities, a persistent structural imbalance and weak fund balances,” as well as a tax cut that would decrease revenues by $1.1 billion over the next four years. New Jersey’s city of Newark — which is 52.4% African American and 33.8% Hispanic, compared to 12.6% and 16.3%, respectively, on the national level, according to U.S. Census data — was slated to lose an estimated $10 million annually as a result of a Moody’s downgrade, the report calculated. Newark’s median household income was just over $33,000, compared to nearly $54,000 nationwide, as of 2015.

That year, Moody’s downgraded Newark’s $374 million in general obligation unlimited tax bonds to Baa3, one level above junk bond status. The rating change, Moody’s said in the press release, reflected “the city’s further weakened financial position since last year,” along with its “reliance on market access for cash flow, history of aggressively structured budgets typically adopted late in the year and uncertainty around continued financial support from the state of New Jersey.” Further west, Chicago Public Schools (CPS) also stood to suffer tremendously from a Moody’s rating drop. The report authors calculated that the school system would lose out on $290 million annually from a September 2016 Moody’s downgrade to B3, five ranks below the highest junk bond rating. Nearly 40% of students are African American, 46.5% are Hispanic and 80.2% are considered “economically disadvantaged,” according to October 2016 CPS data.

Illinois had its bond rating downgraded to one step above junk by Moody’s Investors Service and S&P Global Ratings, the lowest ranking on record for a U.S. state, as the long-running political stalemate over the budget shows no signs of ending. S&P warned that Illinois will likely lose its investment-grade status, an unprecedented step for a state, around July 1 if leaders haven’t agreed on a budget that chips away at the government’s chronic deficits. Moody’s followed S&P’s downgrade Thursday, citing Illinois’s underfunded pensions and the record backlog of bills that are equivalent to about 40% of its operating budget. “Legislative gridlock has sidetracked efforts not only to address pension needs but also to achieve fiscal balance,” Ted Hampton, Moody’s analyst, said in a statement.

“During the past year of fruitless negotiations and partisan wrangling, fundamental credit challenges have intensified enough to warrant a downgrade, regardless of whether a fiscal compromise is reached.” Illinois hasn’t had a full year budget in place for the past two years amid a clash between the Democrat-run legislature and Republican Governor Bruce Rauner. That’s left the fifth most-populous state with a record $14.5 billion of unpaid bills, ravaged entities like universities and social service providers that rely on state aid and undermined Illinois’s standing in the bond market, where investors have demanded higher premiums for the risk of owning its debt. Moody’s called Illinois “an outlier among states” after suffering eight downgrades in as many years.

“The rating actions largely reflect the severe deterioration of Illinois’ fiscal condition, a byproduct of its stalemated budget negotiations,” S&P analyst Gabriel Petek said in a statement. “The unrelenting political brinkmanship now poses a threat to the timely payment of the state’s core priority payments.” Illinois’s 10-year bonds yield 4.4%, 2.5 percentage points more than those on top-rated debt. That spread – a measure of the perceived risk – is the highest since at least January 2013 and more than any of the other 19 states tracked by Bloomberg.

Uber reported yesterday that its NET LOSS totaled more than $700 million last quarter, despite pulling in a whopping $3.4 billion in revenue. (This means they spent at least $4.1 billion!) That’s the latest in a string of massive, 9-figure quarterly losses for the company. The only question I have is– how much cocaine are these people buying? Seriously, it’s REALLY HARD to spend so many billions of dollars. You could have over 100,000 employees (‘real’ employees, not Uber drivers) and pay them $150,000 EACH and still not blow through that much money in a single quarter. Even if you think about Research & Development, Uber still managed to burn through almost as much cash as NASA’s $4.8 billion budget last quarter. The real irony is that this company is worth $70 BILLION. And Uber is far from alone. Netflix is also worth $70 billion; and like Uber, they can’t make money.

Over the last twelve months Netflix burned through over $1.7 billion in cash, and they made up for it by going deeper into debt. The list goes on and on– Snapchat debuted with a $30 billion valuation after its IPO, only to subsequently report that they had lost $2.2 billion in the previous quarter. Telecom company Sprint is still somehow worth more than $30 billion despite having over $40 billion in debt and burning through more than $6 billion over the last three years. And then there’s Twitter, a rudderless, profitless company that is still worth over $13 billion. This is pure insanity. If companies that burn through obscene piles of cash and have no clear path to profitability are worth tens of billions of dollars, it seems like any business that’s cashflow positive should be worth TRILLIONS. None of this makes any sense, and investing in this environment is nothing more than gambling. Sure, it’s always possible these companies’ stock prices increase even more. Maybe Netflix and Twitter quadruple despite continuing losses and debt accumulation. Maybe Bitcoin surges to $50,000 next month. And maybe the Dallas Cowboys finally offer me the starting quarterback position next season.

