Arthur Rothstein General store and railroad crossing, Atlanta, Ohio 1938

And don’t you ever forget it.

• If Things Were Bad in 2008… What’s Coming Will be Far Far Worse (Phoenix)

For six years, the world has operated under a complete delusion that Central Banks somehow fixed the 2008 Crisis. All of the arguments claiming this defied common sense. A 5th grader would tell you that you cannot solve a debt problem by issuing more debt. We’ve just added another $10 trillion in debt to the US system. Similarly, anyone with a functioning brain could tell you that a bunch of academics with no real-world experience, none of whom have ever started a business or created a single job can’t “save” the economy.

However, there is an AWFUL lot of money at stake in believing these lies. So the media and the banks and the politicians were happy to promote them. Indeed, one could very easily argue that nearly all of the wealth and power held by those at the top of the economy stem from this fiction. So it’s little surprise that no one would admit the facts: that the Fed and other Central Banks not only don’t have a clue how to fix the problem, but that they actually have almost no incentive to do so. So here are the facts:

1) The REAL problem for the financial system is the bond bubble. In 2008 when the crisis hit it was $80 trillion. It has since grown to over $100 trillion.

2) The derivatives market that uses this bond bubble as collateral is over $555 trillion in size.

3) Many of the large multinational corporations, sovereign governments, and even municipalities have used derivatives to fake earnings and hide debt. NO ONE knows to what degree this has been the case, but given that 20% of corporate CFOs have admitted to faking earnings in the past, it’s likely a significant amount.

4) Corporations today are more leveraged than they were in 2007. As Stanley Druckenmiller noted recently, in 2007 corporate bonds were $3.5 trillion… today they are $7 trillion: an amount equal to nearly 50% of US GDP.

5) The Central Banks are now all leveraged at levels greater than or equal to where Lehman Brothers was when it imploded. The Fed is leveraged at 78 to 1. The ECB is leveraged at over 26 to 1. Lehman Brothers was leveraged at 30 to 1.

6) The Central Banks have no idea how to exit their strategies. Fed minutes released from 2009 show Janet Yellen was worried about how to exit when the Fed’s balance sheet was $1.3 trillion (back in 2009). Today it’s over $4.5 trillion.

We are heading for a crisis that will be exponentially worse than 2008. The global Central Banks have literally bet the financial system that their theories will work. They haven’t. All they’ve done is set the stage for an even worse crisis in which entire countries will go bankrupt. The situation is clear: the 2008 Crisis was the warm up. The next Crisis will be THE REAL Crisis. The Crisis in which Central Banking itself will fail.

$50 trillion of zombie money in the US alone. It WILL go poof.

• The Warren Buffet Economy – Why Its Days Are Numbered-Part 2 (David Stockman)

[..] .. once Greenspan took the helm and his apparently atavistic embrace of gold standard money melted-down under the Wall Street furies of October 1987, the finance ratio erupted. As shown below, it has never looked back and at 5.5X national income has reached a point that would have been unimaginable on the morning of Black Monday. Stated differently, under a regime of honest money and market determined financial prices, the combined value of corporate equities and credit market debt would not have mushroomed by 8X – from $11 trillion to $93 trillion – during the past 27 years.

For crying out loud, the nominal GDP grew by only 3.5X during the identical span. In effect, the US economy has been capitalized at higher and higher rates for no ascertainable reason of fundamental economics. Indeed, there is no reason why the 260% ratio of equity and credit market debt to GDP that was recorded in 1986 should have risen at all. At that point Paul Volcker had completed his historic task of extinguishing runaway commodity and CPI inflation and had superintended a solid recovery of real economic growth. Arguably, therefore, the US economy was carrying about the right amount of finance. And, at that healthy ratio, today’s $17.7 trillion economy would be carrying about $43 trillion of combined market equity and credit market debt.

In a word, the Greenspan era of central bank driven price falsification and monetization of trillions of existing assets with credits conjured from thin air has generated a $50 trillion overhang of excess financialization. And that’s just for the US economy. In fact, the central bank error is global and the worldwide excess financialization is orders of magnitude larger.

QE increases prices of securities. That sucks out money.

• QE ‘Sucking Out’ Liquidity In Markets (CNBC)

The aim of quantitative easing (QE) might be to increase liquidity in global markets, but it’s actually having the opposite effect, according to one analyst, who echoed comments from several financial institutions. Antonin Jullier, global head of equity trading strategy at Citi, told CNBC Tuesday that the bond-buying policies implemented by central banks including the Federal Reserve and ECB had had a detrimental effect. “The lack of liquidity is coming from QE, it’s one of the consequences…it’s sucking it out,” he said. The aggressive stimulus was “one-sided,” according to Jullier, who said it was increasing valuations of securities, but not producing more stock flotations or capital increases.

“The net inventory of securities has actually been flat for years now. So there are no new securities available,” he added, calling it a period of “de-equitization.” Central banks have been purchasing fixed-income assets in secondary bond markets since the global financial crisis of 2008. The aim is to boost liquidity in the banking sector and thus encourage banks to lend to the wider economy. As well as in the U.S. and euro zone, programs have also been launched in Japan and the U.K. Some economists have lambasted the tactic, however, and more recently market participants have voiced concerns over hefty valuations as well as a lack of liquidity.

A late sleeper?!

• Mergers Might Not Signal Optimism (Sorkin)

A boom in mergers and acquisitions usually signals confidence in the economy, and recent headline-grabbing deals evoke images of chief executives and directors cheering about their business prospects and overall growth. So far this year, deal-making activity in the United States has topped $775.8 billion, up nearly 50% compared with figures in the period last year, just behind deal volume in 2007, according to Thomson Reuters. A steady parade of multibillion-dollar deals have been announced: Charter’s $55 billion acquisition of Time Warner Cable, Teva Pharmaceuticals’s $40 billion hostile bid for Mylan and Avago’s $37 billion takeover of Broadcom are among them. But in contrast to previous merger booms, this recent spate of deals shouldn’t necessarily be considered a barometer of a healthy economy.

If anything, it might be an indicator of the troubles that lie beneath an overheated stock market. In many cases, companies are pursuing takeovers not because they are excited about a growing economy, but because their own growth prospects have waned. The numbers tell the story: Revenue growth at United States companies has declined every year for the last five years, to about 5% now from 11.2% in 2010, according to a report by Citigroup. The bank put the problem bluntly: “Many companies will therefore require a source of inorganic growth to meet analyst revenue projections.” If you can’t build it, then maybe you can buy it.

Mergers and acquisitions have always, to some degree, been a way for companies that are struggling to grow to purchase revenue. But top-line growth for most American companies has been particularly hard to come by in recent years, and to the extent that businesses have been able to continue to increase their profits, it’s been largely a function of cutting costs. That differs significantly from other economic rebounds in which merger volume has tracked increases in revenue.

According to the Citigroup report, “strategic actions, such as M.&A. and asset restructurings, have become a key priority to generate growth in the current environment. The lack of an organic impetus to growth is apparent in the outlook for capital expenditures.” The report said “globally, growth in capital expenditures rose sharply from 5% in 2010 to almost 19% in 2011 following the financial crisis but has decelerated every year since, reaching 4.6% in 2013. Over the next 12 months, the forecasted capital expenditure growth is below 2% globally.”

It is that simple.

• What’s Wrong with the Administration’s Trade-Deal Arguments (Eric Zuesse)

But there is a deeper problem than whether environmental and other standards within various nations are set higher; and it is that they are, in effect, to be set in stone by these agreements. Just as it is vastly more difficult to update a provision in the U.S. Constitution by means of of its Amendment-process than it is to enact a new mere law that updates an old mere law; so, too, it is vastly more difficult to change an international treaty-provision than it is to change a mere single nation’s regulatory standards and laws. Whereas to change a law or regulation requires only intra-national, or inside-the-nation, process, changing a treaty-provision requires a vastly more difficult international process, which demands the unanimous consent of all member-nations of the given treaty or international agreement.

These ’trade’ deals are set up, far more fundamentally, to transfer the power over the decisions concerning such matters, away from democratically accountable national governments, to, instead, panels of ‘arbitrators’ consisting of three lawyers, each one of whom is appointed by international corporations – i.e, by the very same parties whose interest is to lower workers’ wages and rights, to lower environmental standards, to lower protections against defrauding stockholders, to lower protections against global warming, to lower protections against toxics in foods, etc. [..]

..what’s really at issue here is a transfer from national democratic sovereignty to, instead, international-corporate sovereignty, in which international coporations will have locked-in an international dictatorial control over a large portion of what it is that national governments do, and necessarily must do, in order to serve the public good. The whole thing is a corrupt con-job. What is at stake here is nothing less than whether the future of the world will be national democratic governments, or instead an international fascist government. Regardless of whether the old ideal of an international democratic world-federalist government (the old idea of a world government) was a good one, the bringing-about of an international corporate dictatorship is a monstrosity: the very opposite of an international democracy.

Barack Obama wants to bring the world into international fascist control more than has ever yet existed on this planet. If he succeeds, he will thus be the most harmful political leader in world history. His deals must be stopped. They are horrendous.

To hide the real economic numbers.

• Why China Is Blowing An Equity Bubble (John Plender)

Bubbles come in different shapes and forms, but it is striking how often they are the by-product of attempts to make difficult economic transitions. This was true of the US stock market in the late 1920s as Americans reluctantly stumbled towards the hegemonic global role previously played by the British. It was true of the property and equity markets in Japan in the 1980s, when an export-led growth model that had worked well in the catch-up phase ceased to be viable in a country that had turned into an economic giant. So, too, with China today, where first a property bubble and now an incipient stock market bubble have a great deal to do with imbalances in an economy that needs to shift from investment-led growth to increased consumption.