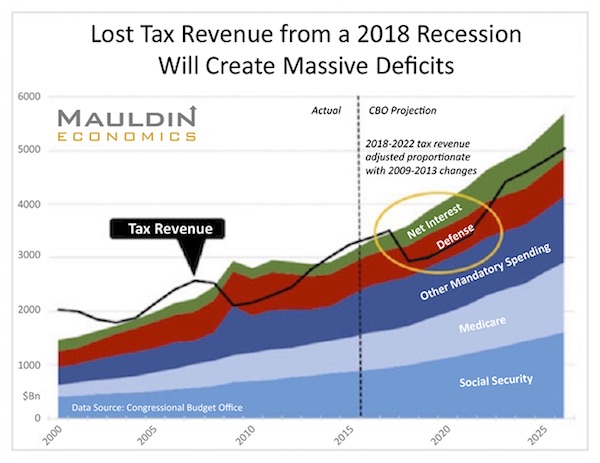

Sometime this year, world public and private plus unfunded pensions will surpass $300 trillion. That is not even counting the $100 trillion in US government unfunded liabilities. Oops. These obligations cannot be paid. A time is coming when the market and voters will realize this. Will voters decide to tax “the rich” more? Will they increase their VAT rates and further slow growth? Will they reduce benefits? No matter what they decide, hard choices will bring political turmoil. And that, of course, will mean market turmoil. We are coming to a period I call “the Great Reset.” As it hits, we will have to deal, one way or another, with the largest twin bubbles in the history of the world. One of those bubbles is global debt, especially government debt. The other is the even larger bubble of government promises.

The other is the even larger bubble of government promises. History shows it is more than likely that the US will have a recession in the next few years. When it does come, it will likely blow the US government deficit up to $2 trillion a year. Obama took eight years to run up a $10 trillion debt after the 2008 recession. It might take just five years after the next recession to run up the next $10 trillion. Here is a chart my staff at Mauldin Economics created in late 2016 using Congressional Budget Office data. It shows what will happen in the next recession if revenues drop by the same percentage as they did in the last recession (without even counting likely higher expenditures this time).

And you can add the $1.3 trillion deficit in this chart to the more than $500 billion in off-budget debt—and add a higher interest rate expense as interest rates rise. The catalyst could be a European recession that spills over into the US. Or it might be one triggered by US monetary and fiscal mistakes. Or a funding crisis in China, or an emerging-market meltdown. Whatever the cause, the next recession will be just as global as the last one. And there will be more buildup of debt and more political and economic chaos.

The price of raw ivory in Asia has fallen dramatically since the Chinese government announced plans to ban its domestic legal ivory trade, according to new research seen by the Guardian. Poaching, however, is not dropping in parallel. Undercover investigators from the Wildlife Justice Commission (WJC) have been visiting traders in Hanoi over the last three years. In 2015 they were being offered raw ivory for an average of US$1322/kg in 2015, but by October 2016 that price had dropped to $750/kg, and by February this year prices were as much as 50% lower overall, at $660/kg. Traders complain that the ivory business has become very “difficult and unprofitable”, and are saying they want to get rid of their stock, according to the unpublished report seen by the Guardian. Worryingly, however, others are stockpiling waiting for prices to go up again.

Of all the ivory industries across Asia, it is Vietnam that has increased its production of illegal ivory items the fastest in the last decade, according to Save the Elephants. Vietnam now has one of the largest illegal ivory markets in the world, with the majority of tusks being brought in from Africa. Although historically ivory carving is not considered a prestigious art form in Vietnam, as it is in China, the number of carvers has increased greatly. The demand for the worked pieces comes mostly from mainland China. Until recently, the chances of being arrested at the border slim due to inefficient law enforcement. But the prices for raw ivory are now declining as the Chinese market slows; this is partly due to China’s economic slowdown, and also to the announcement that the country will close down its domestic ivory trade.