Such transitions are difficult because of the clash of vested interests. Chinese local government officials have been big beneficiaries of easy financing of infrastructure investment and the accompanying land grab. State-owned enterprises have lived handsomely off the same gravy train. At every level of the public sector there are people for whom the status quo is a cornucopia. Equally to the point, liberalisation, which is the key to an effective transition, can only erode the power of the communist party. For those officials who see that change is essential, a further difficulty arises from the new sluggishness of the Chinese economy.

Since their legitimacy derives from delivering high economic growth they are under pressure. It is all too easy to solve the problem by throwing more money at infrastructure and at industries that suffer from surplus capacity. Yet this can only be done at the cost of creating bubbles, running up more debt and misallocating resources on a grandiose scale in what economists of the Austrian school call malinvestment. There is one sense, though, in which euphoria in mainland Chinese equities is unusual. Far from being an unintended consequence of policy, the authorities are egging investors on with articles in the state-run press seeking to justify extreme valuations.

The People’s Bank of China has been busy cutting interest rates. And to good effect. The Institute of International Finance, a club of global banks, says Chinese retail investors have increased their equity investment via margin borrowing by almost 85 per cent this year to a record $400bn. Why, you might ask, would those charming officials in Beijing wish to encourage a bubble? A consequence of the investment boom is that many state-owned enterprises are lossmaking, while state-owned banks have lent excessively to these companies and to local governments. The authorities are urging them to lend more despite the fact that they will never be repaid in full.

Far worse than getting stock tips from your shoeshine boy.

• Chinese Farmers Hope To Harvest Bumper Stock Profits (CNBC)

Farmers are eschewing crops to plough their cash into the booming stock market , a journey by CNBC into the heart of rural China discovered. Six months ago, apple farmer Liu Jianguo invested $8,000 into the Shanghai Composite, a big chunk of his life savings. “It’s a lot easier to make money from stocks than farm work,” he told CNBC’s Eunice Yoon. “But it’s risky, you can earn $1,600 in ten minutes, and lose it all in the next.” Liu is one of many residents in the village of Nanliu, located in the northern Shaanxi province, hoping to profit from a stellar stock rally that has seen the Shanghai Composite breach fresh seven-year highs. The rapid gains have sparked concerns of a bubble among the investor community but amateurs like Liu remain bullish for now.

“I’ve made some small profit and gained experience but I still feel anxious when my investments aren’t doing well,” he said. The villagers first started investing their savings in stocks after hearing about the market craze on a visit to a nearby town. As the excitement spread, a small informal stock market center was set up in the village where residents could monitor their investments by the minute. Aside from tracking market updates with computers, the savvy villagers are also using their smartphones. The farmers now only tend their fields outside of market hours, Liu noted.

“..the “value” created in just 12 months of trading on Chinese stock exchanges..”

• China’s $6.5 Trillion ‘Wonderful’ Market Bubble (Bloomberg)

It’s enough money to buy Apple eight times over, or circle the Earth 250 times with $100 bills. The figure, $6.5 trillion, sums up the value created in just 12 months of trading on Chinese stock exchanges – and why some see a rally that’s gone too far. As China’s boom surpasses the headiest days of the U.S. Internet bubble, signs of excess are cropping up everywhere. Mainland speculators have borrowed a record $348 billion to bet on further gains, novice investors are piling into shares at an unprecedented pace and price-to-earnings ratios have climbed to the highest levels in five years. The economy, meanwhile, is mired in its weakest expansion since 1990. “We have a wonderful bubble on our hands,” said Michael Every at Rabobank in Hong Kong. “Of course, there’s short-term money to be made. But I fear it will not end well.”

Chinese shares face their next big test on Tuesday, when MSCI Inc. decides whether mainland securities are eligible for indexes used by $9.5 trillion of funds worldwide. An endorsement would signal global acceptance for equities that had until recently been off limits to most overseas money managers. Rejection would deal a blow to bulls who pushed the Shanghai Composite Index to a seven-year high on Monday. While no other stock market has grown this much in dollar terms over a 12-month period, previous booms have arguably had a greater impact when adjusted for purchasing power and the size of economic output at the time.

At the height of Japan’s rally in 1989, for example, the nation’s market capitalization reached 145% of gross domestic product, versus an estimated 87% in China today, according to data from the World Bank and IMF. The DJIA climbed for five straight years in the run-up to the crash of 1929, adding more than 200%. On top of price appreciation, China’s $9.7 trillion market is getting a boost from a wave of new share sales. Mainland companies have raised at least $56 billion this year, according to data compiled by Bloomberg. Optimists are betting that China’s Communist Party will keep the rally going to help more businesses tap the stock market for fresh capital. Debt levels for Shanghai Composite companies reached the highest since at least 2005 in January.

“..a free-trade zone in which the black hole at the centre, Germany, absolutely overwhelms all of its competition, and the competition can’t protect itself, is untenable.”

• Is The European Union Already On The Brink Of Inevitable Disaster? (ABC.au)

MARK COLVIN: The European Union has seldom looked so fragile. Greece’s prime minister Alexis Tsipras has said in an interview that if Greece fails, it will be the beginning of the end of the eurozone. Tsipras argued that a ‘Grexit’, as it’s being called, would trigger the unravelling of the whole European project. Meanwhile Britain’s prime minister David Cameron has got in a political tangle over whether he’ll make his cabinet ministers fall into step and campaign for a ‘yes’ vote in Britain’s coming EU referendum. But a new book suggests that whatever happens, Europe is already on the brink of inevitable disaster. Forecaster George Friedman’s book is called ‘Flashpoints’, and he told me on Skype from Texas that Germany – Europe’s economic powerhouse – was the central problem.

GEORGE FRIEDMAN: The fact of the matter is that a free-trade zone in which the black hole at the centre, Germany, absolutely overwhelms all of its competition, and the competition can’t protect itself, is untenable.

MARK COLVIN: There’s a paradox there, isn’t there? Because really the EU was born as a solution to the problem of an overpowering Germany.

GEORGE FRIEDMAN: Precisely. And really, this goes back to around 1871. When Germany was united, it very rapidly became the economic engine of Europe. But Germany is also massively insecure. So at the same time that it was towering over France and equalling Britain in terms of its economic viability, it was also a country very afraid of the forces around it. This is what Germany is today. Germany is by far the most productive country in Europe. But its terror is that the EU will break up, not because of the Euro – that’s a side issue – but because it will lose the free-trade zone. Because you might get protectionism, they won’t be able to sell.

So the Germans are very aggressive with the Greeks, for example, trying to make a show of them, but also aware that if they make too much of a show, the other countries like Spain or Italy might consider leaving. And if they let them off the hook, they give these other countries might consider leaving, and so you are in a very difficult position if you’re Germany. And now Germany is floating the idea that they may not want to force them to pay their debts until 2016 because obviously Germany must keep the free-trade zone in fact. And bluff as it might, it’s terrified that that will close off.

No work equals no access to health care.

• Life Under Austerity Shows Why Syriza Are Fighting It So Hard (Conversation)

In order to understand why further austerity is so strongly rejected in Greece it is imperative that we understand how it has been experienced. One of the areas where this can be seen most vividly is in the country’s healthcare provision. Access to healthcare and medicine in Greece is traditionally based on social security contributions made through employment, which can then also be used by immediate family members. But these contributions have become increasingly more difficult to maintain as the effects of austerity have bitten. Statistics around employment and income highlight why. Since 2010 (when austerity was first introduced) there has been a fall in GDP of 25% and unemployment has ballooned to 26% of the total population (up from 7.7% in 2008).

The figures are even more stark when we consider that youth unemployment, which stood at a staggering 58.3% in 2013, remains around 50%. And, of all those who are unemployed, 19% have been for a year or more. This inability to pay for healthcare is then compounded by the fact that only one in ten receive some form of unemployment benefit), which could provide a buffer against these growing insecurities. For those who still have “wage-related income”, there has been a decrease per household by an average of 10.9% between 2008 and 2012 or 34.6% for those already in the lowest income bracket. Many will tell you they are lucky to earn just €400 a month from a full-time job. All of this is exasperated by lower income groups seeing their tax burden rise by 337.7%.

The effects of austerity on the economy and employment has itself created a difficult enough situation for Greek citizens to access healthcare. This has been compounded by the specific measures taken to the healthcare system. As a study in the Lancet highlights, “from 2009 to 2011, the public hospital budget was reduced by over 25%”, while there was an introduction of “new charges for visits to outpatient clinics and higher costs for medicines”. The overall reform effort has produced a 47% rise in people who feel they are not receiving the healthcare they medically require.

As the authors of the study recognise, none of this is to deny the need for reform of a health system that already did not adequately meet the needs of its users. But “the scale and speed of imposed change limited its capacity to respond to its population’s increased health needs”. This is putting things very politely.

For the record: Never underestimate the amount of real stupidity out there. A professor of economics in Milan, believe it or not. Wonder how he sees Italy.

• Greeks Chose Poverty, Let Them Have Their Way (Francesco Giavazzi)

For more than five years, Greece has been Europe’s biggest concern. Instead of focusing on employment, or immigration, or the challenge of Vladimir Putin’s Russia, the continent’s attention has been on a country that represents 1.8 per cent of the eurozone’s economic output. It would be interesting to calculate how many hours Angela Merkel has dedicated to Athens in the past five years. Imagine President Barack Obama taking part in high-level talks for months on end, where little was on the agenda except the state of Tennessee. That, in effect, is what Europe’s heads of government have been doing. In these five years the world has changed. China and India are undergoing profound transformations.

The jihadis of the Islamic State of Iraq and the Levant (Isis) represents a new and serious threats to the west, as does Mr Putin’s revanchism. But European leaders, instead of devoting their summits to the question of how to best defend our economic and military interests, agonise over what to do about Greece. Five years of negotiations that have achieved virtually nothing (the few reforms that had been adopted, like a small reduction in the inflated number of public sector employees, have since been reversed by the Syriza-led coalition). It is pretty clear that the Greeks have no appetite for modernising their society. They worry too little about an economy ruined by patronage. Europeans, too, have made mistakes. Since Athens joined the monetary union, we have lent Greece €400bn, 1.7 times the country’s gross domestic product in 2013.

It is time for a reality check: they will never be repaid. And it is an illusion to imagine, as the Finns sometimes do, that we could receive compensation in kind by acquiring a few Greek islands. The age when the British empire would do that is, luckily, over. Bygones are bygones. The sooner we accept this and forget those loans the better. If the Greeks do not want to modernise, we should accept it. By a large majority, they have voted for a government that, six months after the election, remains vastly popular. Its popularity with the electorate signals a wish to remain a nation with a per-capita income half that of Ireland, less than that of Slovenia. In a few years it will be overtaken by Chile. I only hope that no one in Athens dreams that debt forgiveness and Grexit offer an alternative path to growth.

Without economic and social reforms, Greece will remain a relatively poor country. But it is not for the rest of Europe to impose reforms on Greece. It should merely make crystal clear that without serious reforms, new official loans are over. The only way for Athens to borrow will be to convince the markets that it will pay its own bills. No more EU guarantees, explicit or otherwise.

Get. Out.

• If The Eurozone Thinks Greece Can Be Blackmailed, It’s Wrong (Costas Lapavitsas)

The never-ending Greek crisis witnessed a dramatic acceleration last week: the government submitted a list of proposals, the troika came back with a list of its own, the Greek side rejected them out of hand, a parliamentary debate followed in Athens during which the prime minister repeated the rejection, and finally Greece failed to make a scheduled payment to the IMF on 5 June, presumably bundling all its payments for the end of the month. After five years of catastrophic failure, there is a sense that the crisis is about to reach a denouement, perhaps involving default and exit. There is frustration among the population with what is perceived as the unbending attitude of the lenders. But there is also deep concern regarding the implications of default and exit.

The proposals by the Syriza government represent a painful compromise compared to its electoral promises. It has accepted tight fiscal targets, and to achieve them it is offering to raise VAT on several goods, while also imposing a substantial tax burden on the rich, thus achieving some redistribution. It has also toned down its policies on privatisation and pensions. In return it is asking the troika for an immediate injection of liquidity, as well as for a serious commitment to reduce Greek debt and to promote long-term investment. There is hardly anything revolutionary, nor even particularly radical, in these demands. The response of the eurozone creditors, judging by a leaked “official” document, has been ruthless.

They have set fiscal targets slightly above those of Syriza, but to achieve these they are demanding a substantial increase in VAT, including a rise of 10% on electricity, thus hitting the poorest where it hurts. They are also demanding the abolition of subsidies and tax relief measures (including for farmers and poor pensioners), and pension cuts. Finally they demand an end to collective bargaining, no increase of the minimum wage and sustained privatisations. These are familiar measures proposed by the IMF on many occasions across the world. They represent failed and outdated economic thinking, and are likely to mean low growth, high unemployment and low incomes. Even worse, the troika is making no suggestions regarding the settlement of debt and future investment.

Greece is offered only a temporary reprieve on very tough terms. It will soon have to get back to the negotiating table to deal with the longer-term issues, involving fresh loans of perhaps €40-50bn. The Syriza government was quite right to reject these proposals and to fire a shot across the bows of the lenders by refusing to pay the IMF on 5 June. But the real question is, what is going to happen now? It is quite apparent that the eurozone creditors have no intention of offering Syriza a deal that would allow it to claim even a smidgeon of victory. Syriza is too much of a danger for the European status quo, and it must be taken down several pegs. It will have to be made to comply with the tough austerity policies that have become entrenched in the eurozone. As far as the lenders are concerned, there is no other option for Greece.

Yanis does a great version of Aesop’s fable.

• Greece, Germany and the Eurozone – Keynote, Berlin June 8 2015 (Varoufakis)

Earlier I referred to the Aesop fable that has done so much damage to our peoples’ understanding of their relation and to their appreciation of each other. Allow me to re-tell it in a manner better suited to the economic circumstances of the Eurozone. To begin with, I hope you agree that the idea that all the ants live in the North of Europe and all the grasshoppers have congregated in the South, in the Periphery, would have been comical if it were not so offensive and so destructive of our shared European project. What happened in Europe after we established the euro, during the good times, was that the ants worked hard everywhere, in Germany and in Greece. And the ants were finding it hard to make ends meet. Both in Germany and in Greece.

In contrast, the grasshoppers both in Greece and in Germany were having a finance-fuelled party. The flow of private money from Germany to Greece allowed the grasshoppers of the North and the Grasshoppers of the South to create huge paper wealth for themselves at the expense of the ants – of the German and the Greek ants. Then, when the crisis hit, it was the ants of the North and especially the ants of the South, of Greece, that were called upon to bailout the grasshoppers of both nations. These bailouts cost the ants dearly. Especially the Greek ants lost their jobs, their houses, their pensions while the German ants felt cheated, hearing about all these billions going to the Greeks while their living standards refused to rise despite their productive eforts.

As for the Greek grasshoppers, some of them also suffered but the big, fat ones had nothing to worry about: they took their ill gotten monies to Geneva, to London, to Frankfurt. And they laughed all the way to the bank. This is what was so wrong with the bailouts. It is not that Germans did not pay enough for Greeks. They paid far too much. For the wrong reasons. Money that, rather than help the Greeks, was thrown into a black hole of unsustainable debts while people suffered everywhere. From debt fuelled growth we went full circle to debt fuelles austerity. It is this vicious cycle that our government was elected to put an end to.

The price of progress.

• Too Poor To Die: The Pauper’s Funeral Returns In Austerity Britain (Guardian)

The manager of a north Liverpool credit union recently told me that the most shocking fallout of the recession and austerity was the sheer volume of people calling because they were unable to bury their loved ones. “People call from the hospital, because they can’t pay the £1,000 to get the undertakers to release the body,” she said. “And these people, they’re under 50. That’s no age to die.” The sharp rise in funeral poverty is one of the grimmer trends in our unequal island: in the past decade, funeral costs have risen by 80%. Wages simply haven’t. The average funeral now costs £3,163 nationally, and £4,836 in London.

If you’re on a low income, the cost of a sudden death is far beyond your modest means, and life insurance can seem like an unnecessary luxury when you’re struggling to heat your home and feed your children. The families who contact Quaker Social Action (QSA), a small charity which offer advice on funeral poverty through its “Down to Earth” scheme, aren’t seeking a lavish send-off for their loved ones, just the ability to bury them at all. All too often, relatives are struggling to raise the necessary capital for a basic funeral, and have to battle to get clear information from funeral directors on costs and expenses. While struggling with grief, many people are unclear on what is a fair price to pay for a funeral – the attendant shame of asking whether prices need to be so high puts vulnerable people in an even worse financial position.

People told QSA of funeral directors asking whether their deceased relative “deserved better”, with staff pressing relatives to pay more for embalming as it was “dignified for the deceased”. One woman contacted QSA when she was quoted £7,500 for a funeral by a firm who told her that was standard: the charity were able to find a provider for £1,500 nearby. But that’s the issue – death isn’t a routine enough event for us to be familiar with the costs and implications of funerals, so QSA is calling for all funeral directors to sign its Fair Funerals Pledge, promising transparency in pricing and ethical behaviour. Families can then look online to see which local funeral directors have committed to be fair and honest about the costs involved.

“No Deutsche Bank employees have been accused of wrongdoing in the case..”

• Prosecutors Search Deutsche Bank Offices For Transaction Evidence (Reuters)

Deutsche Bank offices in Frankfurt were searched on Tuesday by German prosecutors seeking evidence related to client securities transactions, Germany’s largest lender said. A source familiar with the situation told Reuters the raid was related to German private bank Sal. Oppenheim, which Deutsche Bank bought in 2010. No Deutsche Bank employees have been accused of wrongdoing in the case, a bank spokesman said. A spokesman for the Frankfurt prosecutors’ office said “wide-ranging investigative measures” had been carried out, but declined to give no details on the target or cause of the probe.

Deutsche Bank shares extended losses to trade down 3.2% by 6 a.m. EDT, in line with the STOXX Europe 600 banking index. The lender, which on Sunday announced the surprise departure of its Co-Chief Executives Anshu Jain and Juergen Fitschen following a sharp drop in shareholder confidence in the pair, has been straining to rebuild its reputation in face of a raft of legal and regulatory problems. Those problems have prompted billions of dollars in fines and settlements. Authorities have repeatedly raided its offices in recent years in connection with investigations linked to the collapse of the Kirch media empire and a tax fraud case related to the trading of carbon dioxide emissions rights.

How US justice became an oxymoron.

• US Police Kill More In Days Than Other Countries Do In Years (Guardian)

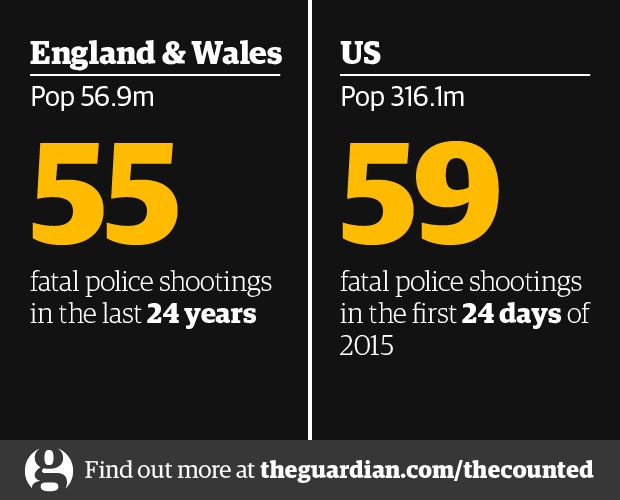

It’s rather difficult to compare data from different time periods, according to different methodologies, across different parts of the world, and still come to definitive conclusions. But now that we have built The Counted, a definitive record of people killed by police in the US this year, at least there is some accountability in America – even if data from the rest of the world is still catching up. It is undeniable that police in the US often contend with much more violent situations and more heavily armed individuals than police in other developed democratic societies. Still, looking at our data for the US against admittedly less reliable information on police killings elsewhere paints a dramatic portrait, and one that resonates with protests that have gone global since a killing last year in Ferguson, Missouri: the US is not just some outlier in terms of police violence when compared with countries of similar economic and political standing. America is the outlier – and this is what a crisis looks like.

Fact: In the first 24 days of 2015, police in the US fatally shot more people than police did in England and Wales, combined, over the past 24 years. Behind the numbers: According to The Counted, the Guardian’s special project to track every police killing this year, there were 59 fatal police shootings in the US for the days between 1 January and 24 January. According to data collected by the UK advocacy group Inquest, there have been 55 fatal police shootings – total – in England and Wales from 1990 to 2014. The US population is roughly six times that of England and Wales. According to the World Bank, the US has a per capita intentional homicide rate five times that of the UK.

Almost funny.

• Hiring Black Officers Is Difficult: ‘So Many Have Spent Time In Jail’ (Guardian)

Hiring more non-white officers is difficult because so many would-be recruits have criminal records, New York police commissioner Bill Bratton has said. “We have a significant population gap among African American males because so many of them have spent time in jail and, as such, we can’t hire them,” Bratton said in an interview with the Guardian. Police departments, responding to widespread protests against several high-profile police killings of black men, are boosting efforts to recruit more non-white officers. But budget restrictions, strained relations between police and minority communities and, according to Bratton, a history of indiscriminate policing tactics that disproportionately target black and Latino men complicate the department’s goal of racial parity.

Bratton blamed the “unfortunate consequences” of an explosion in “stop, question and frisk” incidents that caught many young men of color in the net. As a result, Bratton said, the “population pool [of eligible non-white officers] is much smaller than it might ordinarily have been”. The controversial stop-and-frisk policy was struck down in 2013 by a federal judge, who called the practice a “policy of indirect racial profiling”. Judge Shira A Scheindlin found that the program led officers to routinely stop “blacks and Hispanics who would not have been stopped if they were white”.

But critics say Bratton, who helped shrink the widespread use of stop-and-frisk is partly, if not ultimately, responsible for the relative paucity of eligible non-white recruits. “It is a net that he set out for them,” said Rochelle Bilal, vice-chair of the National Black Police Association and a former Philadelphia police officer. “If [Bratton] didn’t stop people for nothing, he might have a bigger pool to hire from.”

Half-ass legislation.

• San Francisco First City To Approve Health Warning On Sugary Drinks (AP)

San Francisco supervisors have approved imposing a health warning on ads for sugary soft drinks and some other beverages, saying they contribute to obesity, diabetes and other health problems. Observers believe San Francisco would be the first place in the country to require such a warning if it receives final approval. The ordinance would require the warnings on print advertising within city limits “billboards, walls, taxis and buses. It would not apply to ads appearing in newspapers, circulars, broadcast outlets or on the Internet. The ordinance defines sugar-sweetened beverages as drinks with more than 25 calories from sweeteners per 340 grams. It requires warnings for other sugary drinks such as sports and energy drinks, vitamin waters, iced teas and certain juices that exceed the 25-calorie limit.

Liquid sugar is the new tobacco, as far as public health advocates are concerned. Berkeley approved a soda tax last year, the first in the country to do so. Davis, a college town, is requiring restaurants to serve milk and water as the default drink for children’s meals. About 32% of children and teens in San Francisco are overweight or obese, according to a 2012 study by the California Center for Public Health Advocacy and the UCLA Center for Health Policy Research. “This is a very important step forward in terms of setting strong public policy around the need to reduce consumption of sugary drinks; they are making people sick, they’re helping fuel the explosion of Type 2 diabetes and other health problems in adults and in children,” said Scott Wiener, one of three San Francisco supervisors pushing the legislation.

Roger Salazar, a spokesman for CalBev, the state’s beverage association, said, “it’s unfortunate the Board of Supervisors is choosing the politically expedient route of scapegoating instead of finding a genuine and comprehensive solution to the complex issues of obesity and diabetes.” The label for billboards and other ads would read: “WARNING: Drinking beverages with added sugar(s) contributes to obesity, diabetes, and tooth decay. This is a message from the City and County of San Francisco.” Soft drinks cans and bottles would not carry the warning.

Italy does the only thing it can do: let refugess find their way towards Germany.

• Migrants Race Through Italy To Dodge EU Asylum Rules (Reuters)

[..] .. while most of Europe agrees more needs to be done to rescue people at sea, the EU is deeply at odds over how to cope with them once they are ashore – a divide that reflects both the difficulties of European policy making and the rising tide of anti-immigration sentiment sweeping the continent. EU asylum rules, known as the Dublin Regulation, were first drafted in the early 1990s and require people seeking refuge to do so in the European country where they first set foot. Northern European countries defend the policy as a way to prevent multiple applications across the continent. Some are upset with what they see as Italy’s lax attitude to registering asylum seekers. Earlier this year, French police stopped about 1,000 migrants near the border and returned them to Italy.

Smaller round-ups happen daily in Austria, with migrants returned to the Italian side of the Brennero pass. “Some countries do not work very well in registering asylum seekers and refugees,” Stephan Mayer, a conservative German lawmaker who is part of Germany’s parliamentary committee on migrant legislation, told Reuters. But Italy, which receives the bulk of seaborne migrants, says the law is unfair and logistically impossible. It wants a major rethink. “These rules are not rules that help us tackle the problem, because they leave Italy isolated,” Italian Prime Minister Matteo Renzi said of the EU asylum regulations on Sunday. Italian officials say they are stepping up efforts to fingerprint all migrants and potential asylum seekers, but estimate that between a quarter and half of all those who land in Italy dodge the rules.

Part of the problem, says Fulvio Coslovi, a secretary for the Coisp police union in Bolzano, is that it is not a crime in Italy for migrants to refuse fingerprinting, which is how the EU keeps track of where someone enters the bloc. Police, therefore, do not typically force people to register. Coslovi said that the failure to identify migrants helps Italy. “Italy would like to rescue the migrants, but not take care of them,” Coslovi said. “In other words, we want them to disappear.”

The EU claims it has place for 40,000 through the entire year.

• Migrants Crossing Mediterranean Exceed 100,000 So Far This Year (AP)

More than 100,000 migrants – many fleeing the war in Syria – have crossed the Mediterranean Sea to Europe so far this year, the UN refugee agency said Tuesday – and the arrivals in Greece have reached their highest level since the crisis began. Citing national figures, the UNHCR said 54,000 people had traveled illegally to Italy and 48,000 to Greece so far in 2015, with another small fraction heading for Spain and Malta. The numbers were announced as the European Union is struggling to persuade its 28 nations to adopt a quota system aimed at making the crossings less dangerous and easing the burden on Mediterranean countries. In Italy, nearly 6,000 people were picked up over the weekend by a host of ships taking part in the EU-mandated Mediterranean rescue operation.

Most were sub-Saharan African migrants who had set off from Libya. The Italian coast guard and navy ships on Tuesday brought hundreds of migrants to shore in Sicily after having rescued them over the last few days. Officers wearing surgical masks and white coveralls directed the migrants to a processing tent set up at Pozzallo, a port in southern Sicily. AP footage showed one officer dragging an immigrant out of a cabin and striking another man sitting on the deck of a rescue vessel. In Greece, authorities said 457 people had been rescued from the sea in 12 separate incidents off the islands of Lesvos, Chios, Kalymnos and Kos – islands that all face the coast of Turkey – in 24 hours from Monday morning. Another 304 people had made their way ashore Monday to Lesvos’ main port of Mytilene.

The UN agency said about half of the 600 people who arrive daily in Greece are heading to Lesvos – where numbers have shot up from 737 in in January to 7,200 in May. “Record numbers of the refugees are arriving in flimsy rubber dinghies and wooden boats on the Greek island of Lesvos, putting an enormous strain on its capacity, services and resources,» it said. Few migrants want to remain in debt-stricken Greece, where unemployment runs above 26 percent. Most aim to make their way to the more prosperous countries of Europe’s center and north. They usually travel by land across Greece’s northern border with the Former Yugoslav Republic of Macedonia or cross the Ionian and Adriatic seas smuggled aboard ferries into Italy.